Health Insurance and Health Priorities

This is a summary of a major public opinion study conducted by Abacus Data, using an online methodology, for the Canadian Life and Health Insurance Association. The sample size for the survey was 3,800 adult Canadians and the fieldwork was conducted from January 31 to February 14, 2022. The margin of error for a comparable probability sample is 1.6%, 19 times out of 20.

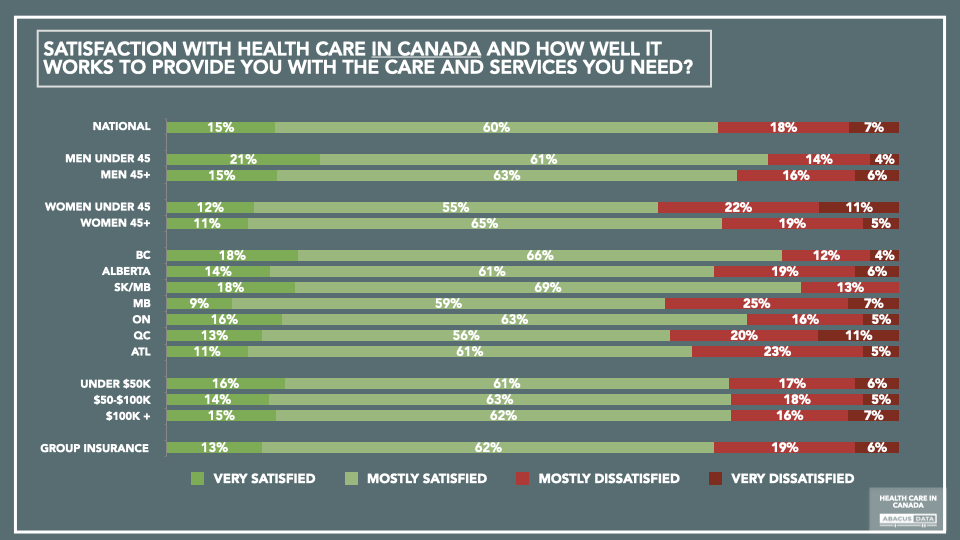

SATISFACTION WITH HEALTH CARE IN CANADA

While health care is often discussed as one of the top priorities for most Canadians, this can sometimes obscure the fact that three out of four people say they are generally satisfied with the way the health care system works for them.

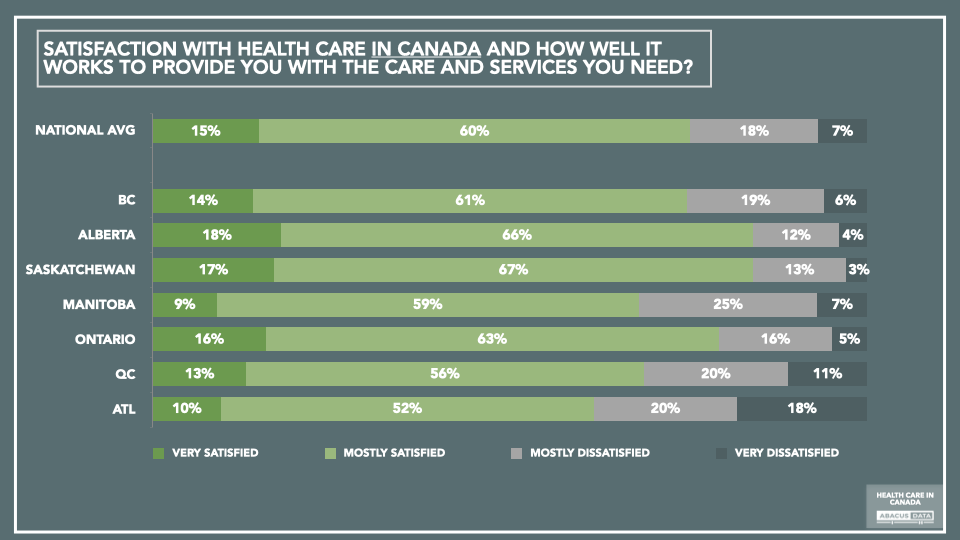

Satisfaction levels don’t vary by income level. BC, Saskatchewan, and Ontario residents show higher levels of satisfaction than Alberta, Manitoba, Quebec, and Atlantic Canadians. Dissatisfaction is highest among women under 45.

While many areas of public policy show marked differences by partisan affiliation or voting preferences, this is not so clear-cut when it comes to health care. More than 70% of those who voted for the Conservatives, Liberals, NDP, and Green parties all express general satisfaction with how the health care system serves their needs.

DETAILED SATISFACTION PROBING

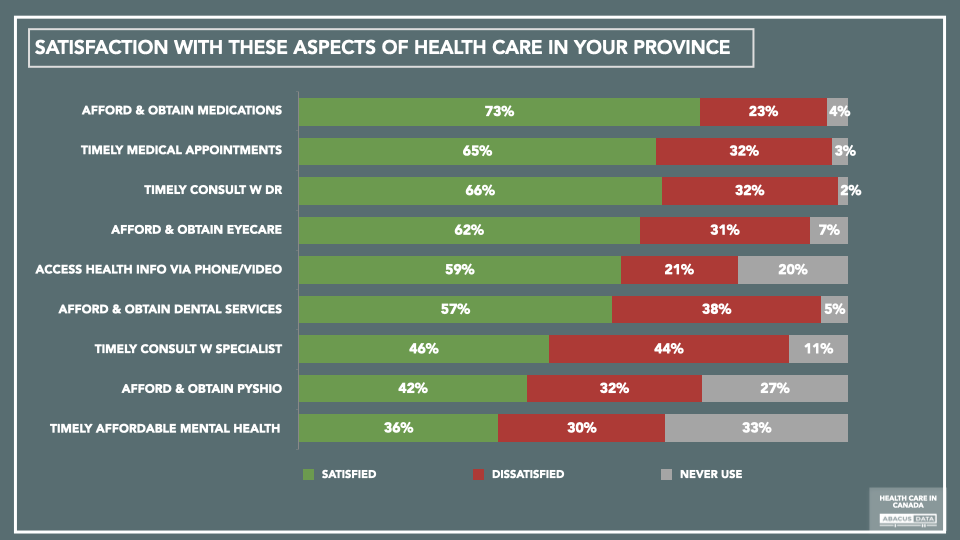

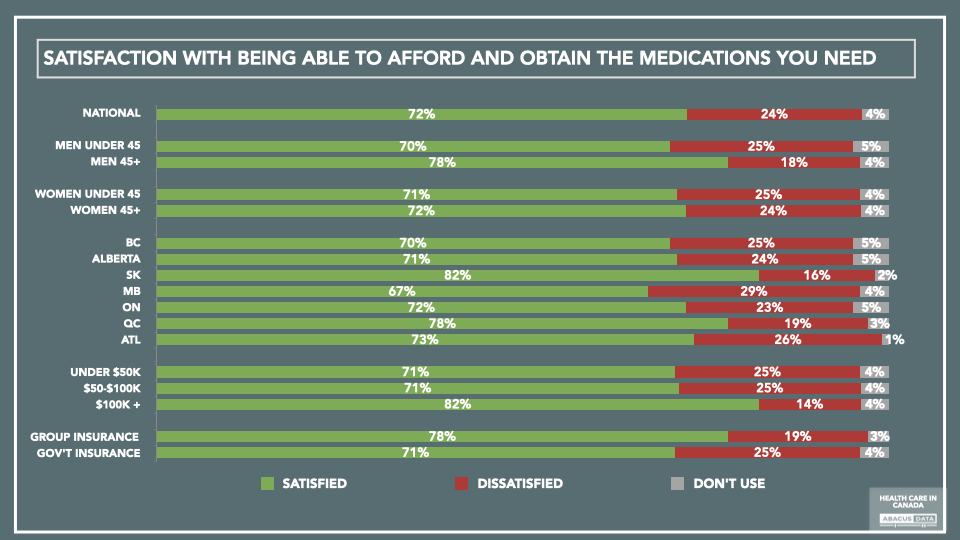

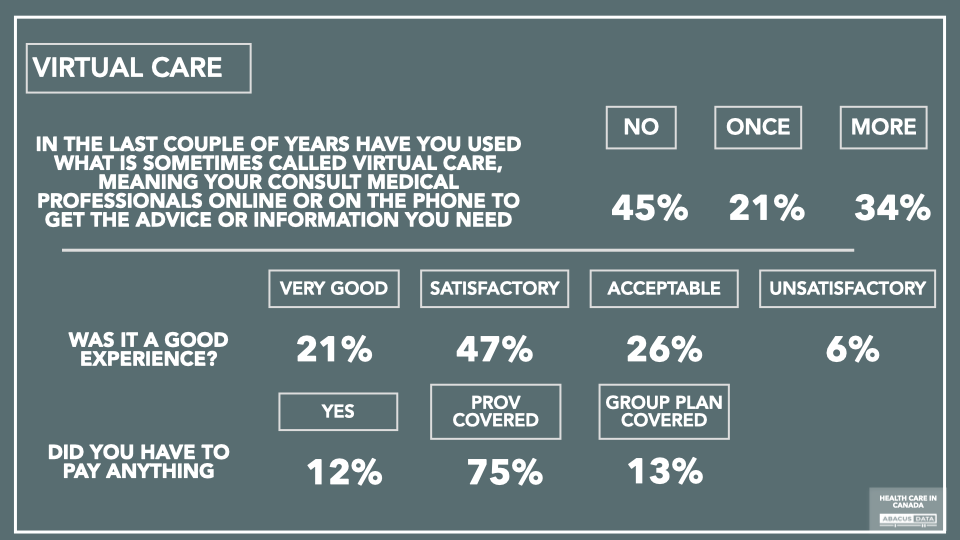

Not all aspects of the health care system generate the same level of satisfaction. At the top of the list of things that people are more likely to be satisfied with is their ability to afford and obtain the medications they need: 73% are satisfied, 23% dissatisfied, and 4% don’t use this form of health service enough to have formed an opinion. Also highly rated is the ability to access health information using phone or video services (virtual health care) with 59% satisfied, 21% dissatisfied, and 20% unable to have formed an opinion yet.

Dissatisfaction is about one in three when it comes to being able to get timely appointments and consultations with a doctor, higher still when it comes to appointments with specialists. About a third are dissatisfied with the ability to afford and obtain eye care, physiotherapy, and dental care.

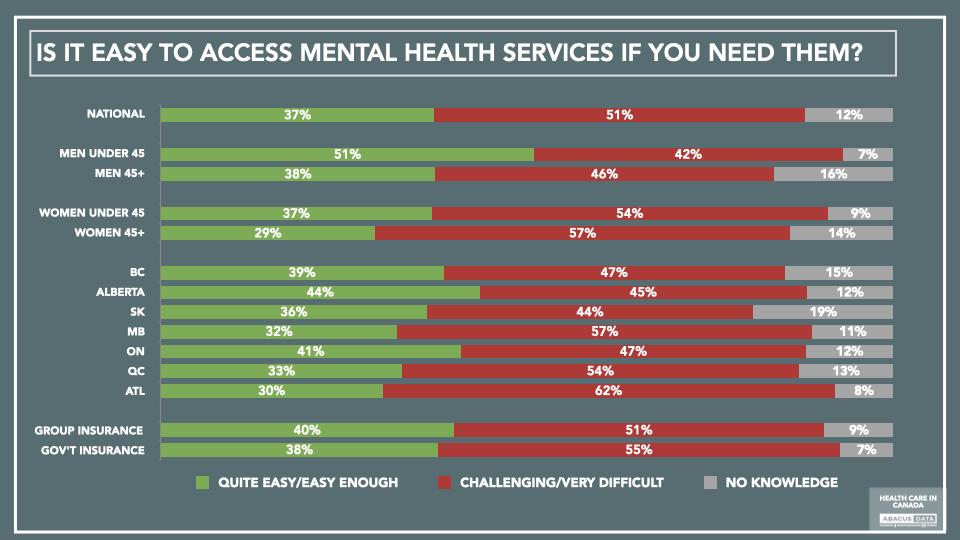

Among those who have accessed or looked to access mental health services satisfaction (36%) is almost equaled by dissatisfaction (30%).

When it comes to satisfaction with affordability and access to medications there are few significant differences. Today, 78% of those who are able to access a group health benefits plan are satisfied with the affordability of their medicines.

IMPACT OF COVID

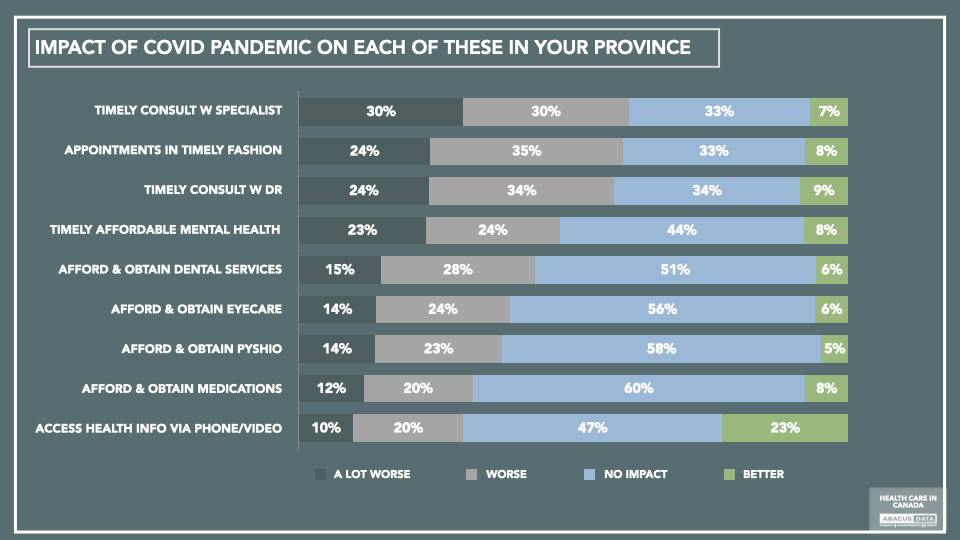

A majority of those surveyed felt that the COVID-19 pandemic made things worse in some aspects of the health system – specifically in terms of allowing for timely appointments with doctors and specialists. However, it is notable that almost as many (47%) said that being able to get timely and affordable mental health support was made more difficult by the pandemic.

The only area where a significant number (albeit the minority) said that the pandemic had a positive impact was on virtual health – the idea of being able to consult health providers by phone or video. For those who used virtual health services, satisfaction levels are high.

SATISFACTION WITH EXTENDED HEALTH BENEFIT PLANS

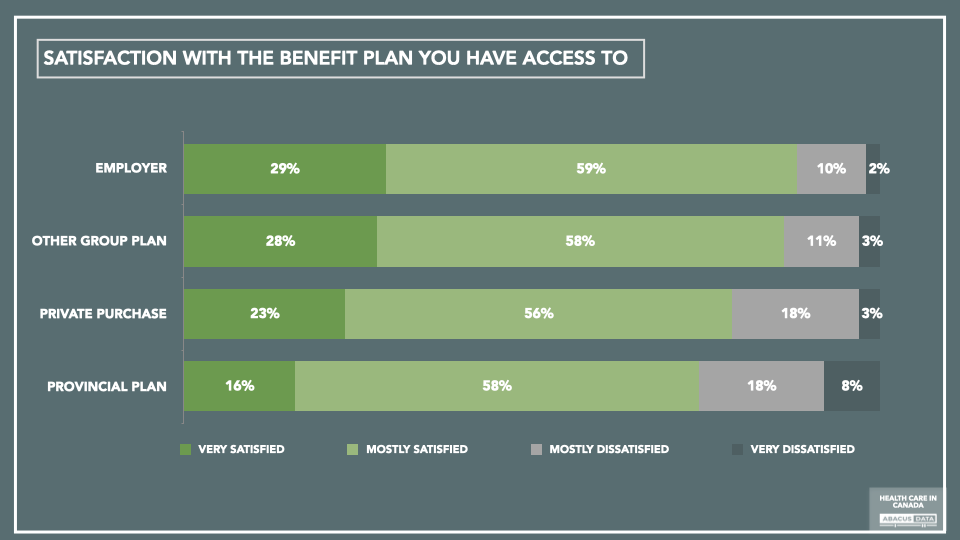

Canadians are generally satisfied with the health benefit plans available to them and see them as helpful in dealing with cost-of-living challenges. Among those who have access to an employer or another similar group plan, 86%-88% say they are very or mostly satisfied with these plans. Those who have privately purchased insurance are 80% satisfied, and those who have access to extended benefits through a provincial plan are 74% satisfied.

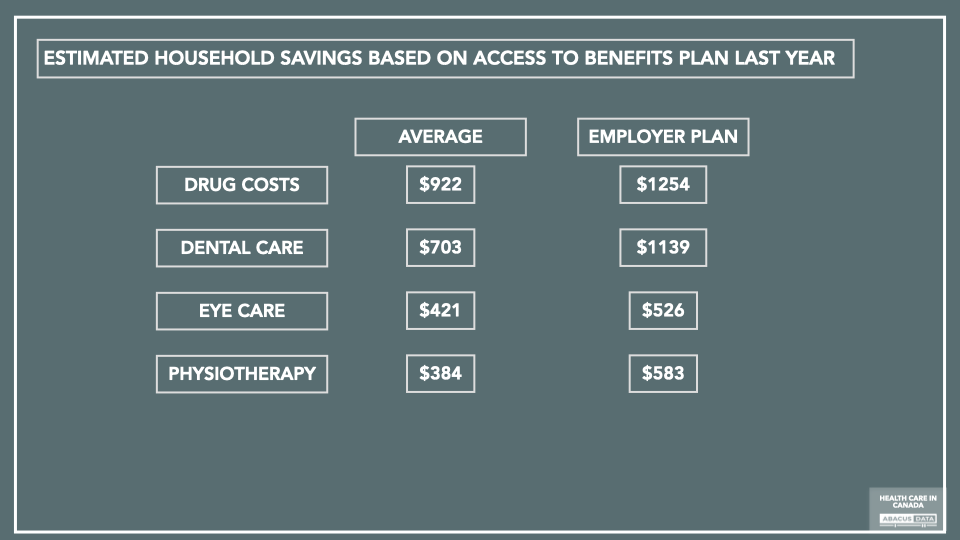

Those who have access to an extended benefits plan were asked to estimate the savings to their household when it came to drug costs, dental care, eye care, and physiotherapy. The estimated savings were extensive with an average of $922 in prescription drugs, $703 for dental care, $421 for eye care, and $384 for physiotherapy. Those with access to an employer benefits plan reported significantly above average savings.

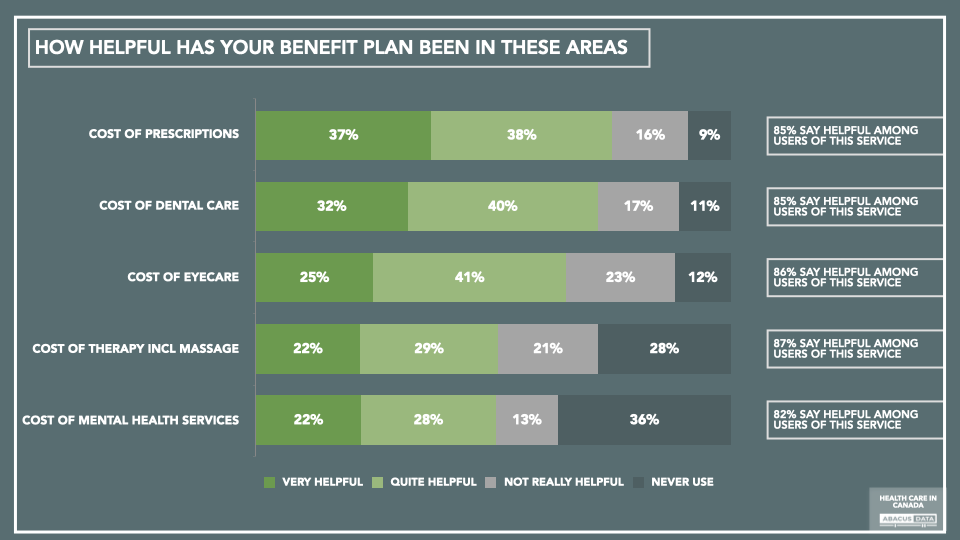

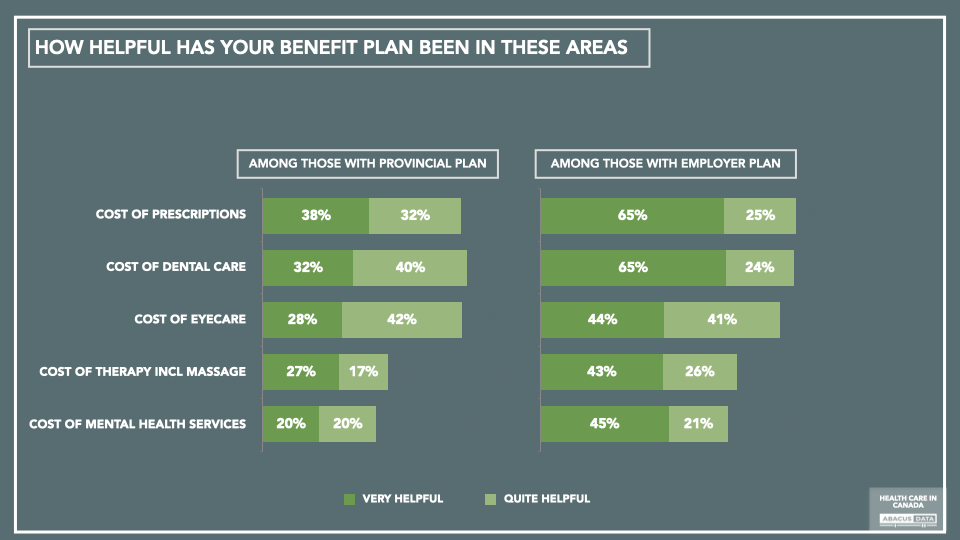

The large majority (85%) of those who have access to an extended benefits plan find it helpful with access and affordability for a variety of health services that they need to access, from prescriptions to mental health. Satisfaction levels are significantly stronger among those who have access to an employer benefit plan compared to those who access a provincial benefits plan.

GROUP INSURANCE AND PUBLIC HEALTH

Canadians are far more likely to see group benefit plans as something which increases the availability and affordability of health services in Canada (78%) rather than something that erodes the idea of universal coverage (28%).

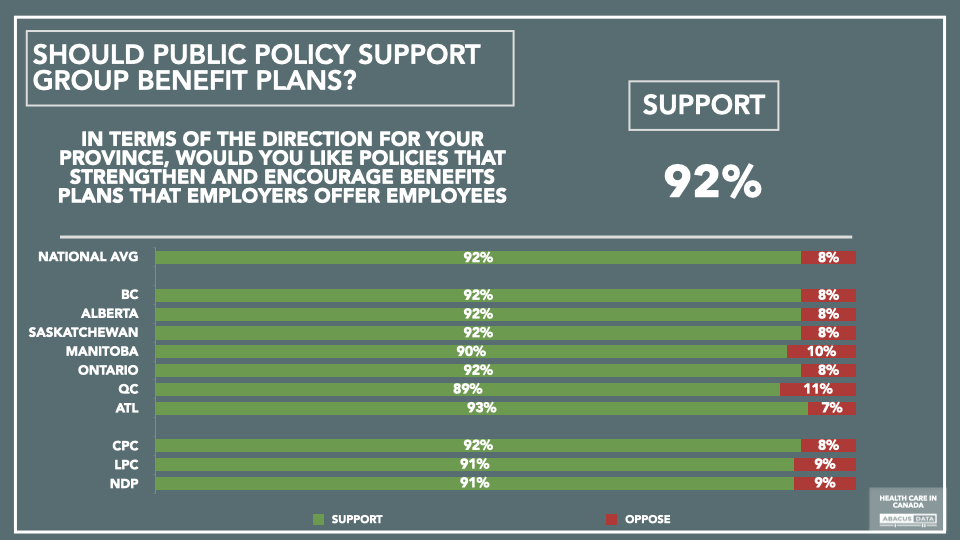

As a consequence of this view that group plans add rather than subtract from public health goals, across the country, and across the political spectrum, there is a virtually unanimous (92%) desire for public policies that strengthen and encourage the use of employer group plans.

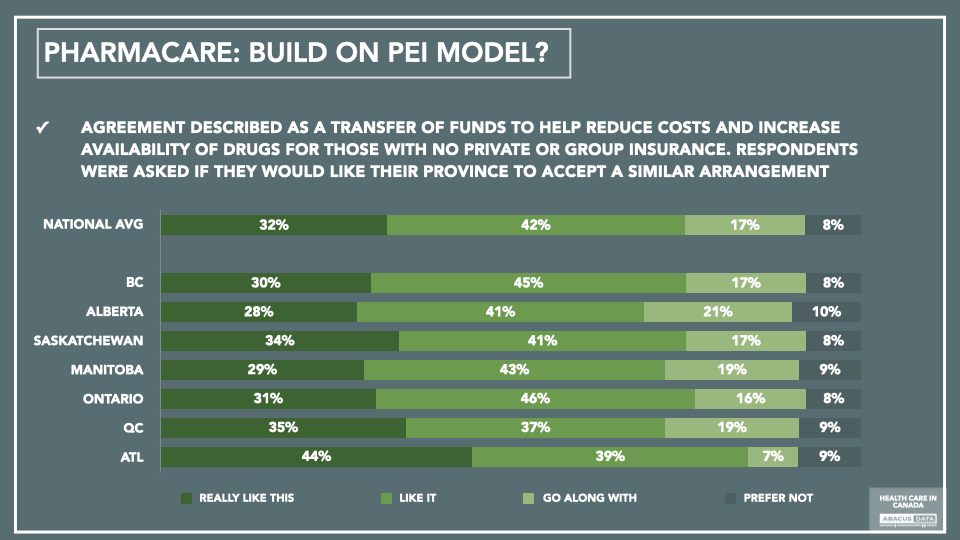

PHARMACARE & THE PEI MODEL

For several years, our surveys have shown that Canadians would like to see public policies that ensure prescription drugs are affordable for those who do not currently have access to plans that help them with drug costs.

In this survey, we described the approach taken to introduce a version of Pharmacare in the province of PEI and found that by a wide margin Canadians would endorse a similar Pharmacare approach being taken in their own province – providing support for those who have no coverage today (72%) rather than causing everyone who has a plan to switch to a government plan which might cover the most common, but fewer drugs. (28%).

Across the country, an average of 74% would like their province to embrace a similar transfer of funds to provide this type of coverage, while only 8% would prefer not to see this happen.

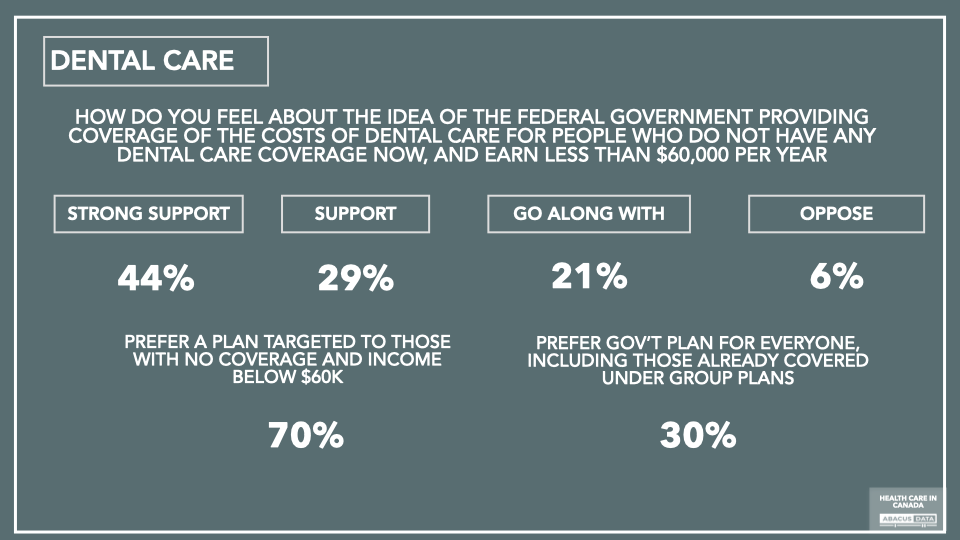

DENTAL CARE

There is broad support for the idea of a federal initiative to ensure dental care coverage for those who do not have access to coverage under a current plan, and whose income falls below a $60,000 threshold. Only 6% oppose this idea and 44% express strong support.

Given a choice between the federal government providing a single program that provides coverage for everyone – including those who already have dental benefits – or an initiative focused on those with lower incomes and no coverage, the substantial majority (70%) prefer a targeted approach.

MENTAL HEALTH

Our recent surveys have indicated a growing demand for mental health services and this survey contributes more evidence that people are finding it a challenge to get the services they need. Just under half say they have accessed mental health services, regularly (12%) or from time to time (30%). More people say it is difficult than say it is easy to get mental health services.

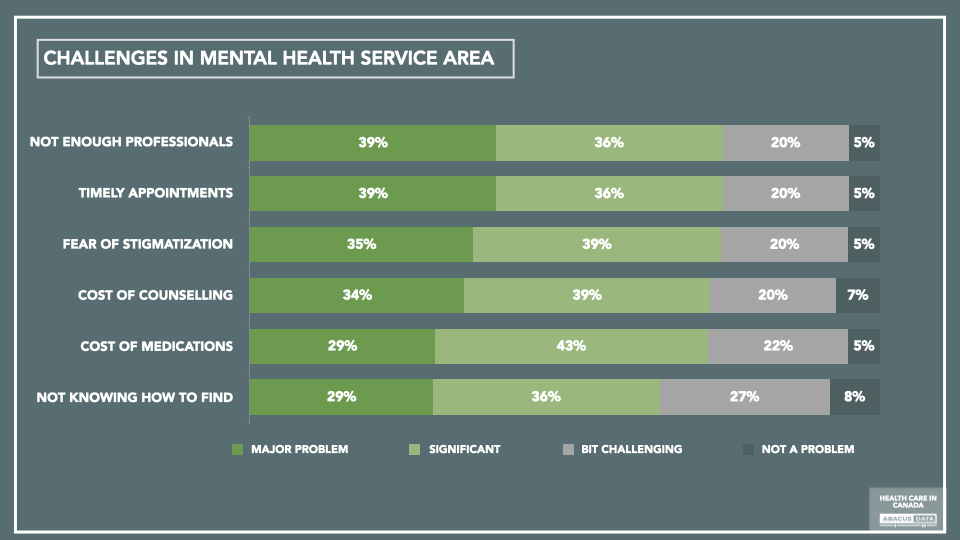

Many people see challenges in terms of the number of professionals available to provide mental health services, the availability of timely appointments, the cost of counselling and medications. A large majority also see the fear of stigmatization as a major or significant problem.

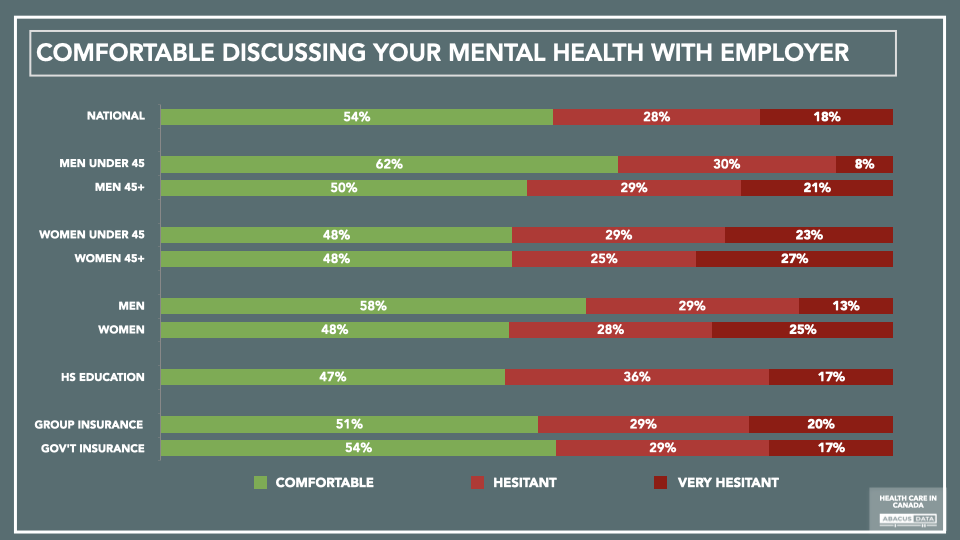

While just over half (54%) say they would feel comfortable discussing their mental health with their employer, almost as many say they would be hesitant (46%). Women indicate 11-point higher levels of hesitancy.

CONCLUSIONS

Most Canadians are satisfied with how Canada’s health care system meets their needs but there are some areas where satisfaction is lower and others where it is higher. People are relatively satisfied with their ability to access affordable medications, but timely access to specialists, the cost of dental care and access to mental health services are more challenging.

Covid has made accessing appointments more challenging, but at the same time there was growth in the use of virtual medicine, and a desire to see more of this functionality in the future.

Canadians consider extended health benefits plans that are in place today highly beneficial in terms of saving them money. This is especially true for those who have access to group insurance plans where the average person indicates that they save significant amounts of money each year when it comes to drugs, eyecare, dental care, and physiotherapy.

Support remains broad for the idea of the government ensuring drug coverage for those who do not have access to such plans today, and there is a clear preference for a targeted plan rather than a single-payer, one program for all approach, which might cause some people to see their current benefits reduced.

There is a growing need for mental health services and a feeling that these are harder to access than is ideal. Looking through the breadth of results in this survey, mental health is probably the topic that reveals the greatest hope for improvement in terms of health system support today.

METHODOLOGY

The survey was conducted with 3,800 adult Canadians from January 31 to February 14, 2022. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 1.6%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

This survey was paid for by the Canadian Life and Health Insurance Association.

ABOUT ABACUS DATA

We are the only research and strategy firm that helps organizations respond to the disruptive risks and opportunities in a world where demographics and technology are changing more quickly than ever.

We are an innovative, fast-growing public opinion and marketing research consultancy. We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

We were one of the most accurate pollsters conducting research during the 2021 Canadian election following up on our outstanding record in 2019.