From 12:00 pm ET on Thursday until 10:00 am ET Friday, Abacus Data conducted a national survey of 1,500 adults commissioned by CUPE, the union representing Air Canada’s flight attendants to understand how Canadians are feeling about the potential for a strike or lockout and the core issues in dispute.

The results reveal a strong current of public support for the flight attendants’ position. Most Canadians believe flight attendants should be paid for all aspects of their work, consider their key bargaining proposals reasonable, think Air Canada can afford to do more, and oppose federal intervention to force a return to work. Strikingly, these views cut across political lines, leaving little political advantage for the federal government that might consider legislating an end to the dispute.

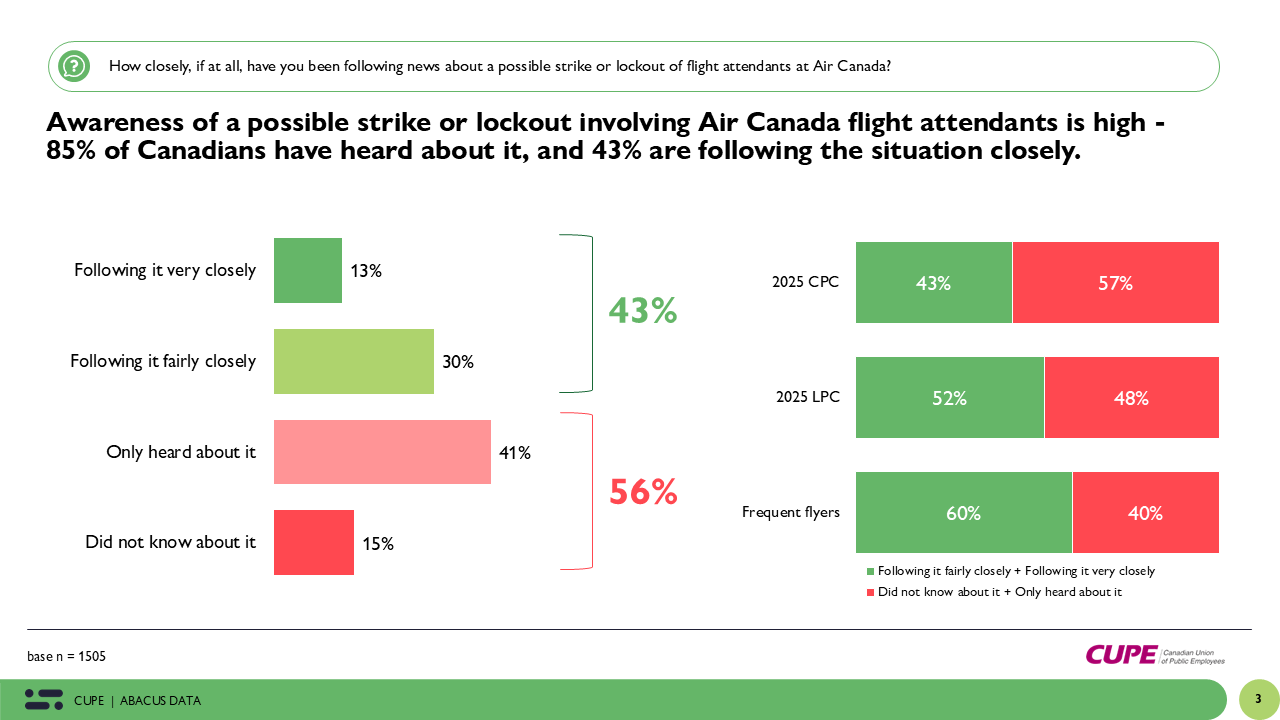

Awareness of the Dispute

A clear majority of Canadians are aware of the possibility of a strike or lockout by Air Canada’s flight attendants. Just under one in six say they had not heard about it at all, while most have at least heard something. About three in ten are following the situation fairly closely and one in ten very closely.

Awareness is somewhat higher among Liberal supporters than Conservatives, and especially high among frequent flyers, a group that could be most directly impacted by service disruptions.

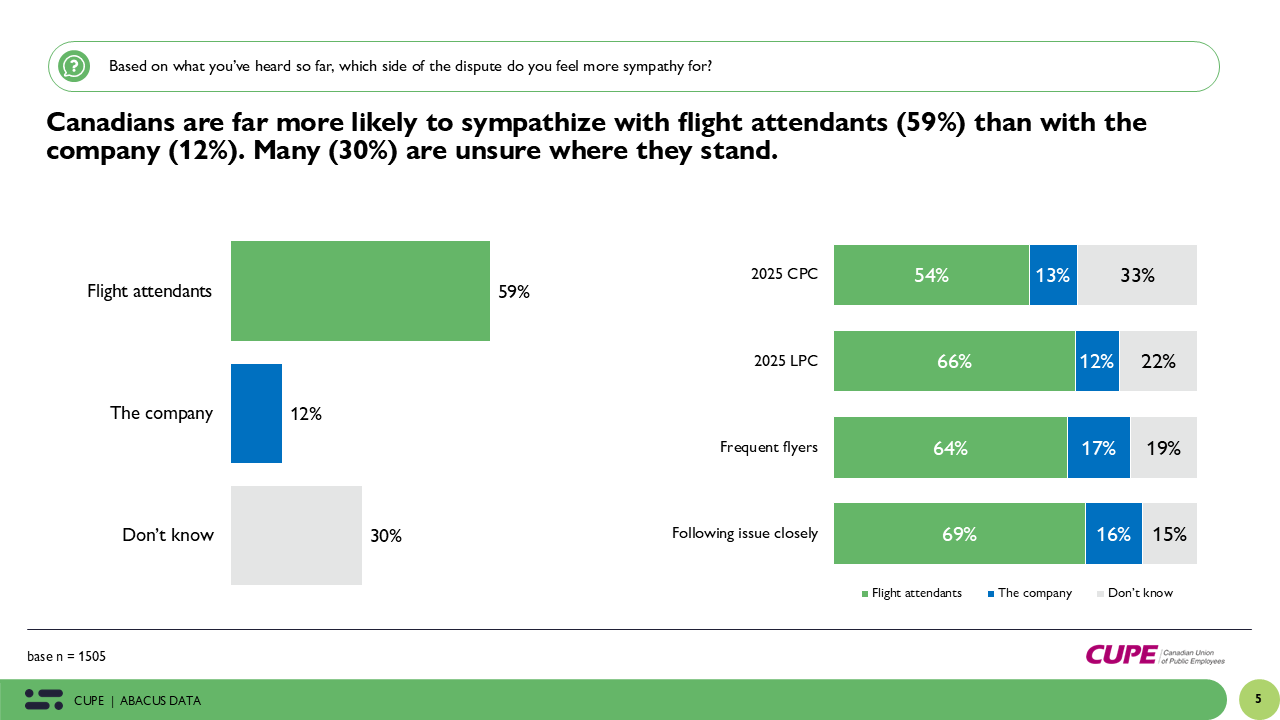

Sympathy for the Parties

When asked which side they feel more sympathy for, a majority of Canadians side with the flight attendants. Only a small minority say they sympathize more with the company, while a third are unsure.

Support for the flight attendants is especially strong among Liberal supporters, but even among Conservatives, more people sympathize with the workers than with the company.

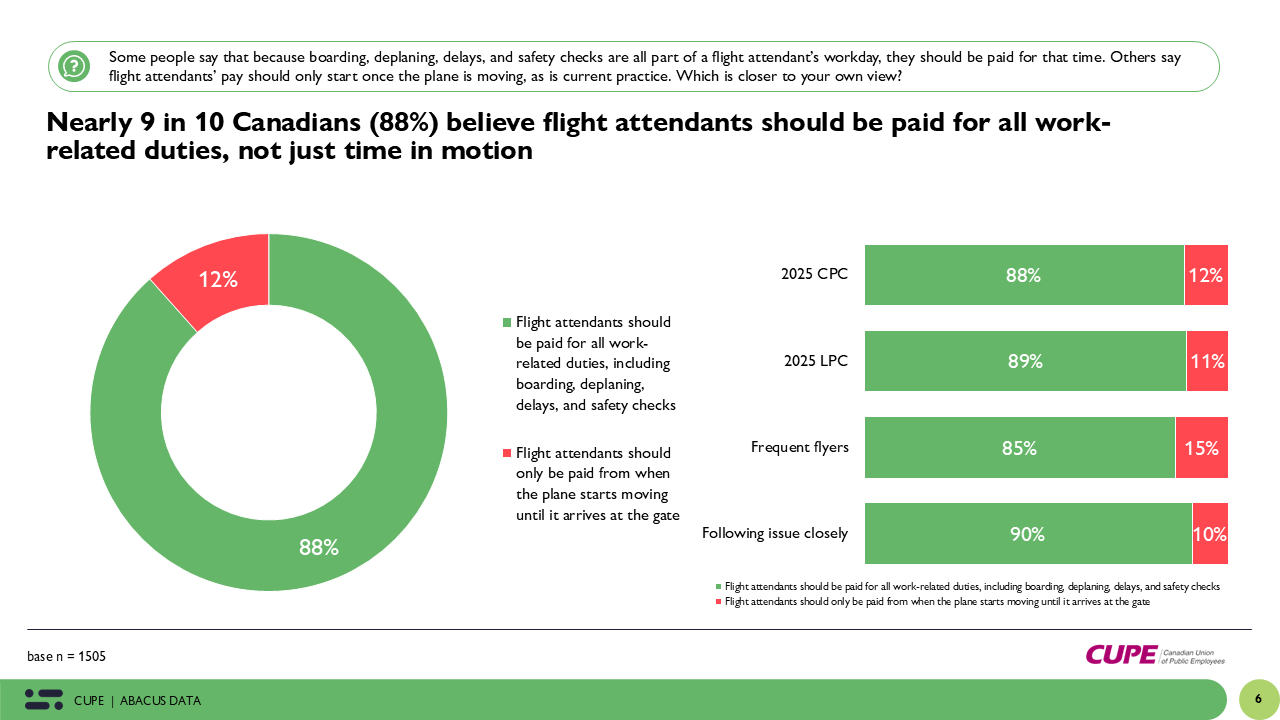

Pay for All Duties

One of the clearest points of consensus in the survey is the belief that flight attendants should be paid for all work-related duties, not just when the plane is moving. Nearly nine in ten Canadians agree with this position, and there is virtually no difference between Liberal and Conservative voters.

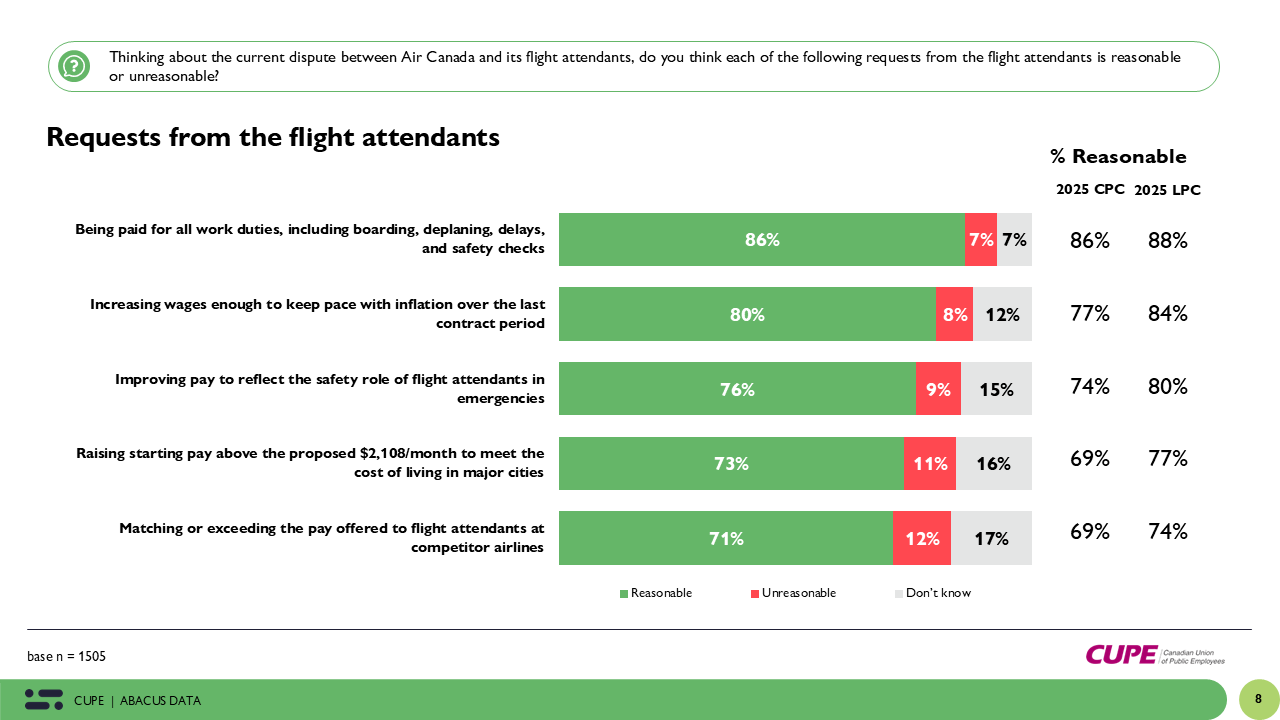

Reasonableness of Bargaining Demands

Across a series of bargaining asks tested, large majorities of Canadians see the flight attendants’ proposals as reasonable.

Being paid for all duties is supported by more than eight in ten.

Raising starting pay to meet the cost of living in major cities is supported by about seven in ten.

Increasing wages to keep pace with inflation over the last contract period has the backing of eight in ten.

Matching or exceeding competitor airline pay is supported by about seven in ten.

Improving pay to reflect the safety role of flight attendants in emergencies is supported by three-quarters of Canadians.

Liberal and Conservative voters are largely aligned on these issues, with only modest differences in levels of support.

Views on Wages and Affordability

When asked whether current entry-level wages are too low to live on in major cities, even after the company’s proposed raise, a majority say they are too low and should be increased. Only about one in five think the wages are fair for the work involved.

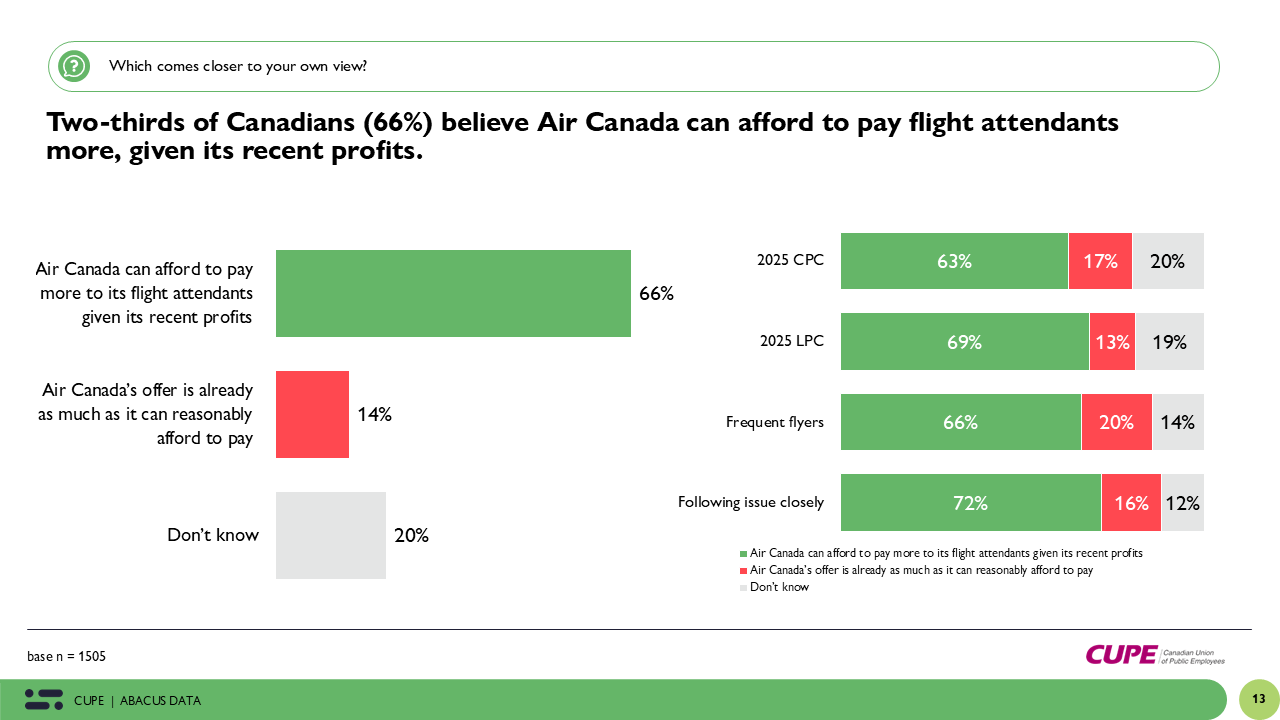

Similarly, two in three Canadians believe Air Canada can afford to pay more given its recent profits. This view is shared by 69% of Liberal supporters and 63% of Conservative supporters.

Federal Government Intervention

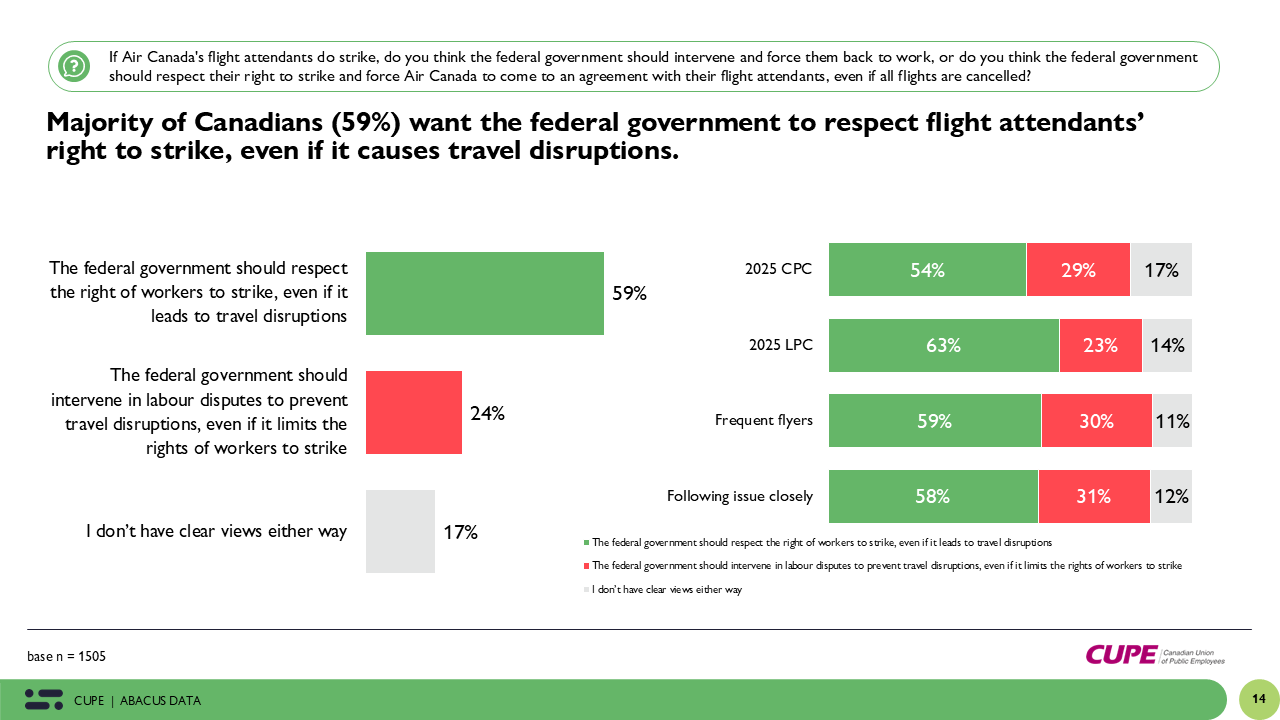

The public is also clear about the role the federal government should play if the dispute leads to a strike. A majority believe the government should respect the right of workers to strike, even if it causes travel disruptions. One in four think the government should intervene to prevent disruptions, and the rest are unsure.

While Conservative supporters are somewhat more likely than Liberals to favour intervention, most in both camps prefer that the government stay out of the dispute and let the parties reach their own agreement.

The Upshot

Public opinion is decisively aligned with the flight attendants. Large majorities, including those who voted for the Carney Liberals, believe their demands are reasonable, think Air Canada can afford to pay more, and support compensation for all aspects of their work. On the question of government intervention, Liberal voters are especially clear: nearly two-thirds say the federal government should respect the right to strike, even if travel is disrupted. This cross-partisan consensus, anchored by the Liberal base, leaves little political benefit in legislating an end to the dispute and considerable risk of alienating core supporters by doing so, especially since large majorities believe the flight attendants’ demands are reasonable.

Methodology

The survey was conducted with 1,500 Canadian adults from 12:00 pm ET on Thursday until 10:00 am ET Friday. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage potential skews in the data from a single source.

The data were weighted according to census data to ensure the sample matched Canada’s population by age, gender, educational attainment, and region. Totals may not add to 100 due to rounding.

The margin of error for a comparable probability-based random sample of the same size is +/- 3.3%, 19 times out of 20.

This survey was paid for by CUPE, the union representing Air Canada’s flight attendants.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

When we think about the future, our expectations shape more than our conversations — they influence how we plan, spend, save, vote, and adapt. In public opinion research, understanding what people believe is likely to happen matters because expectations can be as powerful as reality in driving behaviour. We plan our careers, make investments, choose where to live, and even decide which political leaders to support based not just on the world as it is, but the world as we think it will be.

But history, and human psychology, suggest we often get the timing wrong. As futurist Roy Amara famously put it, “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” While Amara was speaking about technology, the same principle applies more broadly: we can be quick to predict dramatic change in the next few years, yet slow to grasp how deeply those changes might reshape our lives over decades.

Our latest Abacus Data survey asked Canadians how likely they thought a range of events could happen in the next five years. The results reveal a mental map of the near future that blends technological disruption, geopolitical instability, environmental risk, and economic uncertainty. And when we compare across generations and political affiliations, striking differences emerge in how groups anticipate change, and, in light of Amara’s Law, where they may be getting the short-term and long-term wrong.

Cautious on Driverless Roads and Pilotless Skies

Nationally, there’s deep scepticism toward autonomous transportation. Only 15% think most trucks will be driverless within five years, and just 12% expect most passenger planes to operate without pilots.

Gen Z is more open to the idea. 23% see driverless trucks as likely and 22% say the same for pilotless planes. Boomers are almost entirely unconvinced: just 3% and 4%, respectively.

Among partisans, Liberal voters are slightly more optimistic (19% trucks, 16% planes) than Conservatives (13% trucks, 12% planes), though neither group sees widespread adoption as probable. While political leanings shift these numbers only marginally, age remains the biggest dividing line as younger Canadians are more prepared to see rapid technological adoption, older Canadians are not.

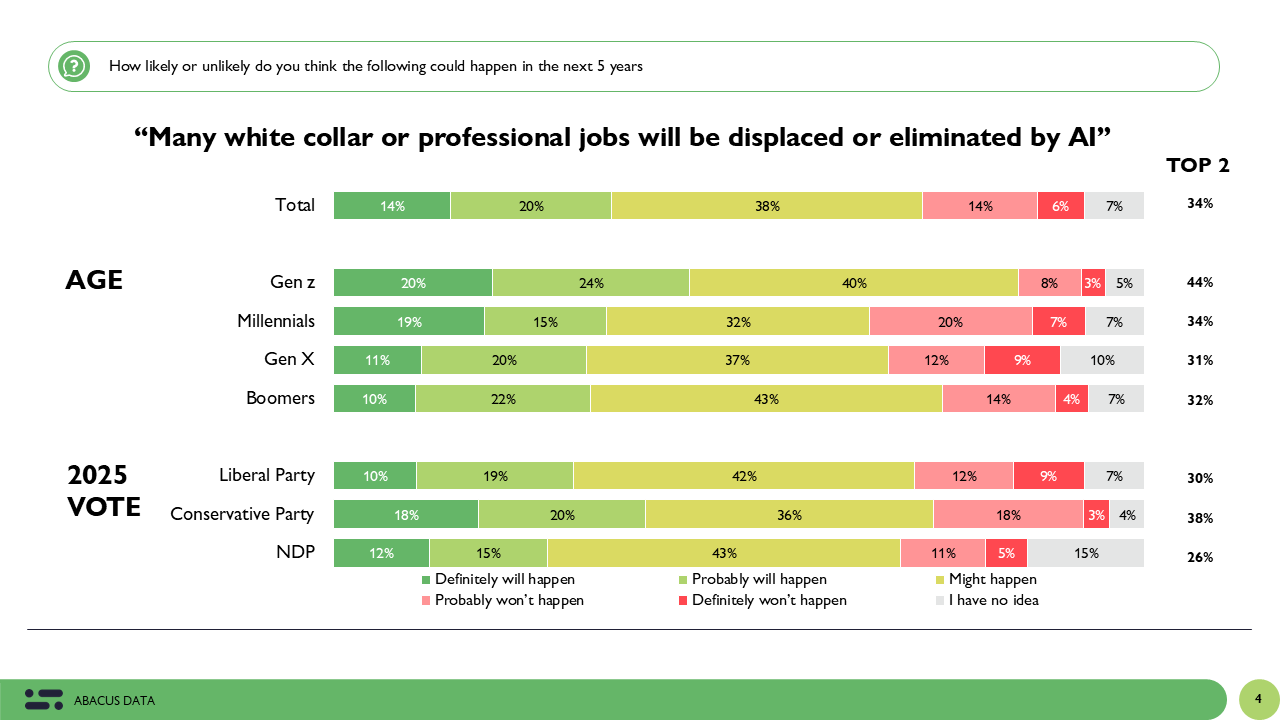

AI and the White-Collar Workforce

AI’s potential to reshape the professional job market is one of the most widely anticipated changes in the survey. A third of Canadians think significant white-collar job displacement will happen within five years, and nearly four in ten say it might.

Gen Z is most convinced, 44% say it’s probable, compared with 32% of Boomers. Political leanings shape this perception too: Conservative voters (38% likely) are more convinced than Liberal voters (30% likely) that AI will displace many white-collar jobs. The gap here may reflect different attitudes toward technological change and economic disruption with Conservatives perhaps more inclined to see competitive pressures and automation as unavoidable.

Geopolitical Flashpoints on the Horizon

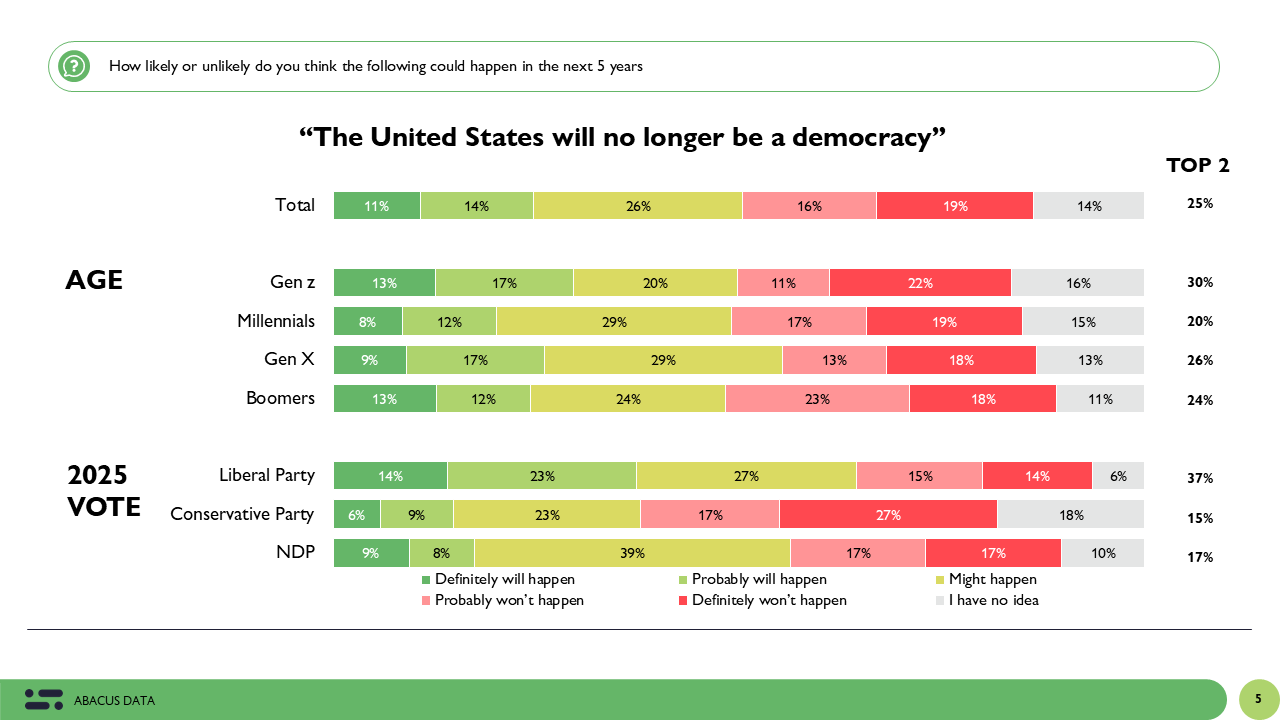

One in four Canadians believe the United States will no longer be a democracy within five years. Gen Z (30%) is slightly more likely than average to believe this, Boomers slightly less (24%). Liberal voters are substantially higher at 37%, while Conservatives are much lower at 15%. This is one of the most politically polarized questions in the survey — reflecting different perceptions of U.S. politics and the state of American democracy.

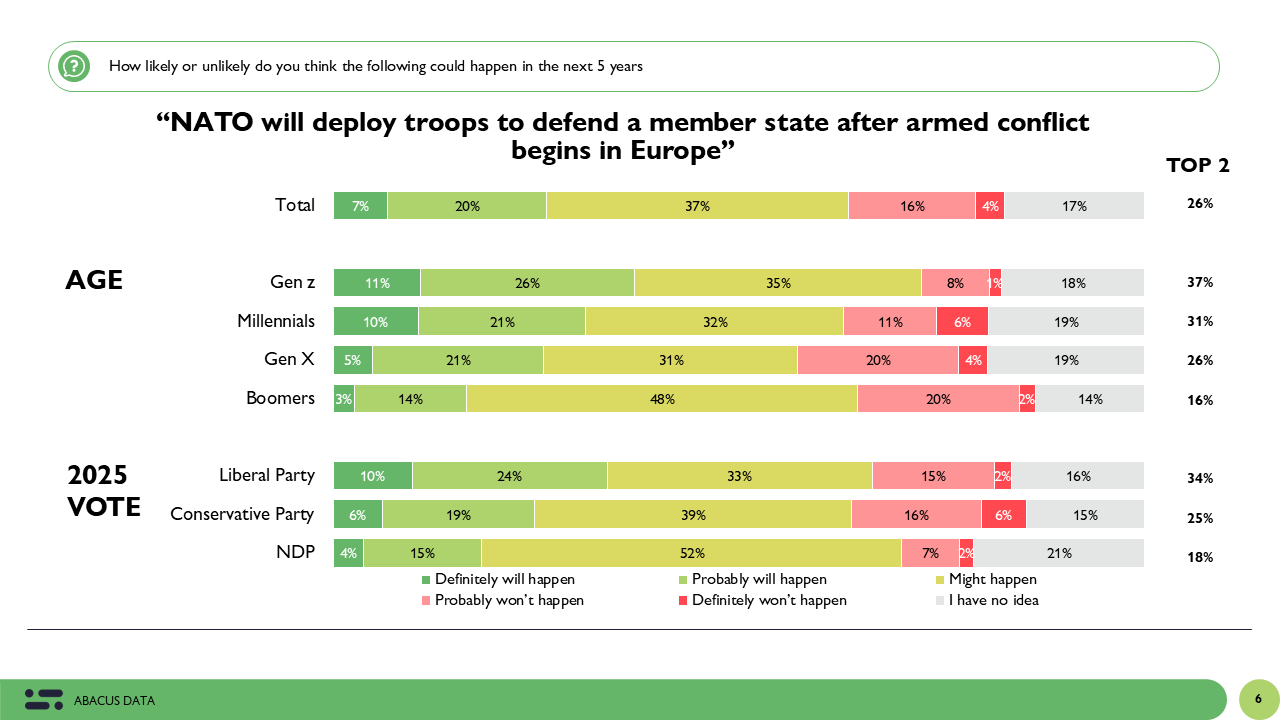

On NATO’s potential to deploy troops to defend a member state in Europe, Gen Z (37%) again leads, Boomers (16%) are more sceptical, and partisans split: Liberals at 34%, Conservatives at 25%. The partisan gap here may reflect differing views on Canada’s role in global alliances.

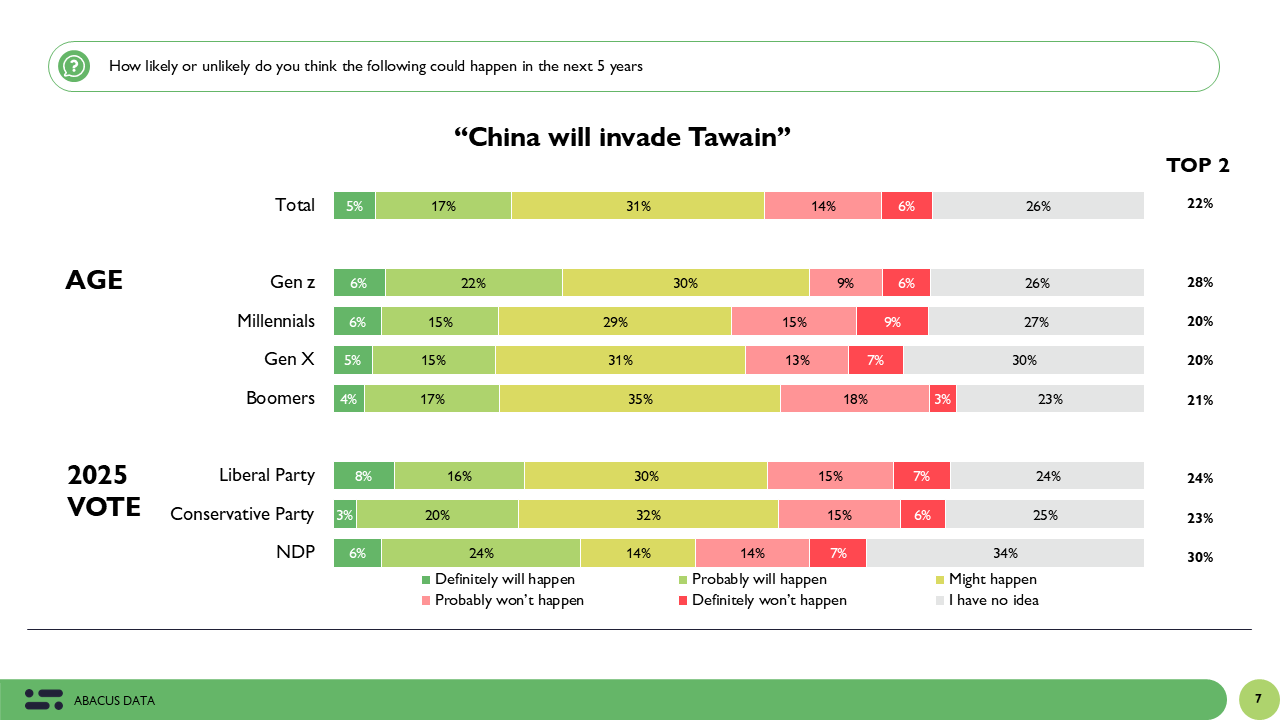

On a potential China–Taiwan conflict, the national average is 22% likely. Liberals (24%) and Conservatives (23%) are nearly identical here, though Conservatives have a slightly higher share saying “don’t know” (25% vs. 24% for Liberals).

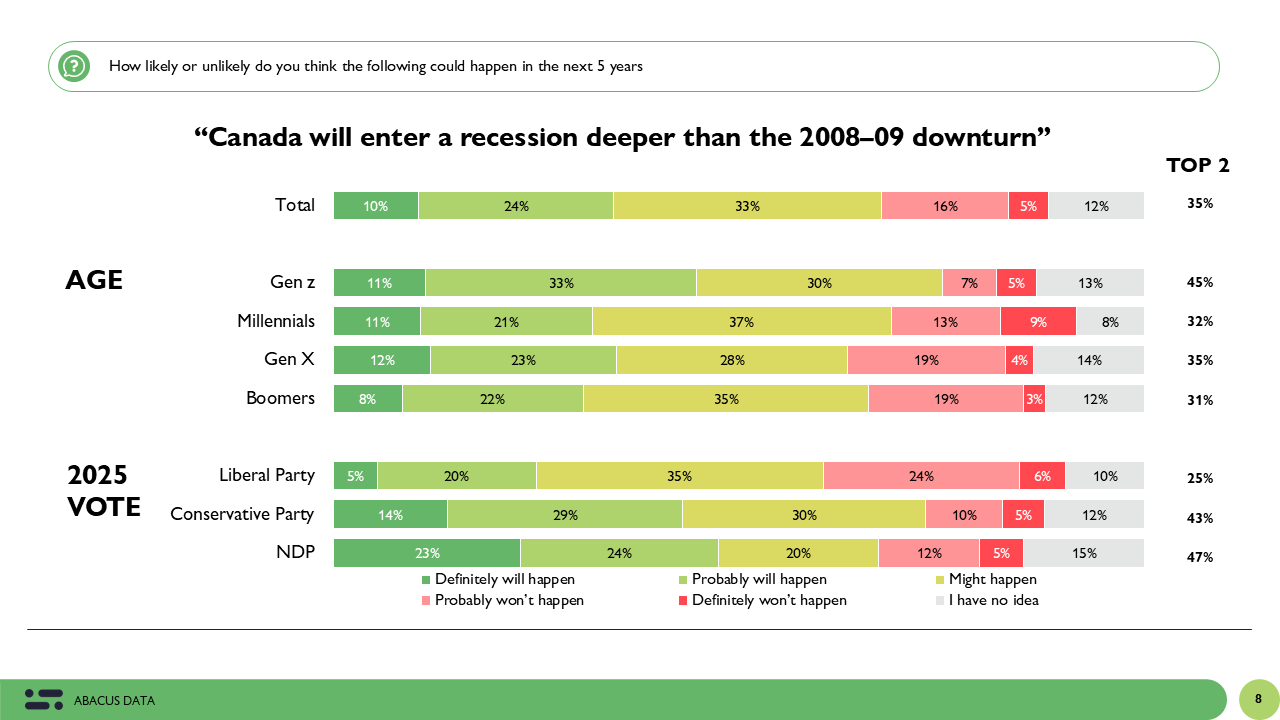

Economic Risks: Recession Feels Possible, Housing Crash Less So

Nationally, 35% believe Canada will face a recession deeper than 2008–09. Gen Z is most pessimistic (45%), Boomers less so (31%). Partisan leanings matter here: Conservative voters are much more likely to expect a deep recession (43%) than Liberals (25%). This likely reflects different levels of confidence in the current government’s economic management.

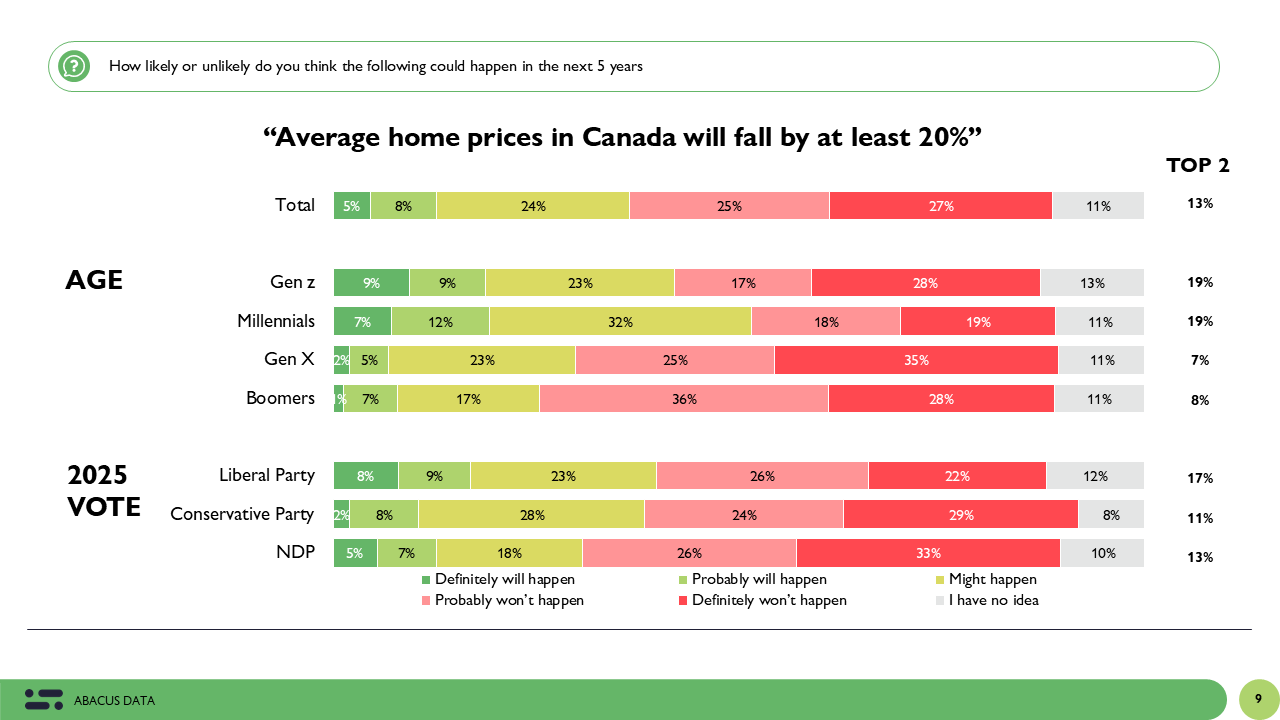

On housing, only 13% nationally think prices will fall by 20% or more in the next five years. Gen Z is somewhat more open to the idea (19%) than Boomers (8%). Among partisans, Liberals are at 17%, Conservatives lower at 11%. This small partisan difference is overshadowed by a much larger age divide with older Canadians remain far more confident in housing market stability.

Climate Change and the Cost of Risk

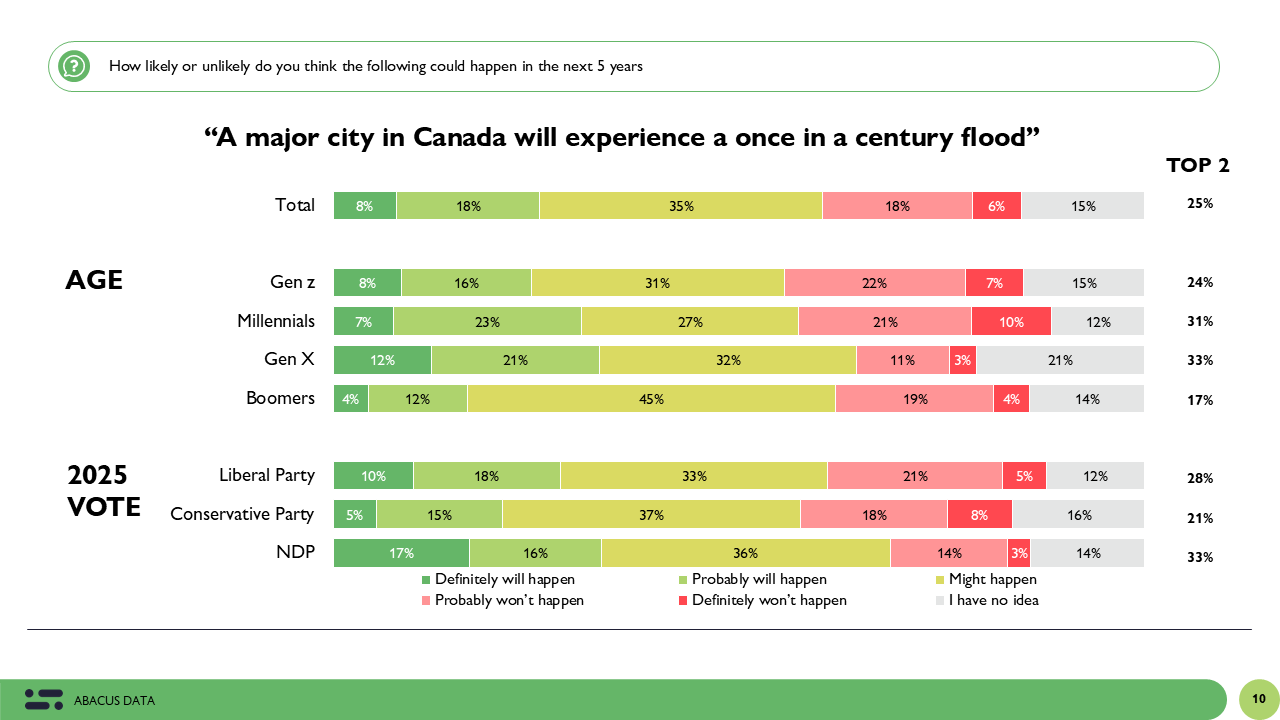

One in four Canadians believe a major Canadian city will experience a once-in-a-century flood within five years. Gen Z is slightly below average (24%), Boomers below that (17%). Partisan differences are sharper: Liberals (28%) are more likely than Conservatives (21%) to see this happening.

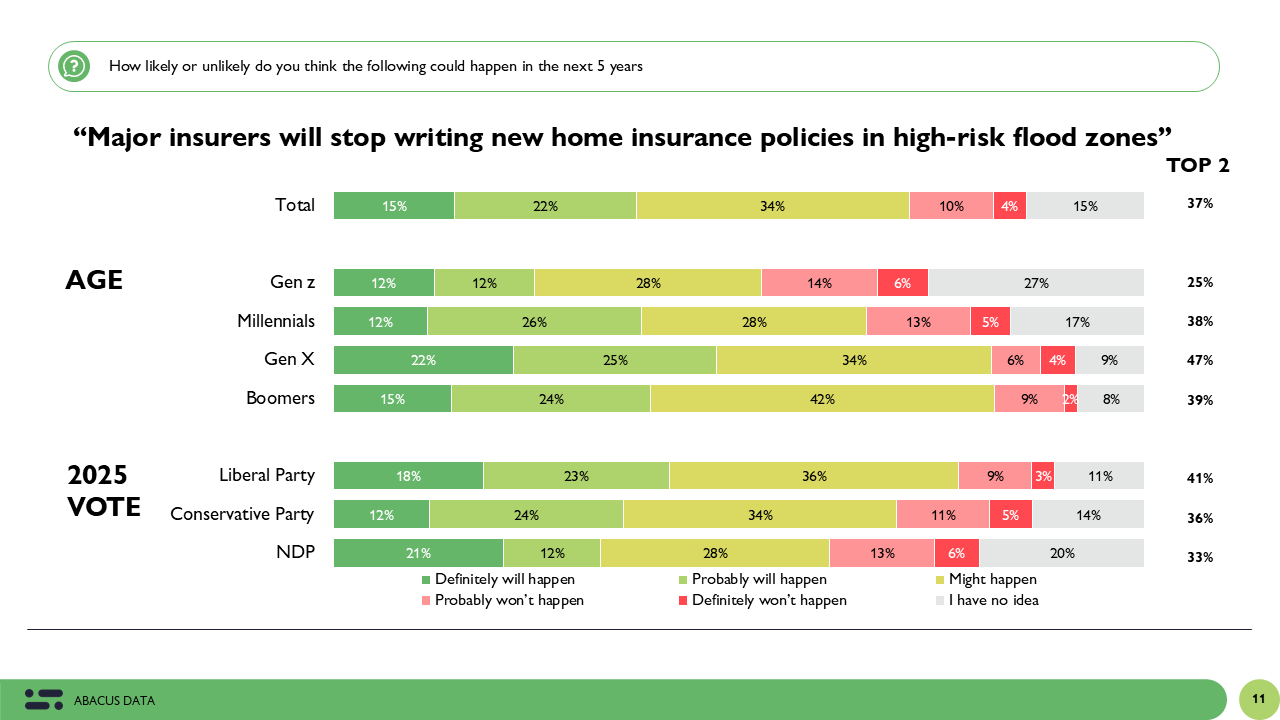

On insurance market impacts, 37% nationally expect major insurers to stop writing new home insurance policies in high-risk flood zones. Boomers are slightly above average at 39%, Gen Z is lower at 25%. Partisan divides are again notable: Liberals lead at 41%, Conservatives close behind at 36%. While both groups see this as a plausible development, Liberals appear more convinced that climate-related market changes will arrive quickly.

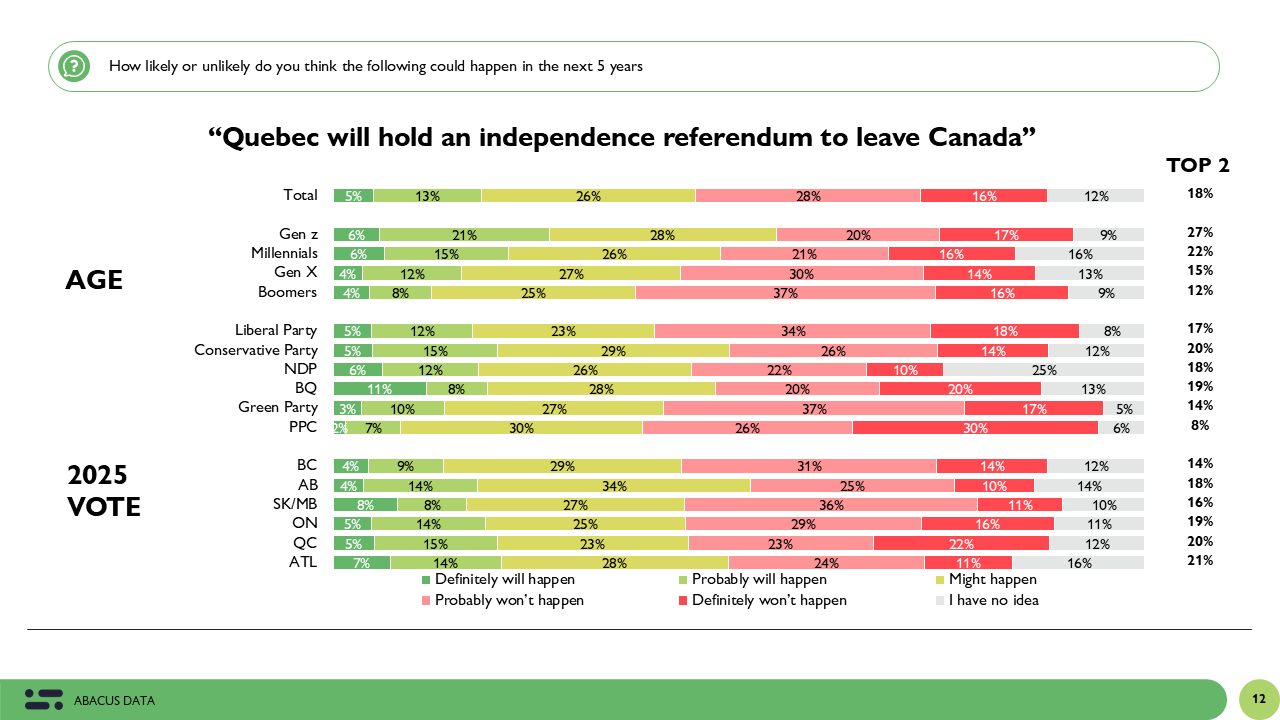

Quebec Independence Expectations

When asked whether Quebec will hold an independence referendum within the next five years, Canadians are more inclined to doubt it than to believe it will happen. Nationally, 18% think such a vote will “definitely” or “probably” take place, 26% say it “might happen,” and 43% believe it probably or definitely will not happen. Another 12% say they have no idea.

Generationally, younger Canadians are far more open to the possibility. Among 18- to 29-year-olds, 27% think a referendum is likely and another 28% think it might happen, leaving just over a third (37%) who think it won’t. Support for the likelihood drops steadily with age with only 12% of those 60 and over believe a vote will be held, while a majority (53%) dismiss the idea outright.

Regionally, expectations vary, though not as dramatically as one might think. Quebecers themselves are somewhat more likely than average to expect a referendum (20% likely, 23% might happen), but a similar share in Atlantic Canada (21%) also see it as probable. British Columbia (14%) and Saskatchewan/Manitoba (16%) are least likely to see a vote as imminent. Across all provinces, “might happen” responses are common, signalling that while Canadians don’t necessarily expect a referendum, they aren’t ruling it out entirely.

Politically, views are more polarized. Conservative voters (20% likely) are somewhat more inclined than Liberals (17%) to believe a referendum will occur, while Bloc Québécois supporters are, unsurprisingly, higher at 19% “likely” and 28% “might happen.” The strongest dismissal comes from Green Party voters (54% unlikely) and People’s Party supporters (56% unlikely). Among NDP voters, just 18% think a referendum will happen, though a quarter say they have no idea, the highest uncertainty among major federal parties.

This pattern, where a majority of Canadians either reject or are unsure about the possibility, suggests that while Quebec sovereignty remains a political undercurrent, it is not a widely anticipated near-term event. However, the higher likelihood placed on it by younger Canadians is notable. If this perception persists, it could shape how future political leaders frame national unity and constitutional debates.

Summary of the Landscape

When you step back, a clear pattern emerges. Age is the strongest driver of differences in future expectations. Younger Canadians are more open to the rapid adoption of new technology, more convinced AI will reshape work, and more pessimistic about economic stability. Older Canadians tend to be more sceptical about technological disruption, more confident in housing market stability, and less certain about major geopolitical change.

Political affiliation shapes the lens through which people view geopolitical and economic risks. Liberal voters are more likely to see threats to democracy in the U.S., anticipate climate-related disruptions, and expect NATO involvement in conflict. Conservative voters are more inclined to foresee a deep recession, more convinced about AI-driven job losses, and less likely to believe U.S. democracy will fail.

On issues like autonomous transportation and housing market collapse, there is cross-partisan consensus both Liberals and Conservatives are sceptical about rapid change. But on democracy, climate, and economic outlook, political identity pulls expectations in different directions.

Why Expectations Matter — and the Implications

Expectations aren’t idle speculation, they shape decisions in the present.

If Canadians believe AI will disrupt the workplace, they may invest in re-skilling, avoid certain career paths, or push for stronger regulation. If they expect climate risks to reshape insurance markets, they might alter home-buying decisions or demand infrastructure upgrades. If they anticipate geopolitical instability, they may support higher defence spending or leaders who promise stability.

From a consumer behaviour standpoint, younger Canadians’ higher expectations for technological and economic change suggest greater openness to new tools and wariness about long-term commitments. Older Canadians’ scepticism toward rapid change, especially in transport and housing, points to more stable consumption patterns. Liberal voters’ heightened expectations on climate and geopolitical risk could translate into stronger support for related policy action, while Conservatives’ greater recession fears may align with calls for fiscal restraint and economic policy change.

In employment planning, Gen Z’s stronger belief in AI-driven job loss suggests greater receptivity to training programs, while Conservatives’ slightly higher AI displacement expectations may influence business investment strategies differently than among Liberal-leaning firms.

For financial planning, Boomers’ faith in housing stability reinforces real estate as a store of wealth, while Gen Z’s more open view to a possible correction may influence their investment mix. Liberals’ higher climate-risk expectations could affect decisions on property location, insurance, and asset diversification, while Conservatives’ recession expectations may lead to more conservative investment portfolios.

In politics, these differences matter. The Liberal base appears more attuned to global democratic risk, climate-driven economic changes, and NATO’s potential role in conflict. Conservatives are more focused on economic vulnerability and AI disruption. These different mental maps of the next five years will influence which issues rise to the top in public debate and shape the policy agendas parties choose to champion.

But there’s another dimension: what happens if expectations are wrong?

If AI and automation evolve more rapidly than most Canadians anticipate, industries, workers, and governments could face sudden skill mismatches, mass displacement, and public anxiety. The pace of policy and training responses might lag, leading to sharper economic and social shocks.

If major geopolitical changes such as the collapse of U.S. democratic institutions, a new European conflict, or an unexpected escalation in Asia occur faster or more dramatically than expected, public opinion could shift overnight. Such events could reorder political priorities, reshape alliances, and cause rapid changes in consumer and investor confidence.

Shocks like these, where the future unfolds faster or more dramatically than people imagine, often have outsized impacts because they disrupt not only the real-world situation but also the psychological and strategic assumptions people have been using to make decisions. This is why measuring and tracking expectations matters: it’s not just about predicting the future, but about preparing for the emotional and behavioural turbulence that comes when reality departs sharply from what people believed was likely.

The future will not unfold exactly as any group expects, but the way Canadians imagine it today will shape how they prepare, respond, and adapt. For leaders in business, government, and advocacy, understanding these expectations and planning for what happens if they’re wrong, is essential to anticipating both market shifts and political currents.mer wears on, it’s the economy, not foreign affairs, that could add more complexity to the political climate heading into fall.”

METHODOLOGY

The survey was conducted with 1,686 Canadians from July 31 to August 7, 2025. A random sample of panelists were invited to complete the survey via partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.4%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, and region. Totals may not add up to 100 due to rounding.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

I’m thrilled to share that Oksana Kishchuk has been promoted to Vice President, Insights at Abacus Data.

Oksana has been a driving force behind some of our most important and impactful work. She leads our agriculture and agri-food practice, guides projects in post-secondary education, youth engagement, and healthcare, and heads our federal government public sector work.

Her ability to combine curiosity with a deep understanding of our clients’ needs has helped us grow existing relationships and build new ones.

With nearly a decade of experience in market research, Oksana has a rare talent for asking the right questions, designing thoughtful research plans, and delivering insights that clients can act on today and in the future.

Her leadership, collaborative spirit, and commitment to quality reflect the best of what Abacus stands for.

Please join me in congratulating Oksana on this well-deserved promotion. You can reach out to her by email and follow her on social media.

— David Coletto Founder & CEO, Abacus Data

ABOUT ABACUS DATA

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

From July 31 to August 7, 2025, Abacus Data surveyed 1,686 Canadian adults on the state of federal politics. The polling occurred primarily after Canada and the United States failed to reach a new trade and security agreement before the self-imposed August 1 deadline, a moment that might have sparked public reaction, but instead revealed just how steady Canadian political attitudes remain.

Despite the geopolitical uncertainty, Canadians appear largely unmoved in their federal political preferences. Government approval has dipped slightly, but vote intentions are static, and the desire for change remains stuck in neutral.

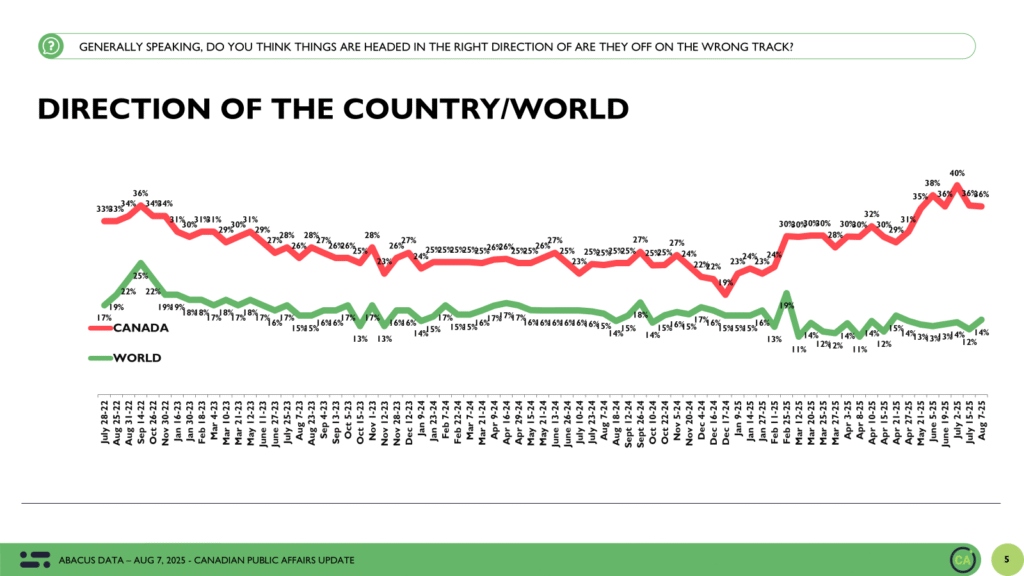

Direction of the Country: No Panic, No Rally

Just 36% of Canadians believe the country is headed in the right direction, the same as in mid-July. Meanwhile, 46% think the country is off on the wrong track, a stable but still elevated level of pessimism. These results suggest Canadians are watching the stalled U.S. negotiations with concern, but not with alarm.

Views about the world remain bleak (14% right direction), as do impressions of the United States (14%), reflecting persistent unease about President Trump’s second term and America’s unpredictable posture on trade and global leadership.

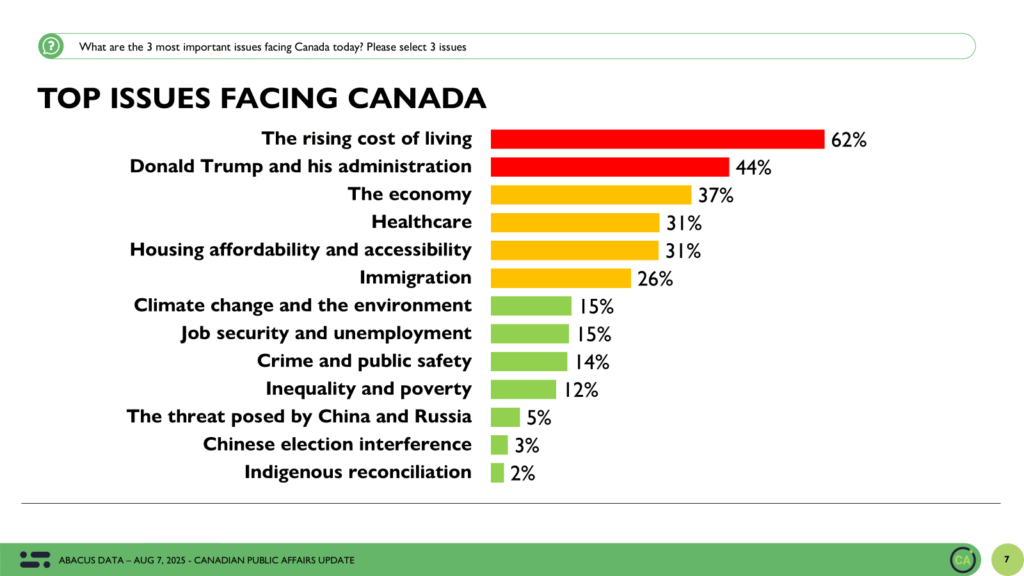

Top Issues: Trump Ticks Up, Housing Drops Back

The rising cost of living remains the dominant issue, cited by 62% of Canadians, up modestly from 59% in the previous wave. Donald Trump and his administration remain the second-most-mentioned concern, rising slightly to 44% (from 43%), further evidence that American politics continue to deeply shape Canadian anxieties.

The broader economy is a close third at 37% (up 1), while housing affordability and accessibility has dropped slightly, from 35% to 31%. Healthcare also edged down to 31%, from 33% two weeks ago.

These shifts, while small, reinforce a political climate shaped by affordability fatigue and international turbulence. The Trump presidency has become a durable second-tier issue, not displacing domestic worries, but consistently competing with them.

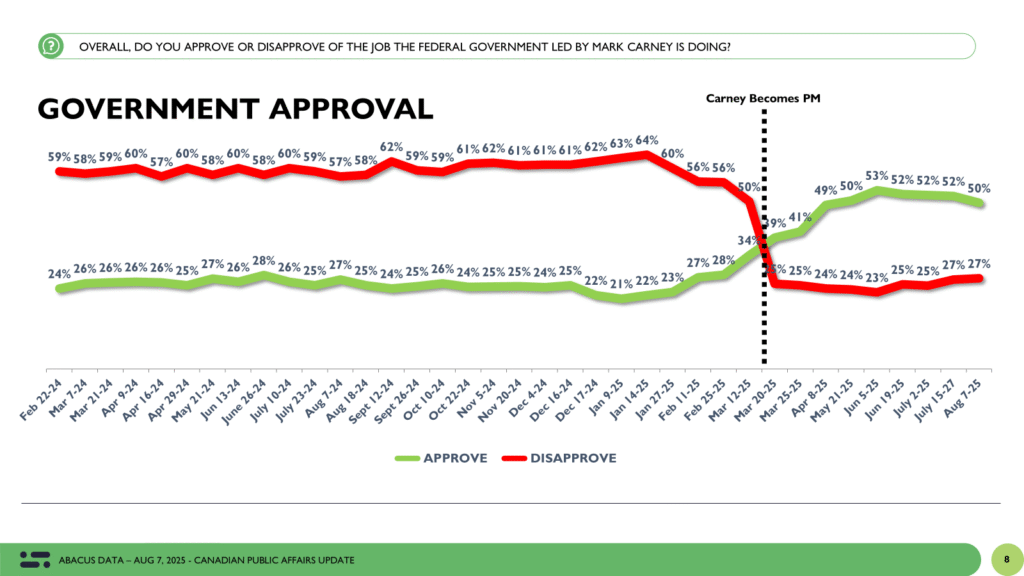

Government Approval: A Small Dip, But Still Majority Support

Approval of the Carney-led federal government now stands at 50%, down two points since mid-July. Disapproval is unchanged at 27%. This marks the first time since March that approval has touched the 50% line, suggesting a mild cooling-off following a long stretch of goodwill.

While the overall balance remains positive, the drop likely reflects concerns about the lack of progress on key domestic files and a perceived absence of resolution in high-profile international negotiations.

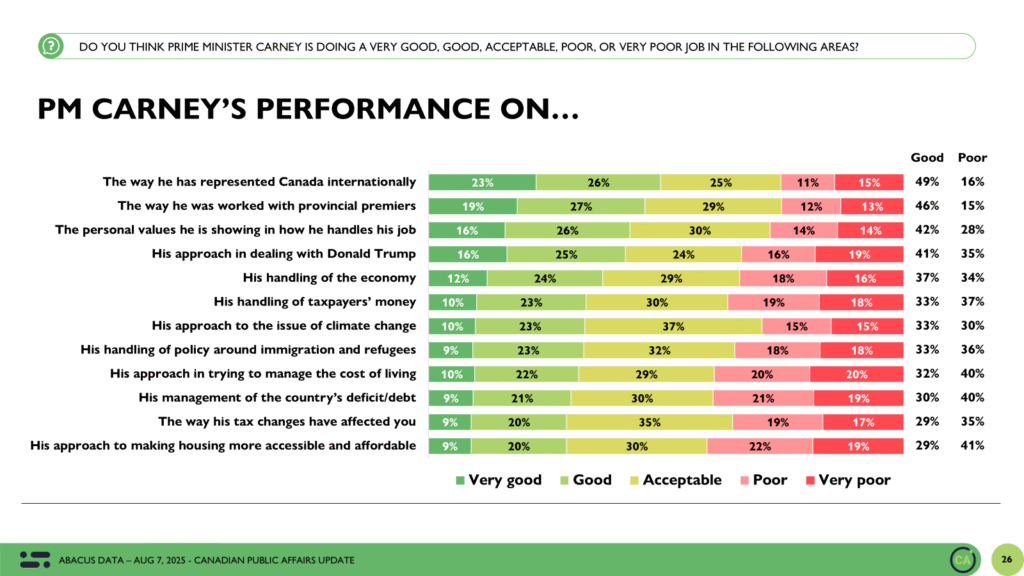

Performance Measures: Strengths Abroad, Weaknesses at Home

Mark Carney continues to earn his strongest marks on files tied to diplomacy and governance:

Representing Canada internationally: 49% good/very good

Working with premiers: 46% good/very good

Handling Donald Trump: 41% good/very good

But when it comes to domestic economic issues, perceptions turn sharply:

Housing affordability: 41% poor/very poor vs. 29% good

Cost of living: 40% poor/very poor vs. 32% good

Handling taxpayer money: 37% poor/very poor vs. 33% good

Deficit and debt: 40% poor/very poor vs. 30% good.

While the public gives Carney credit for his tone, values, and international steadiness, many remain unconvinced that progress is being made where it matters a lot, in their household budgets.

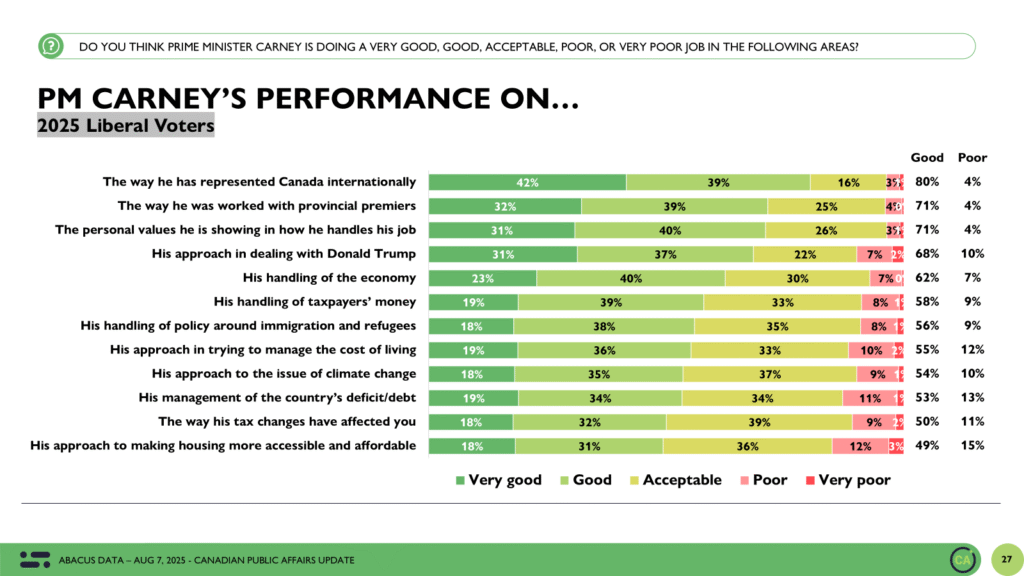

Among Canadians who voted Liberal in 2025, approval levels are markedly higher across every file. Fully 80% say Carney has done a good or very good job representing Canada internationally, 71% say the same about his work with premiers and the values he brings to the job, and 68% approve of his handling of Donald Trump. Even on weaker areas like housing and cost of living, Liberal voters are more forgiving, with about half rating his performance positively, though these remain the lowest-scoring files even among his base. This suggests that while the Prime Minister enjoys deep goodwill among his supporters, expectations on domestic affordability remain a live test heading into the fall.

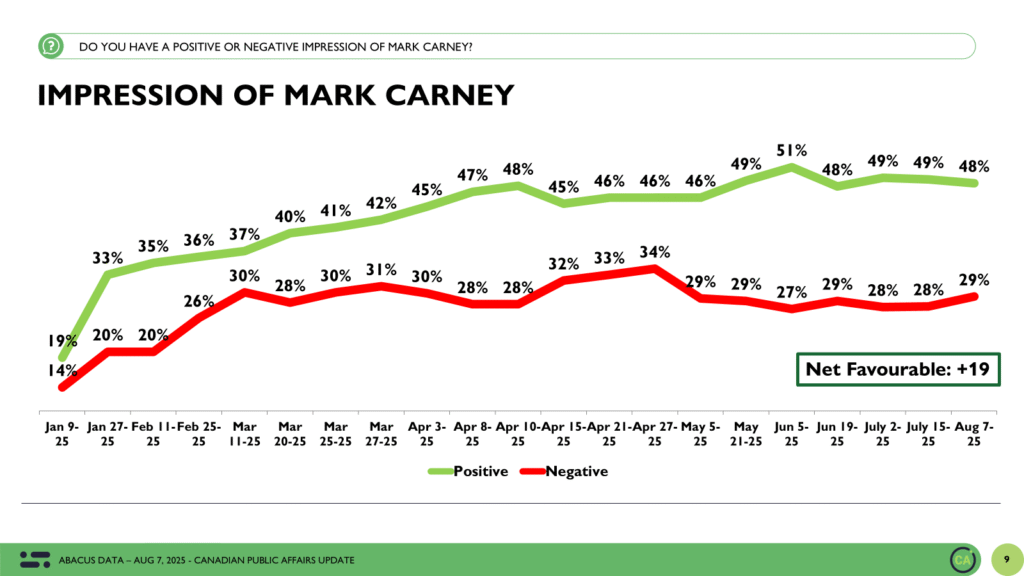

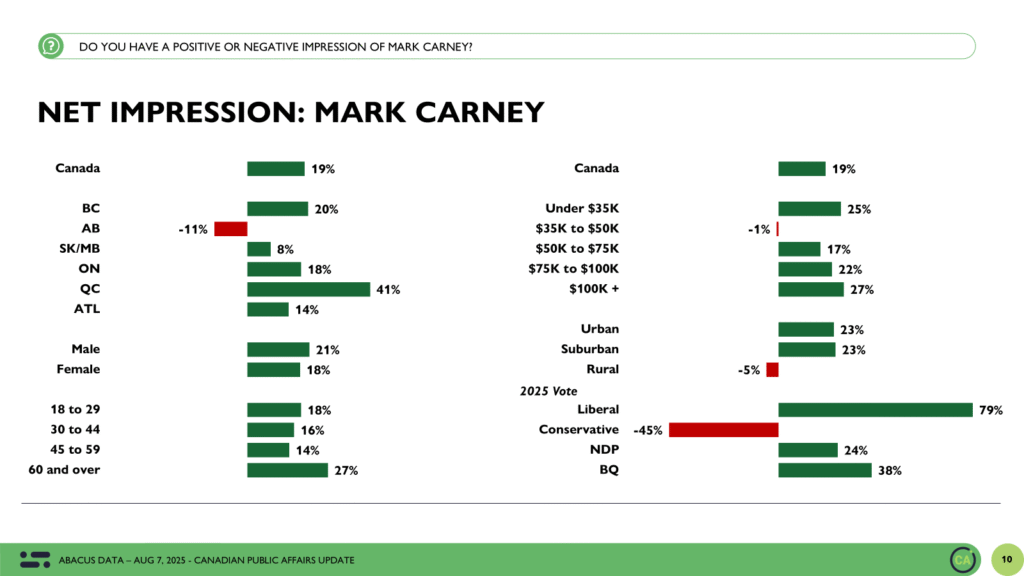

Leader Impressions: Carney Holds Ground, Poilievre Breaks Even

Mark Carney remains in positive territory, with 48% viewing him favourably and 29% unfavourably for a net score of +19. These numbers are down slightly from July but remain strong, particularly in Quebec (+41), BC (+20), and Ontario (+18), and among older voters.

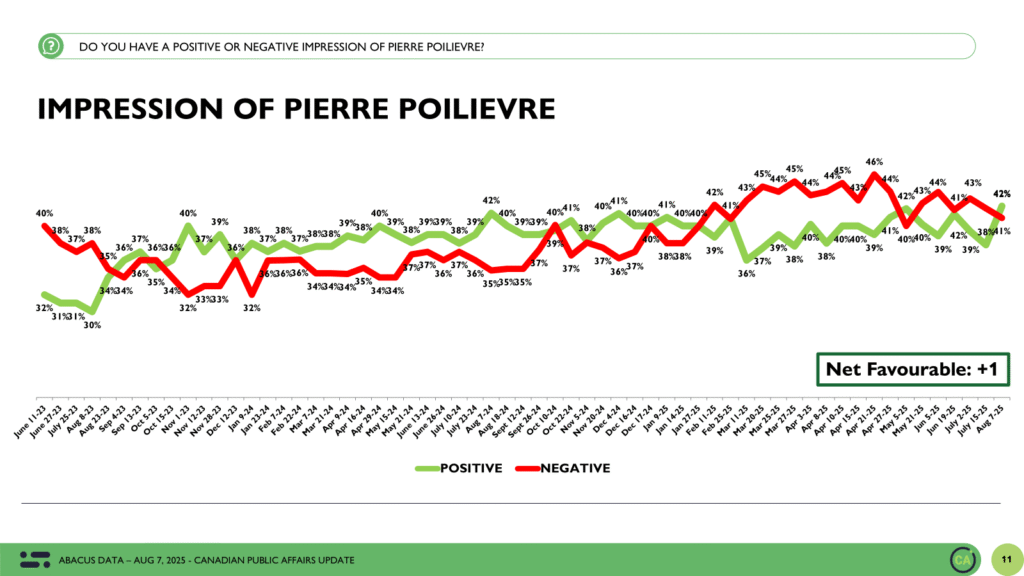

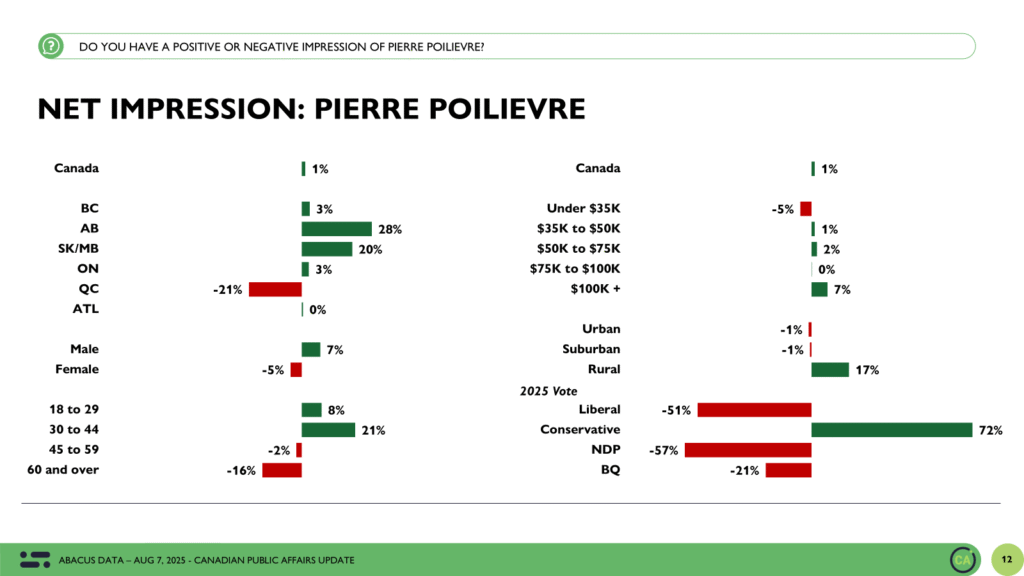

Pierre Poilievre, meanwhile, has reached a rare balance: 42% positive, 41% negative, for a net score of +1. This is his best net rating in months.

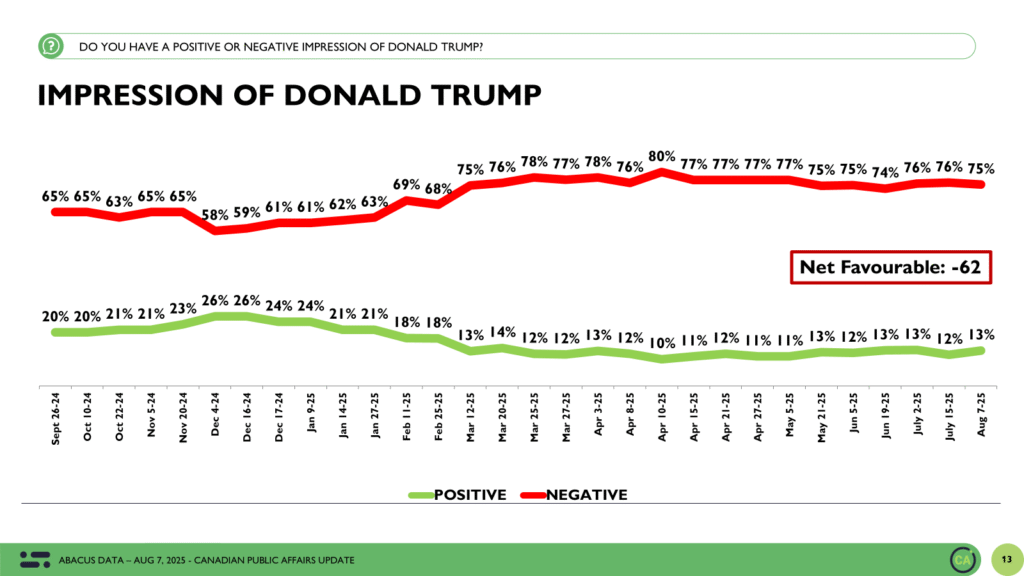

Donald Trump remains deeply unpopular in Canada: 13% favourable, 75% unfavourable, a net of -62, virtually unchanged.

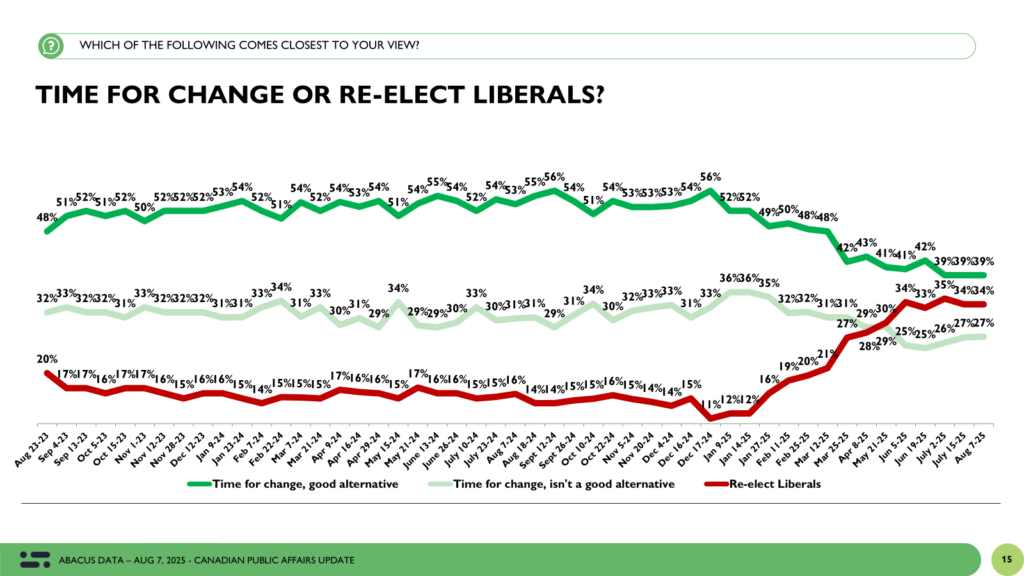

Desire for Change: A Story on Pause

Views about change in government remain unmoved. Four in ten (39%) of Canadians believe it’s time for a change and see a good alternative. Another 27% want change but don’t see a viable option. Meanwhile, 34% say the Liberals under Carney deserve re-election, steady from the last wave and the highest that figure has been in two years.

In short: no new movement, no new momentum.

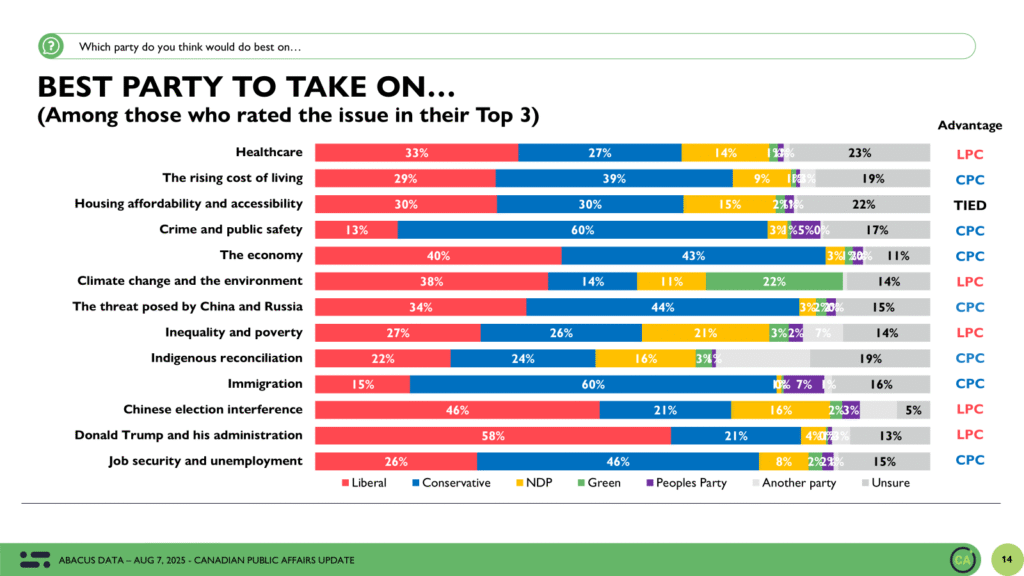

Issue Ownership: A Divided Map

When asked which party is best equipped to handle the issues they care most about, Canadians continue to divide along familiar lines.

Cost of living: Conservatives 39%, Liberals 29%

Donald Trump and his administration: Liberals 58%, Conservatives 21%

On immigration, the Conservative lead remains stark: 60% of those who prioritize it believe the CPC is best suited to handle the issue, compared to only 15% for the Liberals.

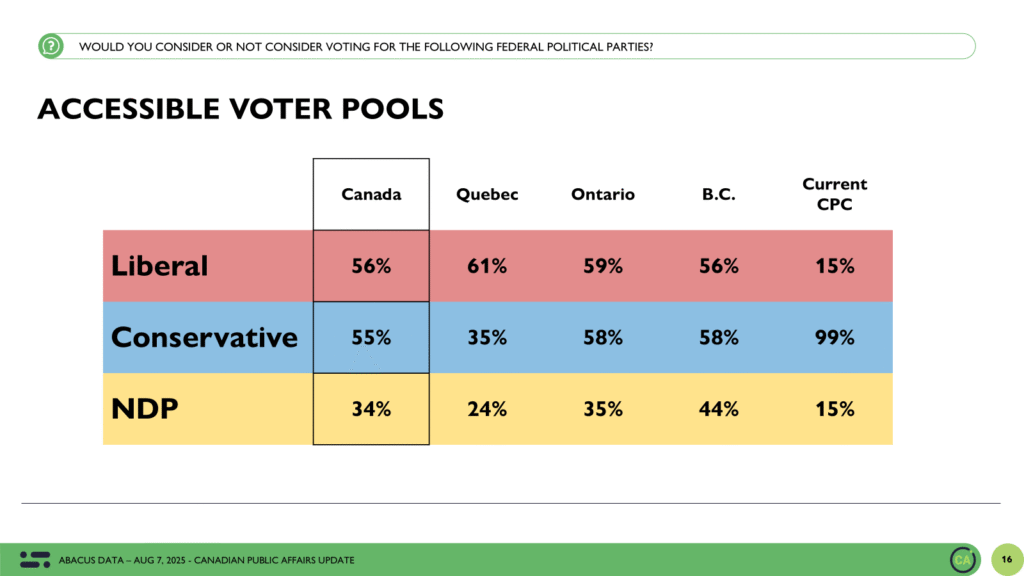

Accessible Voter Pools: Liberals Still Edging Out Conservatives

The accessible universe for the Liberal Party sits at 56%, virtually unchanged from last wave. The Conservatives remain close behind at 55%. Regionally, the Liberals maintain an edge in Ontario and Quebec, while the Conservative pool is wider in the West. The NDP lags significantly behind, at 34% nationwide.

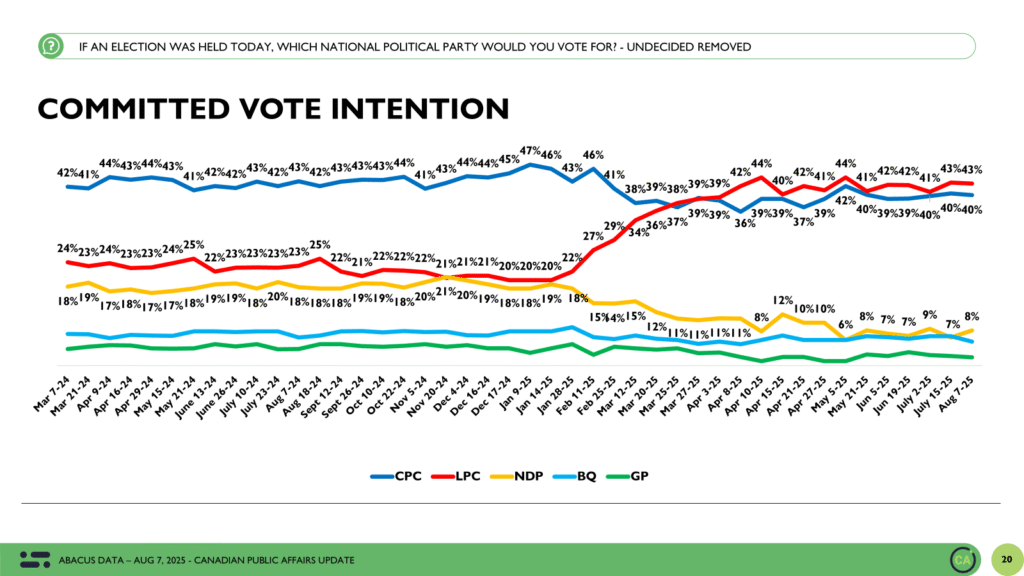

Vote Intention: Still Deadlocked

If an election were held today, 43% of decided voters would cast a ballot for the Liberals — no change since mid-July. The Conservatives also hold steady at 40%. The NDP stands at 8%, the Bloc Québécois at 6%, with the Greens and PPC both between 1% and 2%.

Among those certain to vote, the Liberal advantage increases slightly to 44% vs. 40% for the Conservatives.

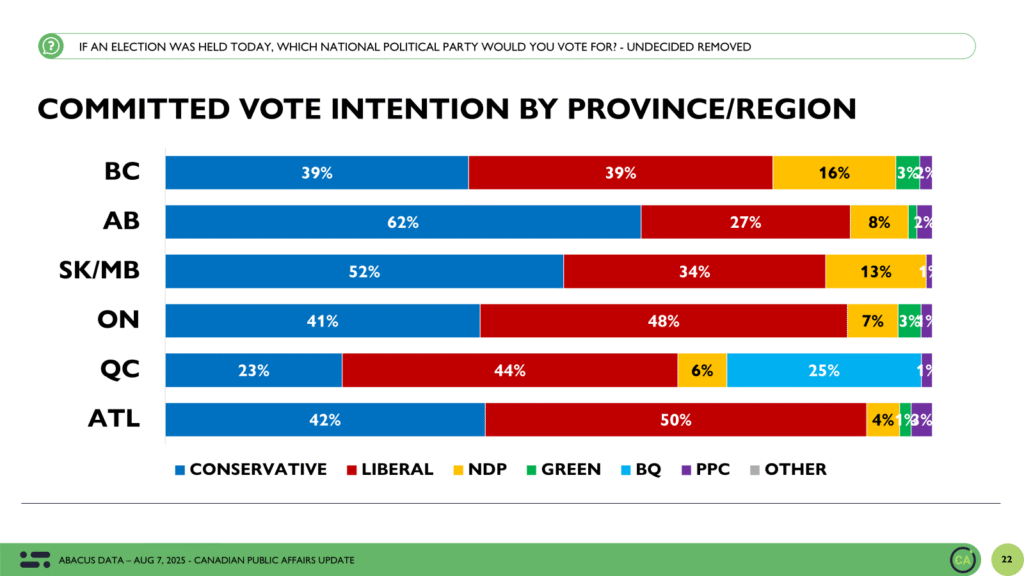

Regionally:

British Columbia: A tie: 39% each for the Liberals and Conservatives, with the NDP at 16%

Ontario: Liberals lead 48% to 41%

Quebec: Liberals at 44%, Bloc at 25%, Conservatives at 23%

Atlantic Canada: Liberals ahead 50% to 42%

Alberta: Conservatives lead with 62%, Liberals at 27%

Saskatchewan/Manitoba: Conservatives at 52%, Liberals at 34%

Demographic Trends: Familiar Patterns Persist

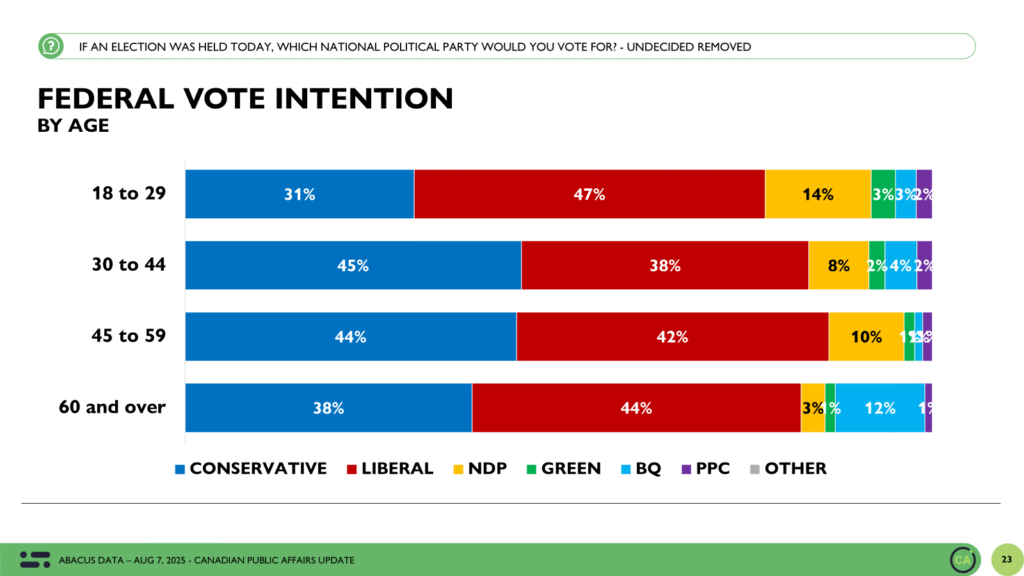

The Liberal advantage remains strong among younger voters (47% among 18–29s), while the Conservatives lead with middle-aged Canadians (45% among 30–44s) and those over 50 (44% to 38%).

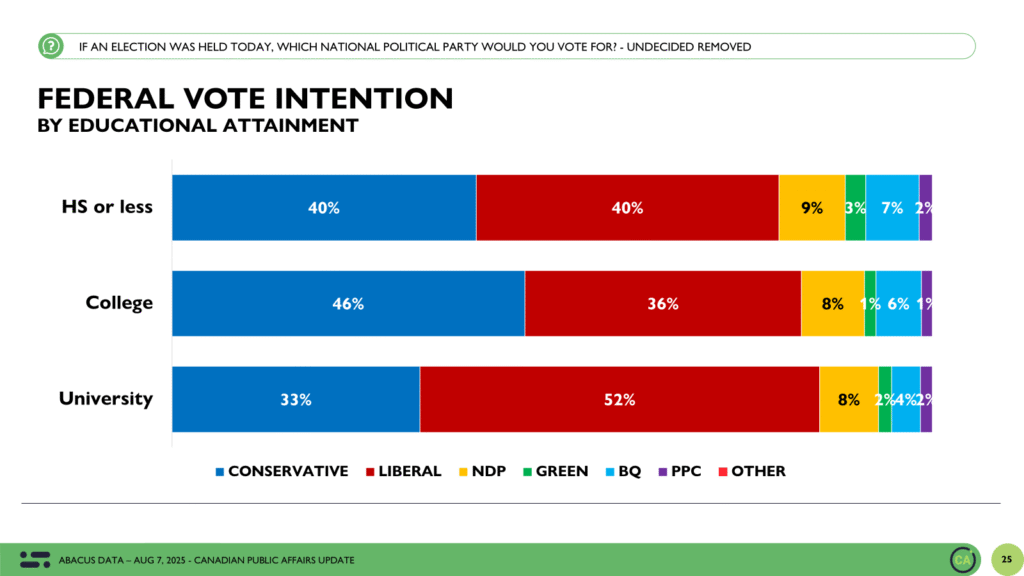

Women lean Liberal (45% to 38%), while men are split more evenly. Among university-educated voters, the Liberals lead by 19 points (52% to 33%), but the Conservatives are ahead among those with a college degree (46% to 36%).

The Upshot

According to Abacus Data CEO David Coletto: “As the deadline for a new Canada–U.S. agreement came and went with no breakthrough, Canadians didn’t blink. Support for the governing Liberals remains strong, vote intentions haven’t moved, and the desire for change is static.

The Carney government retains a solid approval base and a reputation for international competence. But there are signs of drag: its domestic economic ratings are showing wear, and the Prime Minister’s halo on affordability issues may be beginning to dim.

For now, Canadians are separating frustration with outcomes from blame toward the government. But that separation may not last forever. As summer wears on, it’s the economy, not foreign affairs, that could add more complexity to the political climate heading into fall.”

Methodology

The survey was conducted with 1,686 Canadians from July 31 to August 7, 2025. A random sample of panelists were invited to complete the survey via partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.4%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, and region. Totals may not add up to 100 due to rounding.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

In our second deep dive into Canadian attitudes toward artificial intelligence, we turn our attention to AI’s growing role in the workplace. From July 10 to 15, 2025, Abacus Data surveyed 1,915 Canadian adults to understand how they perceive the impact of AI on their jobs and careers. As AI adoption accelerates across the country, Canadians are experiencing a mix of anxiety, curiosity, and cautious optimism. The findings reveal a workforce deeply divided – not just over whether AI will bring more opportunity or risk, but also over how prepared they feel for the changes on the horizon.

AI Anxiety Runs High

Nearly half of employed Canadians (47%) say they’re worried that AI and automation could soon force them to change their job or career. But this concern isn’t evenly spread – it’s most intense among young adults, with 55% of those aged 18-29 expressing anxiety about needing to shift careers within the next five years. People who are already familiar with AI are also more likely to worry (56%), perhaps reflecting a deeper understanding of how quickly workplace technology is evolving.

Most Expect Job Losses, and Many Don’t Feel Ready

The spectre of job loss is widespread – seven in ten employed Canadians believe that AI will make some jobs in their industry obsolete. And the feeling of being prepared to adapt to this new reality is split right down the middle: 50% say they feel ready, while the other half feel unprepared.

Readiness also follows demographic lines. Young adults (63% of those 18-29, 58% of 30-44) and men (54%) are more likely to say they feel equipped to handle the change, while older Canadians (68% of those 60+) and women (55%) are less confident. The biggest gap is between those who are familiar with AI (68% feel prepared) and those who aren’t – 80% of that group say they’re not ready for what’s coming. These findings underscore a real divide in how equipped Canadians feel to face the coming transformation.

Is AI an Opportunity or a Threat? Canadians are Split Down the Middle

Asked whether AI will bring more opportunities than risks to their workplace in the next five years, Canadians are perfectly divided: 49% see the upside, while 51% remain unconvinced. But optimism is more common among men (53%), Canadians aged 30-44 (56%), and those familiar with AI (61%). In contrast, women (58%), older Canadians (61% of 60+), and those who lack AI familiarity (71%) are more likely to view AI as a net risk. This deep split highlights the ongoing debate over whether AI will ultimately help or harm the Canadian workforce.

AI Training Is Still the Exception, Not the Rule

Despite all the anticipation – and anxiety – around AI, only about one in three employed Canadians (36%) report that their employer has encouraged, required, or provided any training to help them use AI tools at work. The vast majority are left to figure things out on their own, or not at all. For most workers, structured support to adapt to AI remains out of reach, potentially widening the skills gap in the years ahead.

A Clear Expectation: More Jobs Lost Than Created

When Canadians consider the bigger picture, pessimism outweighs optimism: 62% believe that AI will eliminate more jobs than it creates, with just 11% believing the opposite. There is a widespread expectation that AI’s impact on the labour market will be more about disruption and loss than new opportunities.

THE UPSHOT

The rise of AI in Canada is more than just a technological shift – it’s a moment of change for our workforce, our economy, and how secure Canadians feel about the future. Many are already feeling anxious about what AI could mean for their jobs and livelihoods, and those concerns are shaping conversations about work, learning, and trust in our institutions.

If these worries are left unaddressed, there’s a risk that progress could slow and divisions could widen. But there is also a real opportunity for leaders – across government, business, and the tech sector – to step up and guide Canadians through this transition. As AI continues to accelerate, people will look for answers and reassurance about how they will be supported and protected.

With open communication, investment in accessible training, and a commitment to inclusion, Canada can help ensure that everyone is prepared to adapt at their own pace and on their own terms. By working together and focusing on people, not just technology, we can help Canadians feel more confident about the future.

AI’s potential will be realized if we bring everyone along. The choices made now will help shape not only the future of work, but also our sense of community and resilience in a rapidly changing world.

METHODOLOGY

The survey was conducted with 1,915 Canadian adults from July 10 to 15, 2025. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.24%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

When people ask me what it’s like to work with Abacus Data, I tell them it’s a bit like flying business class for the first time: suddenly you realize how smooth and easy the journey can be when you’ve got the right partner looking after every detail.

We’re not a vendor.

We’re not just researchers.

We’re your co-pilot.

We help you ask better questions, uncover the truths and unmet needs others miss, and tell stories that resonate because we know the real value of research isn’t the data, it’s the decisions it helps you make and influence.

Our entire approach is built around something we call enlightened hospitality. It’s not just about timelines and deliverables, it’s about how we treat people. We lead every engagement with professionalism, warmth, and responsiveness. You’ll get clear roles, real-time transparency and constant updates that helps you feel confident, not left in the dark.

What makes this possible is our team. We try to live by a set of fundamentals – from “do the right thing, always” to “deliver enlightened hospitality” to “go beyond description and tell them what it means.” These aren’t just posters on a wall. They shape how we show up every day: thoughtful, curious, rigorous, and relentlessly focused on our clients’ success.

We obsess over quality. Every report, every dataset, every slide deck is a reflection of our standards and we sign our work in bold. If something doesn’t feel right, we double-check it. If a number moves in a tracking survey, we pause and ask, “Why?” We’re not afraid to flag issues or tell a client that the data isn’t ready because trust is built in those moments.

Our senior team is hands-on. When you work with Abacus, you’re not handed off to juniors. I still read the toplines, write the debriefs, and get into the weeds of every project that crosses my desk. I’m like that chef whose restaurant you excited to try for the first time. You want that chef cooking in the kitchen. That’s me along with Ihor, Eddie, Oksana, and others on our team. That’s how we ensure clarity, consistency, and depth in everything we do.

Our analysis blends data science and human insight. We use advanced analytics, AI-powered coding tools, and rigorous methods, but we always ground our findings in context and experience.

We don’t just say what the data shows. We explain what it means and how to act on it. That’s why our work gets noticed. It’s why governments, media, and major brands listen when we speak. And it’s why our clients often tell us, “That’s exactly what we needed to hear.”

But it’s not just about the insight, it’s about how we deliver it. We’ve designed our project management around making your job easier. You’ll always know what’s happening next, what we need from you, and when you’ll get the next deliverable. We anticipate roadblocks, solve problems without blame, and stay flexible to your shifting priorities.

We work across sectors – from retail to healthcare to housing to tech to labour to public policy – but what ties our work together is a deep understanding of human behaviour. We sit at the intersection of consumer, citizen, and worker attitudes, which gives us a 360° view of how people think and feel. That perspective helps our clients get ahead of emerging trends, identify unmet needs, and make bold, informed decisions.

We’re proudly independent and fiercely non-partisan. We don’t work for political parties, and we don’t skew the data to fit a narrative. Our job is to tell the truth, even when it’s inconvenient. That integrity has earned us the trust of organizations like the Canadian Medical Association, Google, WestJet, Interac, and many more.

At the heart of it all, we’re endlessly curious. We want to understand what’s changing, what people care about, and how our clients can lead through uncertainty. And we’re generous with what we learn, through briefings, webinars, media commentary, and day-to-day client work. We don’t hoard insight. We share it.

So if you’re looking for a research and strategy partner who will challenge your thinking, deliver clarity in a noisy world, and treat your problems like our own, then Abacus might be the right fit.

We are Canada’s most sought-after and influential full-service market and public opinion research agency.

But what we really do is identify the unmet needs of your audience and develop strategies for you to meet those unmet needs first.

Through qualitative and quantitative research methods, our deep experience and and wide perspective, we ask the right questions that capture insights, show you where things are going to be, and help our clients navigate some of their biggest challenges, deepen relationships with customers and stakeholders, and better understand the road ahead.

About David Coletto

David is one of Canada’s best known and most respected public opinion analysts, pollsters, and social researchers. He works with some of North America and Europe’s biggest and most respected brands, associations, and unions andis frequently called upon by news organizations, to assess public opinion as events happen.

In January 2024, The Hill Times recognized him as one of the Top 100 Most Influential People in Canadian Politics noting, “when David Coletto releases polling numbers, Ottawa listens.”

Contact us with any questions

Find out more about how we can help your organization by downloading our corporate profile and service offering.

New Abacus Data research reveals Canadians have clear expectations for their leaders and Mark Carney currently aligns more closely with those expectations than Pierre Poilievre.

In a moment defined more by uncertainty than upheaval, Canadians are not just evaluating what their leaders promise to do, they’re watching closely for how they lead. What kind of leadership do Canadians want right now? What traits are considered essential for the job of Prime Minister? And how well our main national political leaders – Mark Carney and Pierre Poilievre – living up to that standard?

That’s the question this research set out to answer.

Rather than focusing on policy or partisanship, we asked Canadians to step back and consider leadership more fundamentally: what qualities matter most in a Prime Minister? And once those expectations are established, how well do they describe the current Prime Minister and the man who hopes to replace him someday?

The data tell a compelling story. Canadians have a clear and widely shared view of what they want in a leader: calm under pressure, principled over partisan, thoughtful, strategic, and in touch with ordinary people. When measured against these expectations, Mark Carney significantly outperforms Pierre Poilievre on nearly every dimension. The contrast is especially striking among accessible voters – those open to voting Liberal or Conservative but don’t currently support those parties – who see Carney as better aligned with the leadership qualities they value most.

What follows is a detailed look at what leadership looks like to Canadians in the moment we are and how well the two main political figures in the country measure up.

The Nine “Must-Have” Leadership Qualities

We presented Canadians with a list of nine traits and behaviours and asked how important each is in selecting a Prime Minister. The result: a broad consensus on what Canadians expect in a leader.

Three-quarters (74%) say a Prime Minister must put the country’s interests ahead of political gain.

72% say they must understand the challenges facing ordinary Canadians.

71% want someone who has a clear strategy and plan.

68% expect open and clear communication about goals.

67% prioritize evidence-based decision making over ideological rigidity.

Traits like being calm and steady during uncertain times (65%), providing thoughtful answers (63%), and being willing to change one’s mind (59%) are also seen as must-haves.

Even traits that may feel like political style points, such as avoiding unnecessary conflict, are deemed essential by a majority (56%).

What’s notable is that these are not qualities easily written off as partisan. Liberal and Conservative voters alike rate them highly, with only small gaps between the two camps. This tells us that, for most voters, the bar is set high, and not particularly differently across the political spectrum.

Carney Closer to the Mark

Across all nine of the qualities tested, more Canadians believe Mark Carney embodies these traits than Pierre Poilievre. The gaps are not just statistical; they are substantial and consistent.

For example:

69% say Carney is “calm and steady during uncertain times”, the highest score on any attribute. Just 45% say the same about Poilievre.

On avoiding unnecessary conflict, Carney leads Poilievre by 16 points.

On providing thoughtful answers and communicating clearly, he leads by 13 and 5 points respectively.

Even on the top “must-have” item, putting the country’s interests ahead of political gain, Carney is seven points ahead (55% vs. 48%).

Carney’s biggest advantage shows up when we isolate “accessible” voters for the Liberal and Conservative parties – those who don’t currently support the party but say they might consider voting for it. Among these swing voters:

79% say Carney is calm and steady, compared to just 48% for Poilievre.On thoughtfulness and avoiding unnecessary conflict, the gaps are +18 and +20 in Carney’s favour.

Even on items like changing one’s mind when presented with better evidence, a rare trait in modern politics, Carney has a 7-point edge.

In short, Carney is not just liked. He’s seen as competent, principled, and measured, qualities that resonate strongly with the electorate right now.

Poilievre’s Challenge: A Growing Gap Between Expectations and Perception

For Pierre Poilievre, the picture is more complicated. While his supporters see him in highly positive terms, and his ratings are strong within the Conservative voter universe, his alignment with broader public expectations is weaker.

Among all Canadians, there’s a double-digit gap between what people want and what they believe Poilievre offers on almost every attribute:

A 26-point gap on putting the country ahead of politics (7-point larger gap than Carney)

A 20-point shortfall on making decisions based on evidence (9-point larger gap than Carney)

15- to 18-point deficits on being calm, having a plan, and communicating clearly.

To be clear, this doesn’t mean Canadians dislike him – since 55% say he understands ordinary Canadians, 54% say he communicates clearly, and earlier analysis finds his net favourable is -4 at the moment.. But those numbers simply aren’t high enough to match the public’s expectations vis-à-vis Mark Carney.

The result: a leader with a solid, motivated base, but one who faces clear resistance from other voters, especially those looking for calm, substance, and non-combative leadership.

What About Carney’s Gaps?

Carney’s numbers aren’t perfect either. Among all Canadians, there are still gaps between expectations and perception on several items. The largest:

19-point gap on putting the country ahead of politics.

17 points on understanding ordinary Canadians.

15 points on having a plan.

But these gaps are smaller than Poilievre’s, and in many cases, they’re closed or reversed among key groups. Among 2025 Liberal voters, for instance, Carney overperforms expectations on eight of the nine tested traits. And among accessible Liberal voters, he performs particularly well, including:

79% say he’s calm and steady.

77% say he avoids conflict.

70% say he communicates clearly.

The Qualities That Matter Most Right Now

Not all traits matter equally. When we look at what Canadians are telling us, three “must-have” qualities consistently sit at the top of the list:

Putting country over politics (74%)

Understanding ordinary Canadians (72%)

Having a clear strategy (71%)

These three speak to a moment where voters are tired of gamesmanship, hungry for authenticity, and eager for competence. The current context, post-pandemic fatigue, Trump 2.0, micro-economic anxiety, extreme weather, and international instability, has pushed people to look for leaders who are serious, grounded, and credible.

Traits like “calm during uncertain times” and “decisions based on evidence” round out the top five, reinforcing the picture of an electorate seeking steadiness, not spectacle. Reassurance over disruption.

In this environment, Mark Carney is better positioned. He delivers more of what voters say they want. And he does so not just with his base, but with those still up for grabs.

More Advanced Analysis

If the analysis above didn’t provide enough evidence, then the following should. When we use binary logistic regression to understand which of the nine elements are the most important in predicting positive impressions of both Mark Carney and Pierre Poilievre.

Mark Carney

The analysis for Mark Carney reveals that three attributes are especially predictive of a favourable impression of him.

Calm and steady during uncertain times (Estimate: 1.03, p < 0.001) This is the strongest predictor. Canadians who believe Carney embodies this trait are significantly more likely to view him favourably. In a moment shaped by volatility and uncertainty, this calmness appears to be a core leadership signal.

Puts the country ahead of party (Estimate: 0.90, p < 0.001) This quality, ranked as the most essential by Canadians, is also a strong driver of Carney’s appeal. It reinforces the importance of perceived integrity and national focus in shaping political impressions.

Makes decisions based on evidence, not ideology (Estimate: 0.88, p < 0.001) Competence and rationality matter. Carney’s technocratic brand appears to align well with voter preferences for evidence-based, pragmatic leadership.

Other statistically significant predictors include thoughtful communication, a clear plan, and a willingness to avoid unnecessary conflict. Traits like “changing one’s mind” or “understanding ordinary Canadians” are directionally positive but fall short of statistical significance at the 95% confidence level.

Pierre Poilievre

We ran a separate binary logistic regression to determine which leadership traits best predict positive impressions of Pierre Poilievre.

The most powerful predictor for Poilievre is “puts the country’s interests ahead of political gain” (Estimate: 1.46, p < 0.001). Canadians who perceive this quality in him are far more likely to view him favourably, reinforcing the central role this attribute plays across political lines. However, while the trait matters a great deal, fewer voters assign it to Poilievre compared to Carney, making it both a key opportunity and a vulnerability.

Two other traits also stand out as significant predictors of positive impressions:

“Provides thoughtful answers, not just talking points” (Estimate: 0.80, p = 0.005) This suggests that when Poilievre is seen as substantive and thoughtful, rather than reactive or rehearsed, his appeal broadens considerably.

“Understands the challenges facing ordinary Canadians” (Estimate: 0.62, p = 0.009) This aligns with one of Poilievre’s brand strengths, his repeated focus on affordability, housing, and everyday struggles. When this connection lands, it drives favourability.

Three additional traits, having a strategy, clear communication, and avoiding conflict, are also statistically significant and positively associated with favourable views. However, the magnitude of these effects is smaller.

Interestingly, “being calm during uncertain times” and “making decisions based on evidence, not ideology” are not significant predictors in this model. This may reflect a brand built more on urgency, conviction, and contrast than on calmness or technocratic pragmatism.

One trait, “avoids unnecessary conflict”, is negatively associated with favourable impressions of Poilievre (Estimate: -0.70, p = 0.04), meaning that those who perceive him as not combative are less likely to view him positively suggesting those who like him, appreciate the friction he creates. They likely want more, not less – even as most Canadians would prefer a leader who doesn’t do that.

Insight from the Advanced Models

When we compare the two models side by side, a clear pattern emerges: while both Mark Carney and Pierre Poilievre benefit from being seen as leaders who put the country ahead of political gain, the drivers of favourable impressions diverge beyond that.

For Carney, favourability is most strongly linked to perceptions of calmness, evidence-based decision-making, and measured, principled leadership, traits that reflect a technocratic, steady approach.

In contrast, Poilievre’s support is driven more by being seen as thoughtful, in touch with ordinary Canadians, and clear in his communication, although his more confrontational style may be limiting his broader appeal despite it being a driver of favourability to those who like him. In short, Canadians reward both men for seriousness and purpose, but Carney wins with reassurance and steadiness, while Poilievre’s strength comes from connection and conviction.

So What?

In a tight race where the Conservative and Liberal parties are statistically neck-and-neck, the question of leadership character could play a defining role. Voters aren’t just asking who has the better policy, they’re asking who they trust to steer the country through a moment defined by volatility, high stakes diplomacy, and shifting economic terrain.

Pierre Poilievre’s strength continues to lie in mobilizing his base and speaking to a sense of urgency and dissatisfaction. But the data here reveal the limits of that strategy: his brand is not yet aligned with the broader public’s expectations of a Prime Minister. And his more confrontational political style, while appealing to core supporters, may be holding him back among those who value calm, collaboration, and institutional trust.

Mark Carney, on the other hand, benefits from being perceived as measured and policy-driven. His perceived temperament matches what more Canadians are looking for right now, especially as his government navigates complex negotiations with the United States and continues to respond to global trade turbulence stirred up by Donald Trump.

Canadians are not vague or passive about what they want in a leader. They want someone who puts the country first, understands their challenges, and brings a clear, steady hand. Right now, Mark Carney is meeting those expectations better than Pierre Poilievre, not just with his own base, but with the people in the middle who will decide future elections.

These numbers reinforce the challenge Poilievre faces in broadening his appeal. He’s not far off in raw vote numbers, but he trails on the stuff that defines prime ministerial leadership in the minds of most Canadians. That doesn’t mean the gap can’t close, but it may require a recalibration of tone and substance or a change in the competitive landscape (a rising NDP and BQ).

As Canadians enter the second half of 2025, most are not demanding radical reinvention. They’re asking for stability, empathy, and competence. The question isn’t just whether voters are satisfied with government performance at this point; it’s whether they see a leader who matches the moment.

Carney’s calm, technocratic style fits well with a public mood that prizes steadiness over spectacle. For Poilievre, the challenge isn’t enthusiasm, it’s expansion. Unless he can reshape how Canadians see him on the traits they value most, the path to victory will depend less on how frustrated people are with the status quo, and more on whether they believe the alternative is truly ready to lead.

Methodology

The survey was conducted with 1,915 Canadian adults from July 10 to 15, 2025. A random sample of panelists were invited to complete the survey via partner panels based on the Lucid exchange platform.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.2%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, and region. Totals may not add up to 100 due to rounding.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

Between July 10 and 15, 2025, Abacus Data conducted a national survey of 1,915 Canadian adults to examine their perceptions and opinions about artificial intelligence (AI). As AI rapidly becomes a fixture of our daily lives, Canadians are grappling with a complex mix of curiosity, skepticism, fear, and optimism. From virtual assistants, fast diagnostics, rapid customer service, and smart devices to recommendation systems, AI is becoming increasingly embedded in the fabric of our daily routines. Governments, corporations, and influencers are touting the benefits. But the big question remains: Are we truly ready to embrace its opportunities, or are we cautious or even scared about the risks it brings? The truth lies somewhere in between.

The Growing Presence of AI in Everyday Life

AI is here, and it is becoming a part of many Canadians’ daily lives, even if they don’t always realize it. 45% of Canadians use AI tools on a regular basis, while 55% note that they rarely or never engage with AI. When considering usage, there is a clear generational divide: Younger Canadians are far more likely to use AI, with 72% of those aged 18-29 and 62% of those aged 30-44 regularly incorporating it into their lives. In contrast, just 20% of Canadians aged 60+ use AI on a regular basis. This growing reliance on AI among younger generations signals a significant shift, one that has the potential to expand as technology becomes even more integrated into everyday life.

Trust and Distrust in AI

When it comes to trust in AI, Canadians are split: 37% trust in AI, but a significant 50% remain skeptical about its role in society. Young people tend to be more trusting: 57% of 18-29-year-olds express confidence in AI, while only 20% of Canadians 60+ share that sentiment. Men also tend to trust AI more than women, with 42% of men confident in its capabilities compared to just 32% of women.

What accounts for this gap? Familiarity plays a significant role. While 53% of Canadians say they are familiar with AI tools, this figure is notably higher among younger, more tech-savvy groups. Specifically, 74% of those aged 18-29 and 67% of those aged 30-44 are comfortable navigating the AI landscape. In contrast, 69% of Canadians aged 60+ report being unfamiliar with AI.

Moreover, familiarity with AI is closely linked to trust. Among those who are familiar with AI, 56% express trust in it, compared to just 16% of those who are not familiar. Additionally, frequent users of AI report higher levels of trust—69% of regular AI users trust it, while only 17% of occasional users and just 5% of non-users share that sentiment. This highlights the need for improved AI literacy across all generations to foster greater trust and understanding.

The Benefits of AI: Optimism for the Future

Despite the skepticism that comes with technological advancements, there is unmistakable evidence of AI’s ability to revolutionize and improve various aspects of life. Many Canadians see AI as a tool for increased efficiency and productivity, with 33% believing it can reduce human error and 30% feeling it will improve access to information and education. Others are excited about the promise of convenience in daily life, enhanced healthcare, and new opportunities for creativity and innovation.

However, not everyone is convinced. Only 13% believe AI will significantly drive economic growth or create new jobs, and 24% feel it will have no positive impact on society. Despite these concerns, many Canadians see AI’s value in improving everyday experiences – whether through faster decision-making, personalized recommendations, or even advancements in healthcare and other industries.

The Dark Side of AI: Concerns and Risks

While AI offers many benefits, it also raises significant concerns with the public. Many Canadians fear AI could be used for malicious purposes, with 43% worried about its potential to manipulate or harm. The spread of misinformation is another major issue, cited by 42%, as AI-generated content becomes increasingly difficult to differentiate from truth. Privacy is also a key concern for 38%, who worry about personal data being exploited.

Economic and social fears are prevalent as well. 34% of Canadians are concerned about job losses due to automation, and another 34% fear losing human control over AI systems, with machines making decisions without oversight. Social isolation is another worry for 30%, who fear that increased AI interactions could reduce meaningful human connection. Additionally, 25% are anxious about unintended consequences beyond human control, highlighting the need for careful management and regulation as AI becomes more integrated into society.

Unprepared for Change: How AI Is Changing Our Lives

Most Canadians do not feel prepared for the change that AI will mean for them and society. A little over half (54%) of Canadians feel unprepared to keep up with the rapid pace of change that AI is bringing, with older Canadians (73% of those 60+) feeling the most unready. In contrast, younger Canadians, particularly those aged 18-44, are much more confident in their ability to adapt to AI’s growing role. This divide highlights the need for greater education, engagement, and support to help all Canadians, especially older generations, navigate the challenges and opportunities that AI will bring to our lives.

The Upshot

Governments, including the Mark Carney-led federal government, are charging ahead with AI strategies, investment plans, and regulatory frameworks, aiming to harness AI’s potential to drive innovation, productivity, efficiency, and global competitiveness. However, outside of official Ottawa and in the boardrooms of tech firms, public sentiment remains far more cautious, if not outright skeptical.

As AI continues to evolve, Canadians are presented with both exciting opportunities and significant concerns. While AI holds the potential to transform industries, improve daily life, and spark innovation, its rapid development, combined with limited understanding, has fuelled skepticism and fear. This is particularly true among older generations, who feel disconnected from the technology and its broader implications. And we believe understanding of AI’s impact is underappreciated suggesting public opinion could change rapidly as stories about job losses, disruption, and change continue to spread. The speed of AI’s advancement, coupled with uncertainties about privacy, misinformation, and job displacement, has made many wary of its potential risks.

The gap between elite enthusiasm and public anxiety is dangerous. As David argued in the Toronto Star op-ed recently, it risks creating a political backlash that could rival past populist uprisings, especially if the human costs of AI are downplayed or ignored. To bridge this divide, the government must lead with transparency, addressing concerns head-on while emphasizing AI’s economic and social benefits. Only then can we ensure AI is embraced as a transformative force, rather than a source of fear and division.

Methodology

The survey was conducted with 1,915 Canadian adults from July 10 to 15, 2025. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.24%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2025 Canadian election following up on our outstanding record in the 2021, 2019, 2015, and 2011 federal elections.

A few months removed from a commanding re-election, Premier Doug Ford and the Ontario PCs continue to find themselves continuing to hold high levels of public support and a big lead over a divided opposition. With no major controversies consuming Queen’s Park, a relatively quiet opposition, and a public square still focused more on the potential impact of Trump’s policies, the opinion environment remains favourable to the provincial government.

Vote Intention: PC Party Tops 50%

If a provincial election were held today, 50% of committed voters say they would cast their ballot for the Progressive Conservatives. That’s up one point since our last survey in early June and marks the party’s highest vote share since the start of 2024. The Liberals remain at 28%, unchanged from last month, while the NDP has slipped further to 13%, down a point. The Greens now sit at 6% (+1), while other parties attract 3% of the vote.

Approval Holding at High Levels

Doug Ford’s approval ratings remain strong and stable. As of mid-July, 44% of Ontarians approve of the job he and his government are doing, unchanged since our last wave. Disapproval has edged up slightly to 32% (+1), but the government still holds a +12 net rating, among the highest seen in the past two years.

The trendline confirms it: since late 2023, the Ford government has been on a slow but steady upward climb. From a low point in early 2024, approval ratings recovered through the spring and peaked just before the provincial election. Today, they remain near those highs, suggesting a Premier still very much in control of his narrative.

Ford’s Personal Brand Continues to Strengthen

The Premier’s personal numbers are even more telling. Today, 46% of Ontarians say they have a positive impression of Doug Ford, compared to 33% who view him negatively, a net +13 rating, and the highest of any provincial leader by a wide margin.

By contrast, Bonnie Crombie’s impressions are evenly split (33% positive, 32% negative), resulting in a net of just +1. Marit Stiles and Mike Schreiner both have net impressions of +4, but nearly one in five voters say they don’t know enough about either to offer an opinion.

Among all voters, Ford is also the top choice for Premier, with 46% selecting him, more than double the number who choose Crombie (20%) or Stiles (12%). That advantage extends across nearly every region, age group, and gender category.

Broad and Stable Coalition

The PC coalition remains impressively wide. Regionally, they lead by double digits across the board:

GTHA: 54% PC vs. 30% Liberal

Toronto: 49% PC vs. 32% Liberal

Southwestern Ontario: 54% PC vs. 23% Liberal

Eastern Ontario: 43% PC vs. 29% Liberal.

Demographically, the PCs lead among both men (53%) and women (48%), and especially among Ontarians aged 45 to 59, where they hold 59% support. Among voters aged 60 and over, they lead with 53%, and even among younger voters aged 18 to 29, the party garners 42%—still ahead of the Liberals at 31% and Greens at 10%.

This is a government whose support reaches across regional and generational lines, anchored by perceptions of stability and confidence at a time of uncertainty created by US President Donald Trump.

The Opposition Faces Familiar Challenges

While Ford’s numbers have remained strong, the opposition continues to struggle with definition and visibility.

Bonnie Crombie’s numbers have improved modestly over the last few months, but she remains a polarizing figure with a net impression of just +1. Marit Stiles and Mike Schreiner remain liked by those who know them but largely unknown to most voters. Neither the NDP nor the Greens are making meaningful gains.

That being said, the Ontario Liberals have as large a pool of accessible voters as the PCs. 54% of voters say they would consider voting Liberal, one point ahead of the PCs at 53%. The NDP’s accessible voter pool sits at 40%, and the Greens trail at 30%. There is potential for the Ontario Liberals to expand their support.

Ford the Collaborator?

Part of Ford’s sustained appeal appears to be his shifting political style. The “buck-a-beer” populism of earlier terms has been replaced by a more pragmatic, centrist governance model that seems well-attuned to the mood of the moment. In a province (and country) focused on responding to economic uncertainty, affordability, and geopolitical friction, Ford’s leadership feels, at least to many, grounded, less partisan, and more functional.

He’s also benefited from an increasingly cooperative dynamic with the Carney-led federal government, particularly on economic growth and dealing with the United States. Ford’s willingness to be a team player on the national stage, without losing his brand, continues to reinforce a positive image among many Ontarians.

The Upshot

Doug Ford and the Ontario PCs are heading into late summer in a commanding position. With 50% of committed support, a wide lead over their rivals, and consistently strong personal numbers, the Premier appears to have consolidated both power and public confidence, at a time when many Ontarians are looking for stability and economic focus.

The opposition, by contrast, remains fragmented and low-profile. The Ontario Liberal Party, while still the main alternative in vote share, has not gained ground. However, Bonnie Crombie’s personal numbers have improved over the last two months, and the party’s accessible voter pool is equal to that of the PCs. With a party convention looming in September, where Crombie will face a formal leadership review, the pressure to redefine the Liberal brand and solidify support is only growing. But the environment is one the Liberals will have a hard time shaping themselves and there’s likely little Crombie can to do change fortunes right now. It’s about building and being ready to respond in the future if the mood and circumstances change.

The NDP and Greens, meanwhile, continue to struggle with visibility. Both leaders remain modestly liked, but their parties are not yet competitive across key regions or age groups.

At a broader level, voters remain focused on affordability, inflation, and Canada’s role in a volatile global landscape. In that context, the Ford government’s measured, pragmatic approach continues to resonate. For now, the political environment remains calm, and that calm continues to benefit the Premier.

But as always, conditions can change. Economic pressure points remain. Public patience on housing is not unlimited. And the Liberal convention in September could reshape the conversation, either by clarifying Crombie’s mandate or reopening questions about who should lead the Liberals.

For now, though, the PCs are in a dominant position, and Doug Ford shows every sign of making the most of it.

Methodology

The survey was conducted with 1,000 eligible voters in Ontario from July 10 to 15, 2025.

A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 3.1%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Ontario’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

We are Canada’s most sought-after, influential, and impactful polling and market research firm. We are hired by many of North America’s most respected and influential brands and organizations.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail, and exceptional value.

And we are growing throughout all parts of Canada and the United States and have capacity for new clients who want high quality research insights with enlightened hospitality.

Our record speaks for itself: we were one of the most accurate pollsters conducting research during the 2021 Canadian election following up on our outstanding record in the 2019, 2015, and 2011 federal elections.

From July 10 to 15, 2025, Abacus Data surveyed 1,915 Canadian adults about the state of federal politics, capturing opinion just days after the federal government adjusted its approach to the Digital Services Tax (DST) in response to the Trump administration. As Ottawa continues its high-stakes renegotiation of the Canada-U.S. trade relationship, aiming for a deal before August 1, Canadian public opinion remains remarkably steady.

Direction of the Country: Optimism Holds, But Unease with the World Persists

Just over a third (36%) of Canadians believe the country is headed in the right direction, down slightly from two weeks ago. While more still say Canada is on the wrong track (44%), that number has stabilized after months of modest improvement. However, global sentiment remains bleak: only 12% think the world is headed in the right direction, and just 11% feel that way about the United States, a low point driven largely by anxiety over President Trump’s economic and foreign policy moves.

Supporters of the federal Liberals are far more optimistic (57%), while just 20% of Conservatives share that view. Optimism is higher among older Canadians (43% among those 60+), Atlantic Canadians (43%), and higher-income households. Young people (18–29) and women remain notably less upbeat, with only 33% and 31% respectively saying Canada is headed in the right direction.

What’s Keeping Canadians Up at Night? Tariffs, Trump, and Global Instability

In a word cloud generated from open-ended responses, two terms dominate: “Tariff” and “Trump.” Trade anxieties have clearly surged to the top of Canadians’ concerns this week, particularly in the wake of the Trump’s announcement of a 35% tariff on Canada. While domestic issues like “costs” and “rent” remain visible, the overriding worry is global: war, economic uncertainty, and Trump’s unpredictability loom large.

Top Issues: Affordability, Trump, and the Economy