On behalf of the Canadian Nuclear Association, Abacus Data developed a different approach to surveying contemporary attitudes towards nuclear energy. Instead of looking principally at nuclear as a source of energy, we created a survey that explored whether people might feel differently about nuclear if the conversation was about how to find energy solutions that reduced carbon emissions.

This release details our findings from this study, which was conducted among 2,500 Canadian adults from February 8 to 12, 2019.

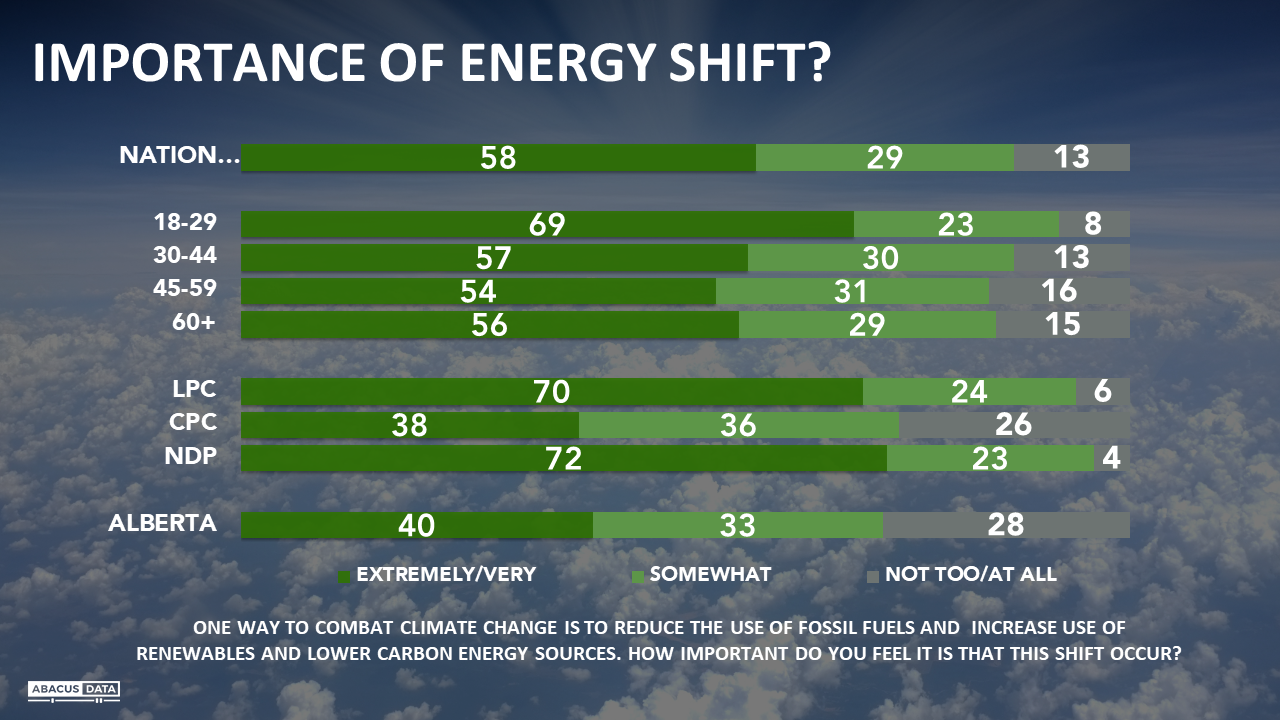

CLIMATE CONCERNS AND SUPPORT FOR A LOW CARBON ENERGY SHIFT

• The large majority (82%) of Canadians are somewhat, very or extremely concerned about climate change.

• Alongside this, 87% consider it somewhat, very or extremely important to “reduce the use of fossil fuels and increase the use of renewables and lower carbon energy sources”. Belief in the importance of this shift cuts across regional, generational and partisan lines.

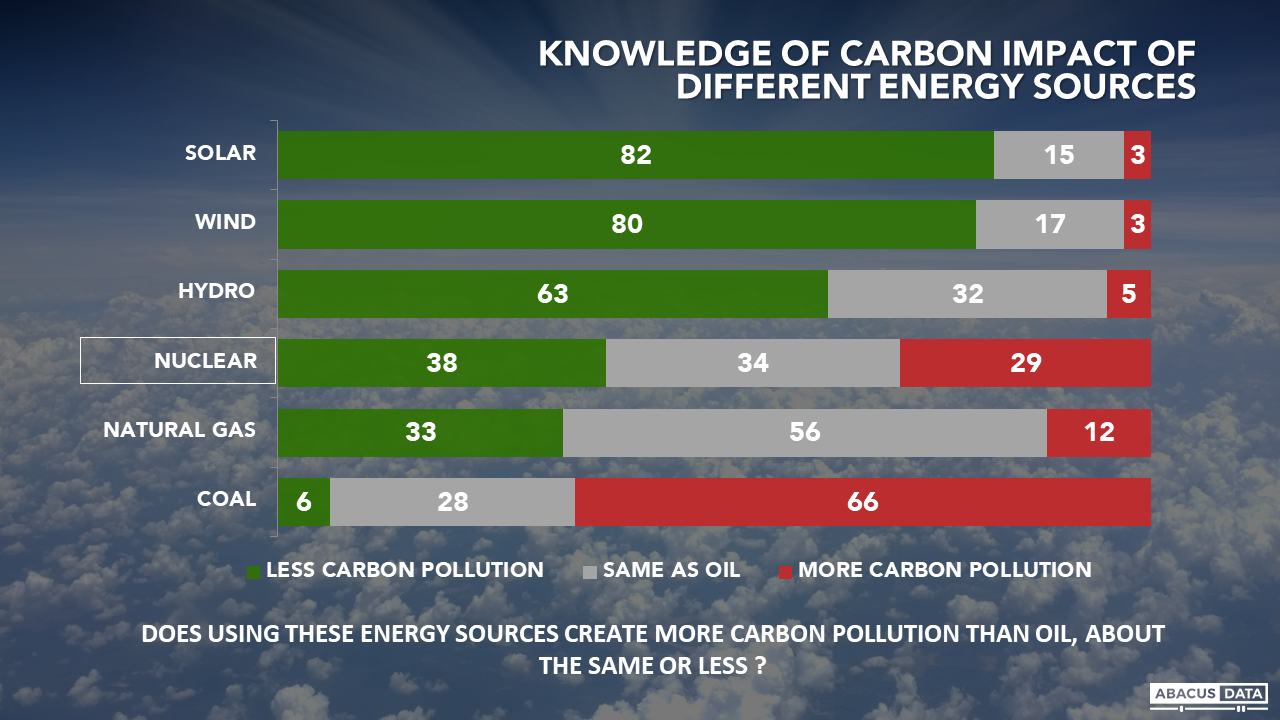

KNOWLEDGE OF CARBON IMPACT OF NUCLEAR

• To measure how familiar people are with the carbon impact of nuclear energy we included in our survey a series of questions that asked people whether they perceived each of a variety of different energy sources as having a greater, equal or lesser impact than oil. The results revealed that only 38% of Canadians were aware that nuclear is a lower carbon form of energy compared to oil.

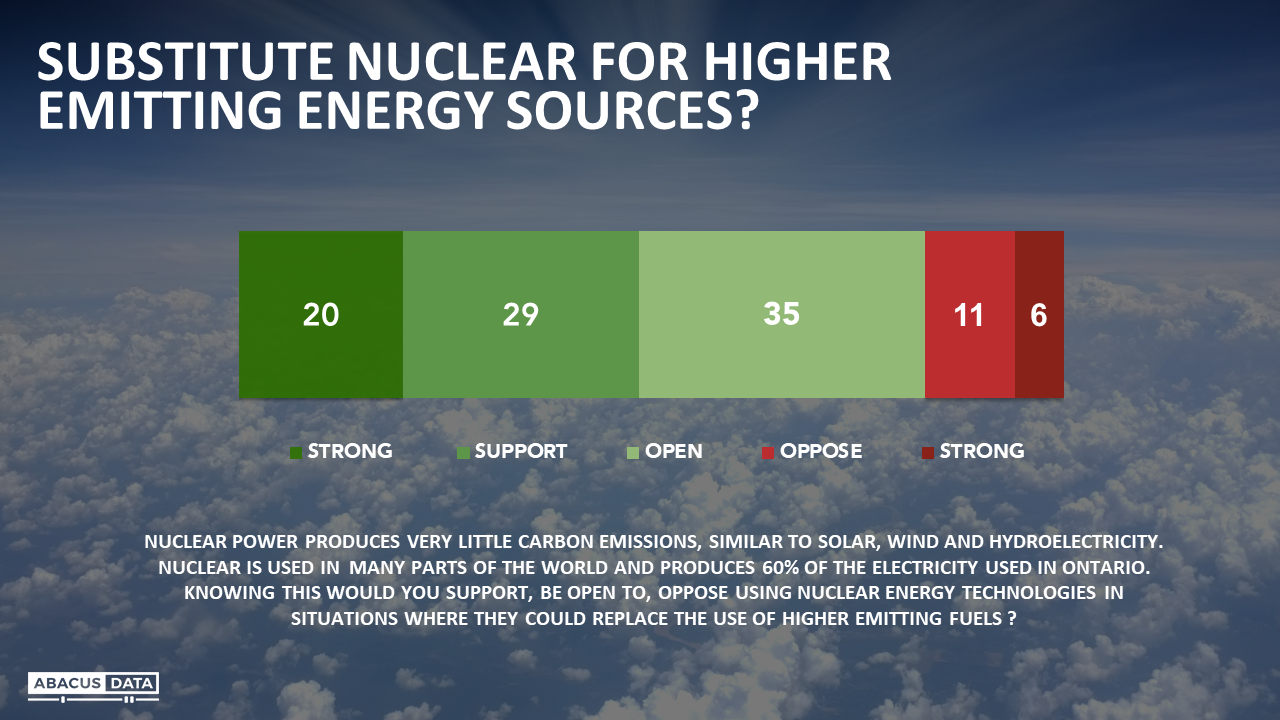

INFORMED REACTION TO NUCLEAR

• When informed that nuclear power emissions are similar to solar, wind and hydro, and asked how they felt about the idea of using nuclear in situations where it could replace higher emitting fuels, a large majority (84%) say they are open (35%) to or supportive (49%) of this.

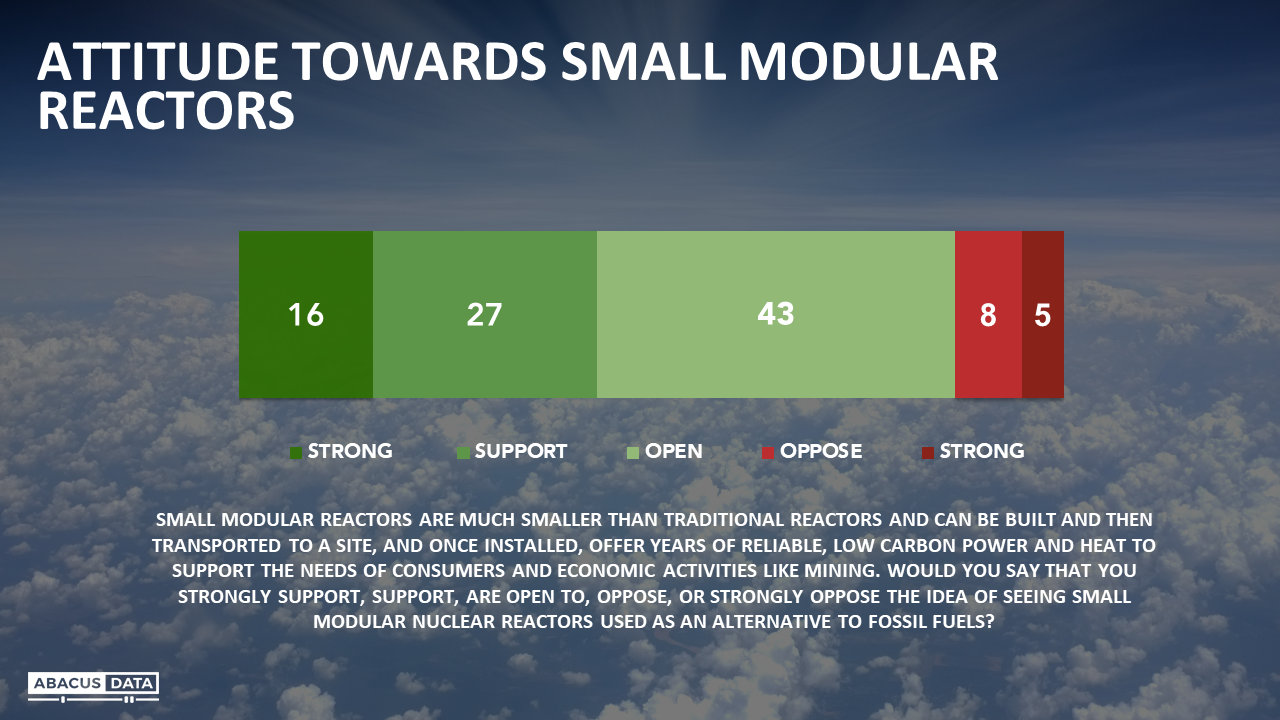

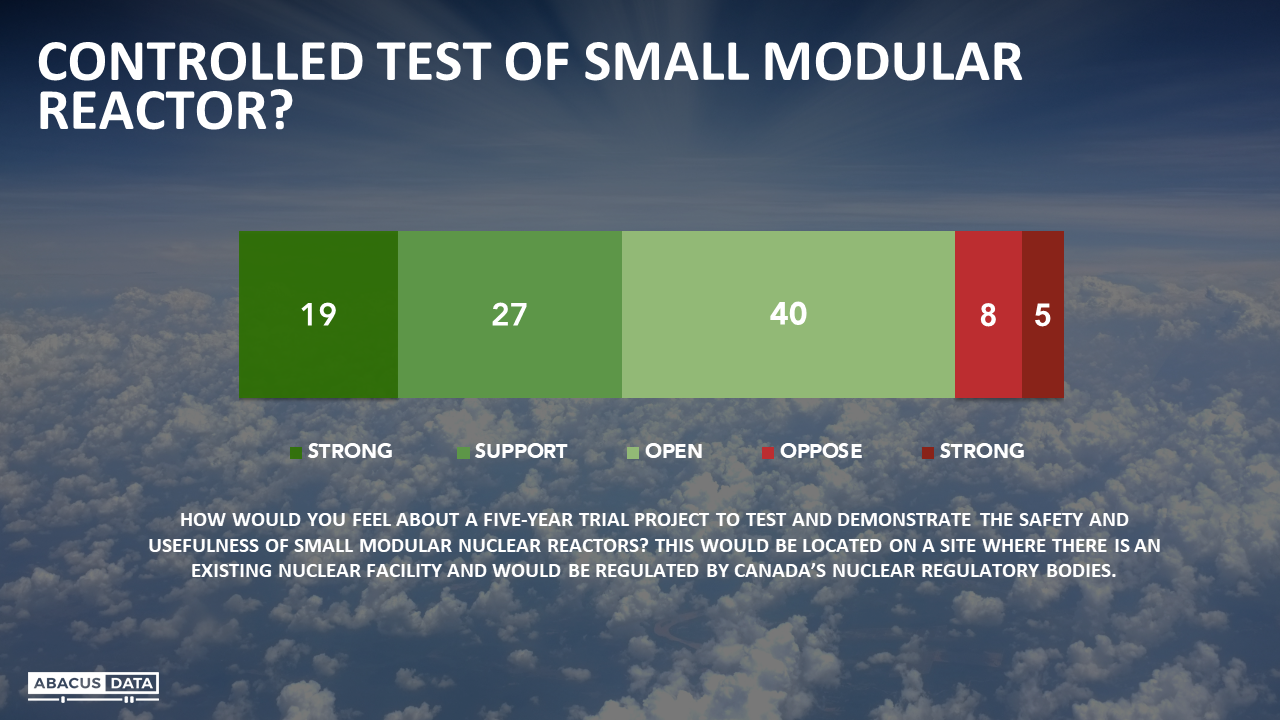

REACTION TO SMALL MODULAR REACTORS

• When informed that small modular reactors can be built transported to a site and once installed can offer years of reliable, low carbon power and heat to support the needs of consumers and economic activities like mining” a large majority (86%) say they are open (43%) to or supportive (43%) of this.

• Similar support is found for the idea of a five-year trial project to test and demonstrate the usefulness of small modular reactors, located on an existing regulated facility.

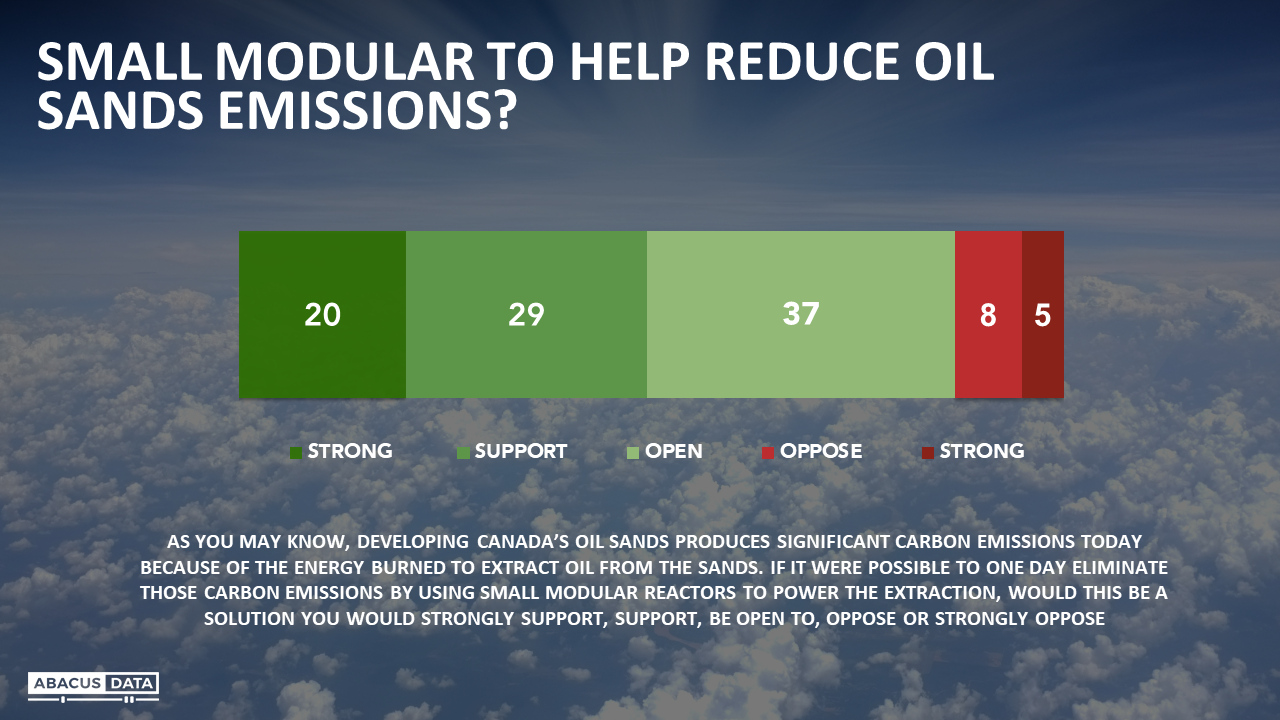

• The idea of using small modular reactors to help reduce oil sands emissions also shows very broad support or openness.

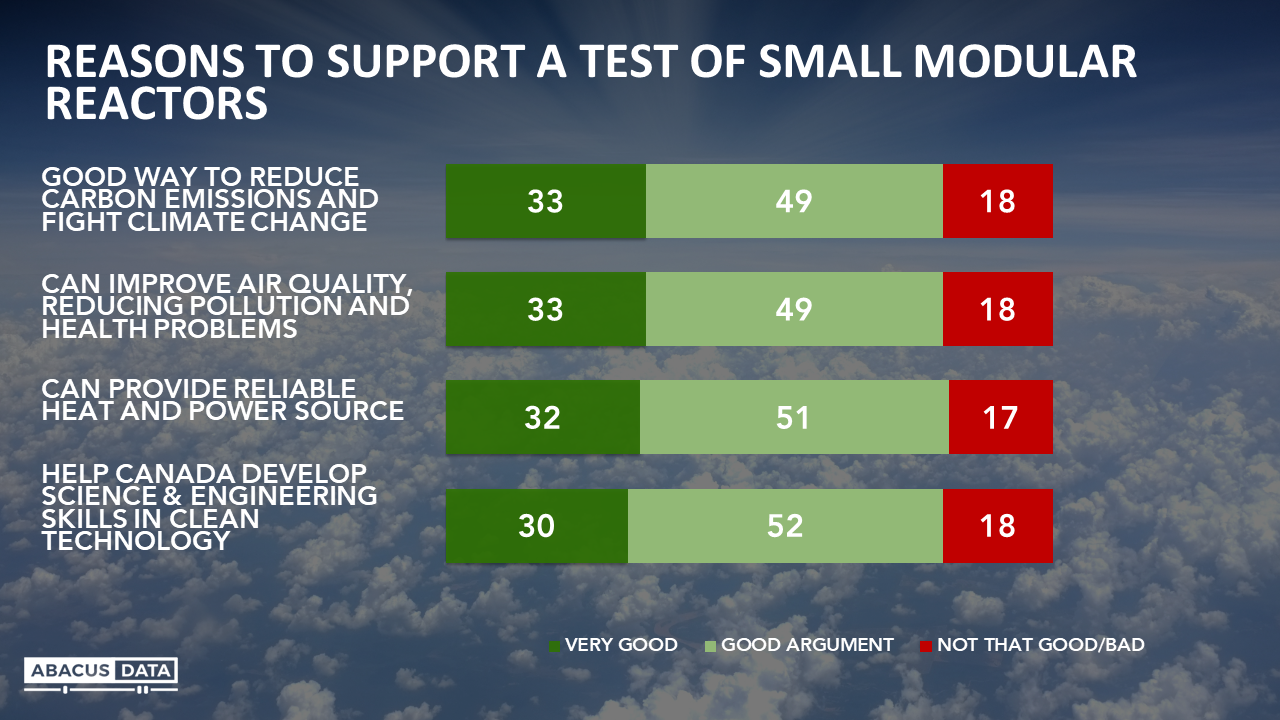

• Support for the idea of a trial is predicated on several arguments that resonate with people: including reducing emissions and fighting climate change, improving air quality and health, offering a reliable heat and power source, and helping Canada develop skills in clean technology.

SURROUNDING OPINIONS

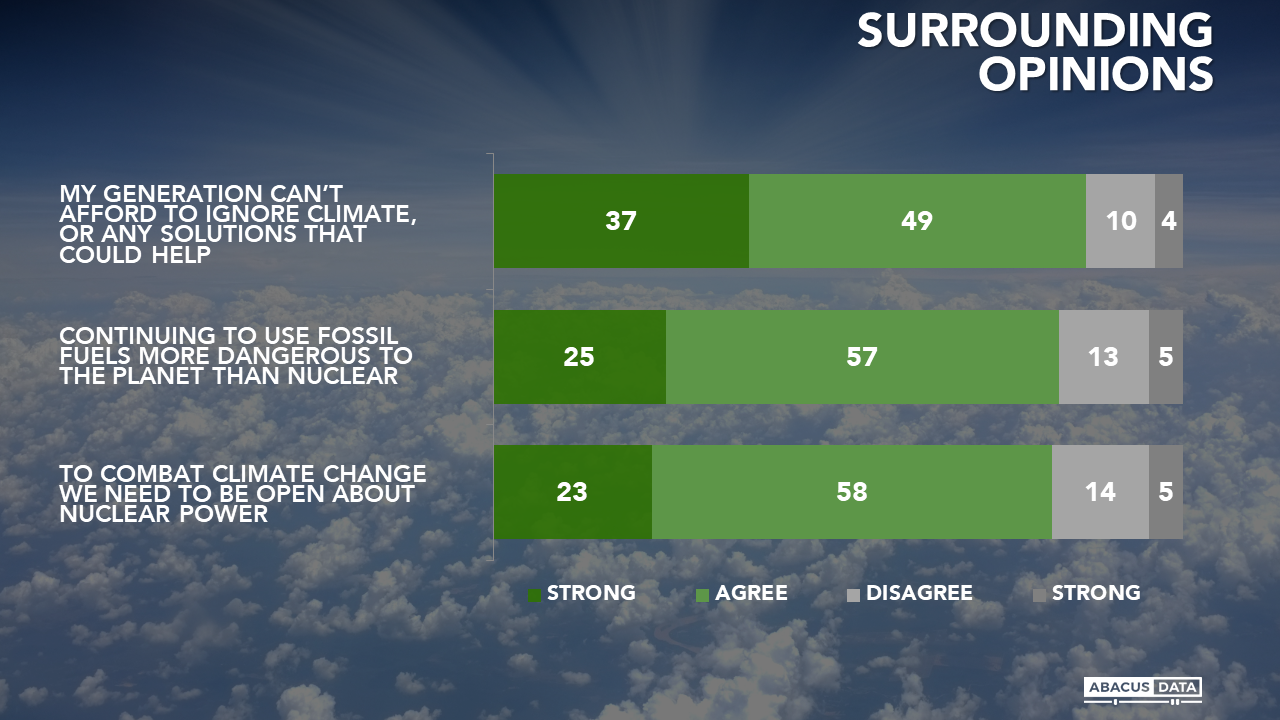

• In our survey, we also explored some surrounding opinions. Among the interesting findings were that 83% believe that continuing to use fossil fuels is more dangerous to the planet than nuclear energy. Similar proportions feel that “to combat climate change we need to be open about nuclear power.”

UPSHOT

According to Bruce Anderson: “These results make clear that for many people, the issue of climate change and the need to reduce carbon emissions, means being open to potential new roles for nuclear technology. To date, many people are unaware of the carbon-reducing contribution that nuclear can offer, and the data indicate that when informed about the facts, there is broad interest in exploring potential trials in a regulated context.”

METHODOLOGY

Our survey was conducted online with 2,500 Canadians aged 18 and over from February 8th to 12th, 2019. A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 1.9%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

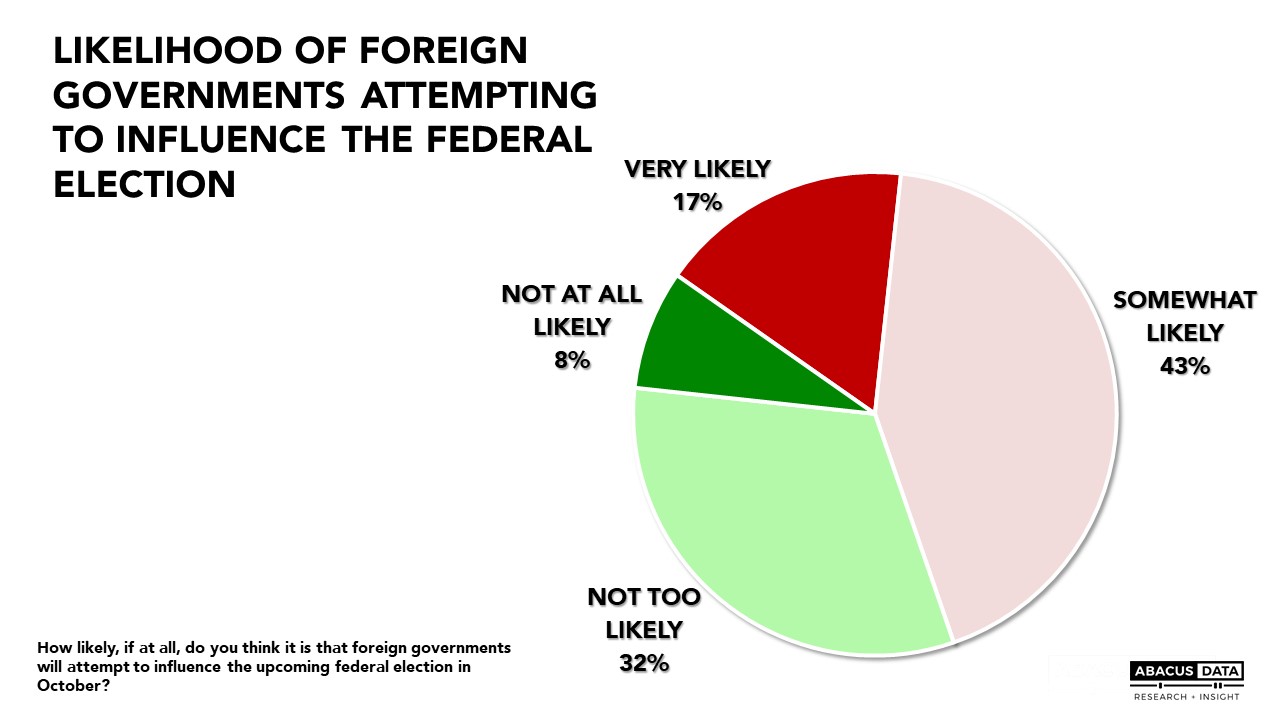

Over the last couple of years, there has been a lot of discussion about interference in elections. In our latest survey conducted at the end of January to early February, we explored how Canadians feel about the risks facing Canada.

Here’s what we found:

Most (60%) Canadians think it likely that foreign governments will attempt to influence Canada’s federal election this October. This worry is fairly consistent across the political spectrum. Most (64%) Liberal, NDP (64%), and Conservative (58%) supporters believe it is likely that foreign governments will attempt to influence our election.

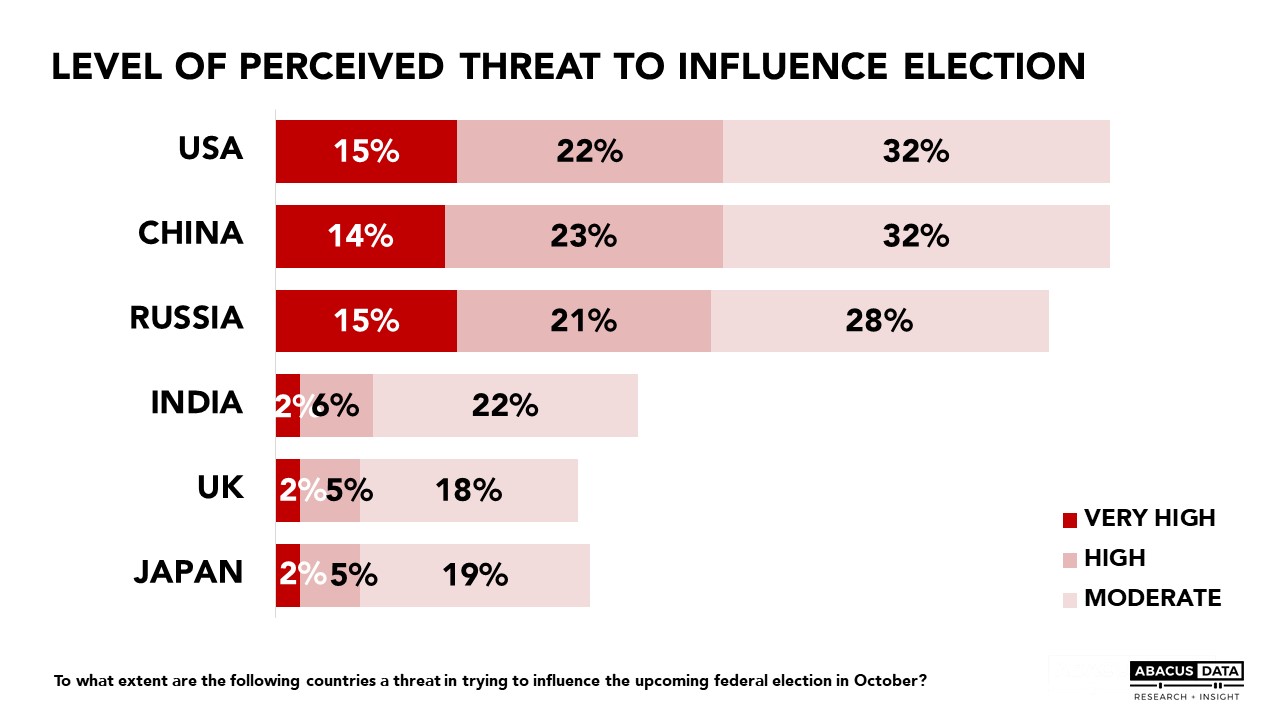

Not all countries are seen as equal when it comes to the chances that they might try to influence our political process. People are much more likely to see China, Russia, and the US as posing a threat than Japan, the UK, or India.

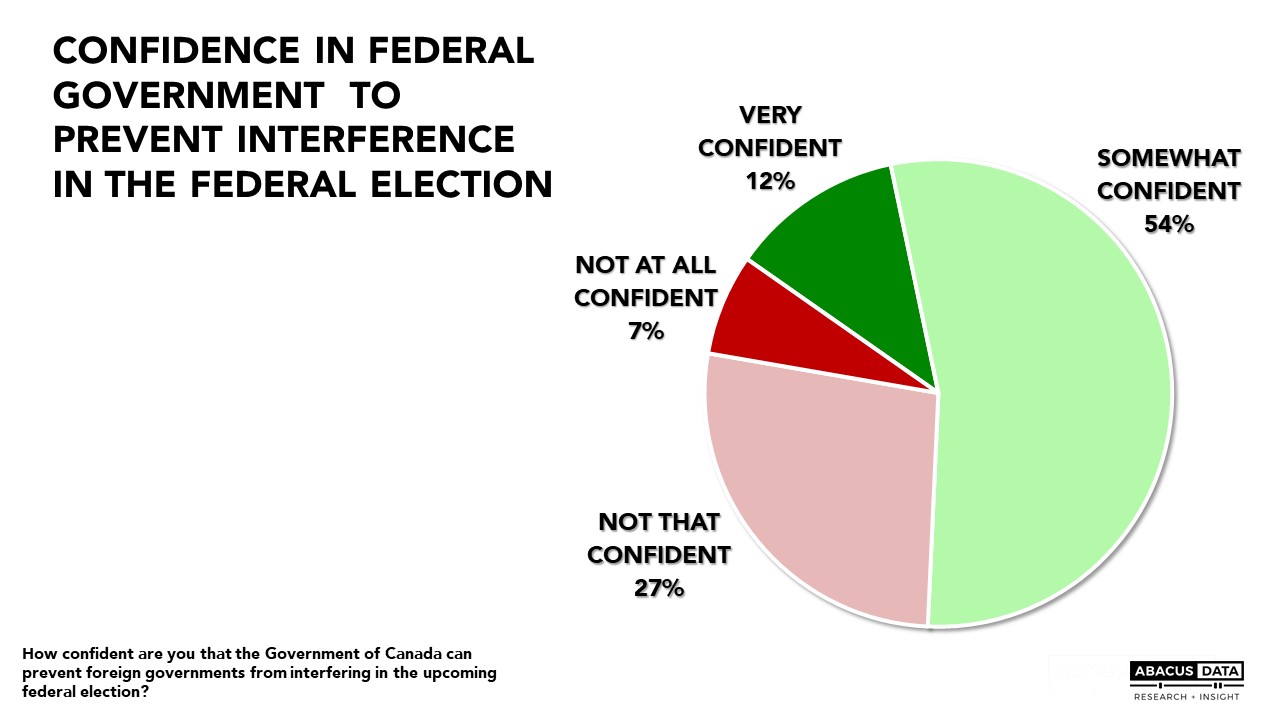

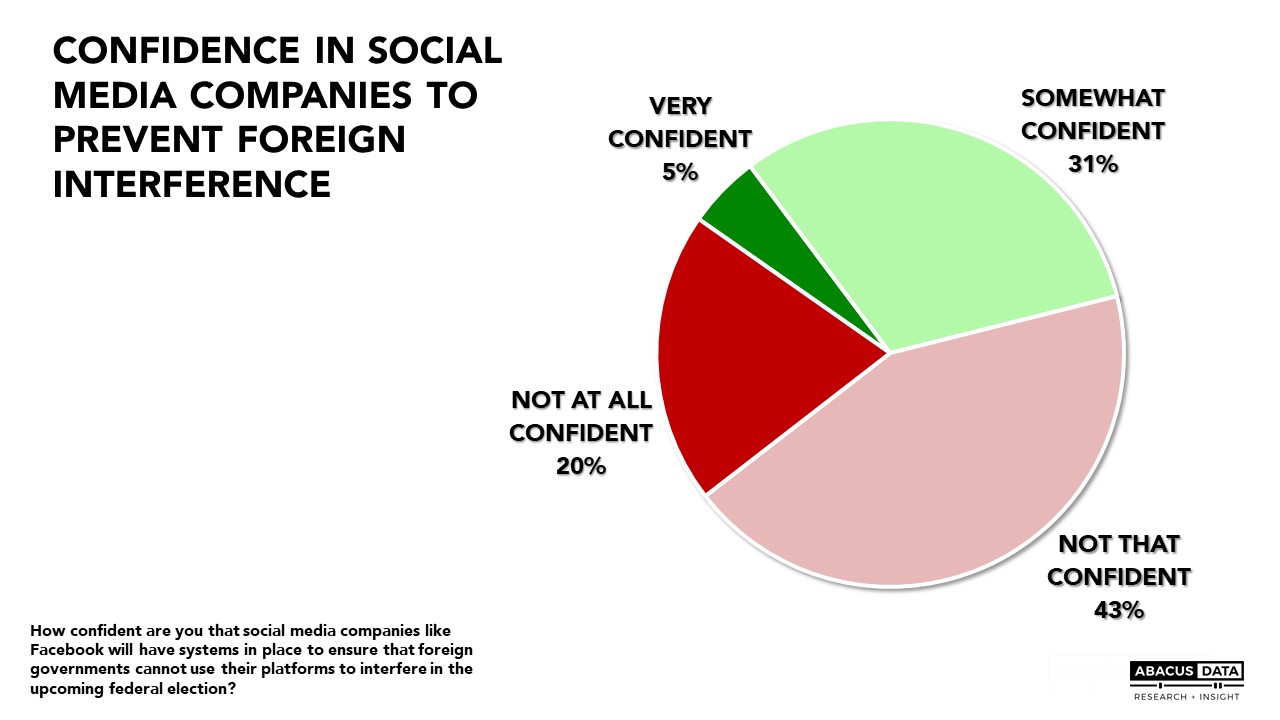

Confidence in the defenses against attempts to influence our election is mixed. Two out of three have some confidence that the Government of Canada can prevent foreign governments from interfering. But confidence in social media companies like Facebook is much lower.

Younger Canadians (18 to 29) express more confidence in social media companies to prevent foreign interference (48% at least somewhat confident vs. 34% among those aged 30+). Liberal supporters (44%) are slightly more confident than Conservative (37%) and NDP (37%) voters.

UPSHOT

According to Bruce Anderson: “It’s remarkable how many people arrived at a point where they place the same level of trust in the US as they do in China and Russia when it comes to interfering in our political process.

It’s also striking that the idea of interference has almost become an expected, unwelcome part of life in the digital age.

Finally, the gap in confidence about the defenses offered by government compared to social media companies is a signal that people will likely call for tougher regulation if they judge that private companies are lax in their efforts to protect our democracy from interference.”

According to David Coletto: “Canadians are mindful that foreign governments are likely to try and influence the upcoming federal election but most are at least somewhat confident that the Government of Canada can prevent it from happening. When it comes to social media companies, there’s much less confidence, although younger Canadians express a higher level than those older than them. What is clear is that concern about foreign influence on Canada’s election is a cross-partisan issue and one that worries Liberals, Conservatives, and New Democrats alike.”

Read the Toronto Star’s coverage of the poll here.

METHODOLOGY

Our survey was conducted online with 2,500 Canadians aged 18 and over from January 30 to February 5, 2019. A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.0%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

ABOUT ABACUS DATA

We are the only research and strategy firm that helps organizations respond to the disruptive risks and opportunities in a world where demographics and technology are changing more quickly than ever.

We are an innovative, fast-growing public opinion and marketing research consultancy.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail and exceptional value.

One of the most hotly debated issues in Ottawa in recent years has been the federal government’s legislative proposals surrounding major project reviews. The current bill in question is known as C-69. In our latest nationwide survey, we asked a few questions to take the temperature of the public on this legislation. Here’s what we found:

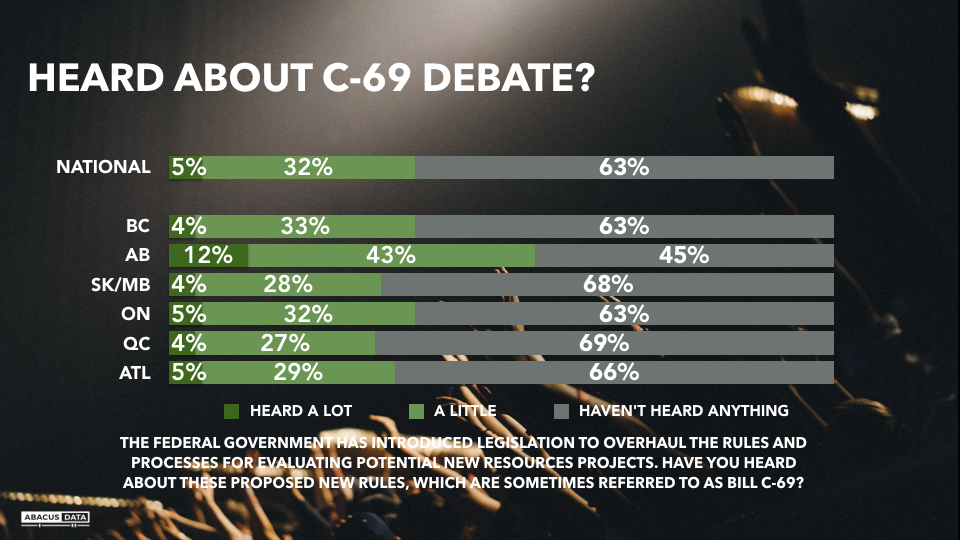

Initial question: “The federal government has introduced legislation to overhaul the rules and processes for evaluating potential new resources projects. Have you heard about these proposed new rules, which are sometimes referred to as Bill C-69?”

• Few people (5%) have heard a lot about this bill. Another 32% say they have heard a little, but 63% say they haven’t heard anything. Awareness is higher than average in Alberta, but even in that province only 12% say they have heard a lot about the bill, and almost half have heard nothing about it.

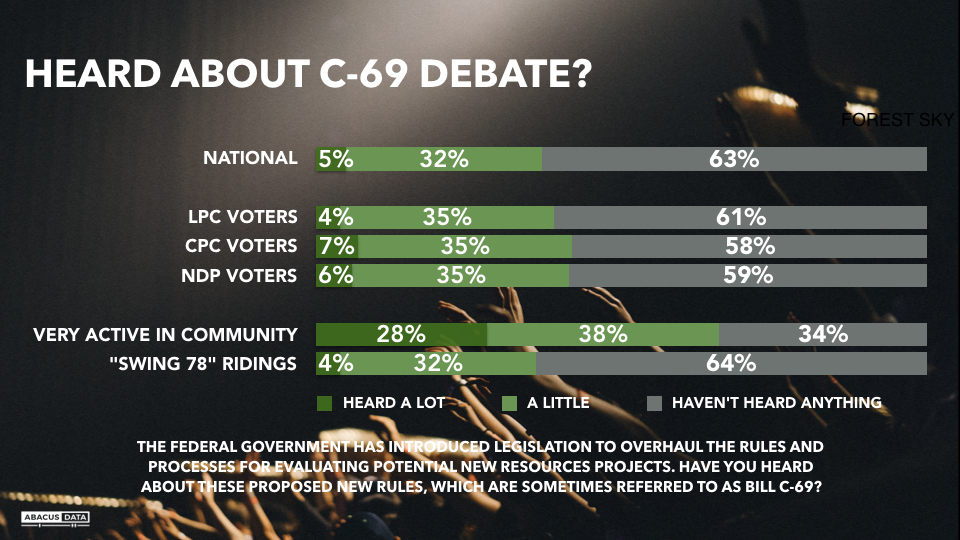

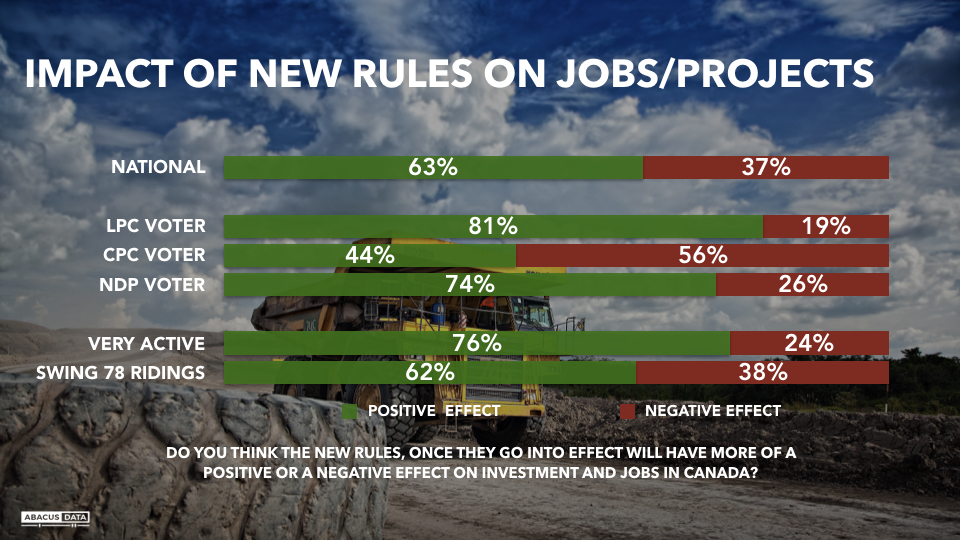

• Levels of awareness of this bill are basically the same across party lines. In the 78 ridings won by a margin of 5% or less in 2015 (we refer to as the “Swing 78” awareness of the C-69 debate is no higher than the national average.

• Higher levels of attentiveness are seen among those who describe themselves as very active in discussing community matters, but this subset only amounts to 6% of the adult population.

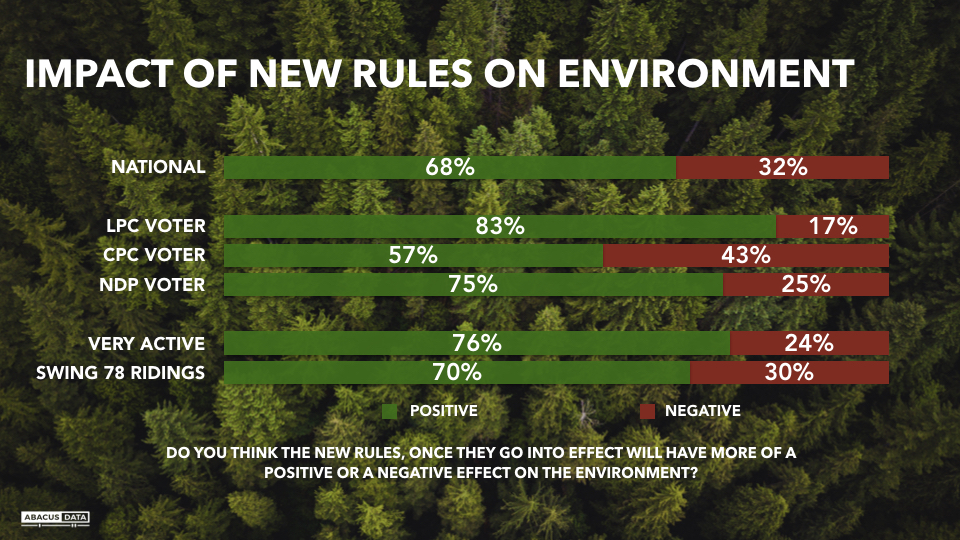

• Among the 37% who have heard about the bill (917 respondents), opinion is generally positive, with 63% saying they think it is a step in the right direction. In Alberta, 42% say the bill is a step in the right direction. The bill has more support among Liberal and NDP supporters, while Conservative voters are evenly split.

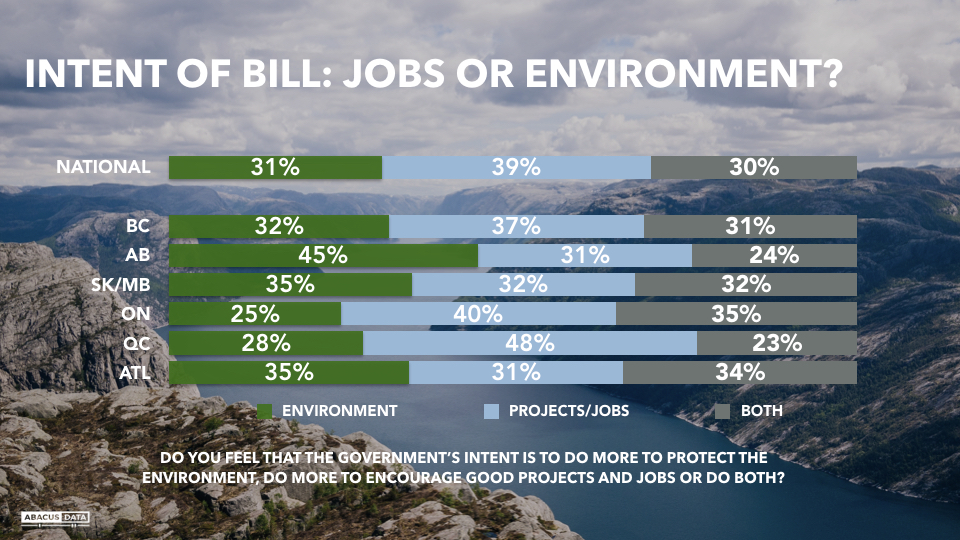

• Among those aware of the legislation, 31% think it is designed to do more to protect the environment, 38% think it is designed to do more to encourage good projects and jobs, and 31% think it is intended to do both.

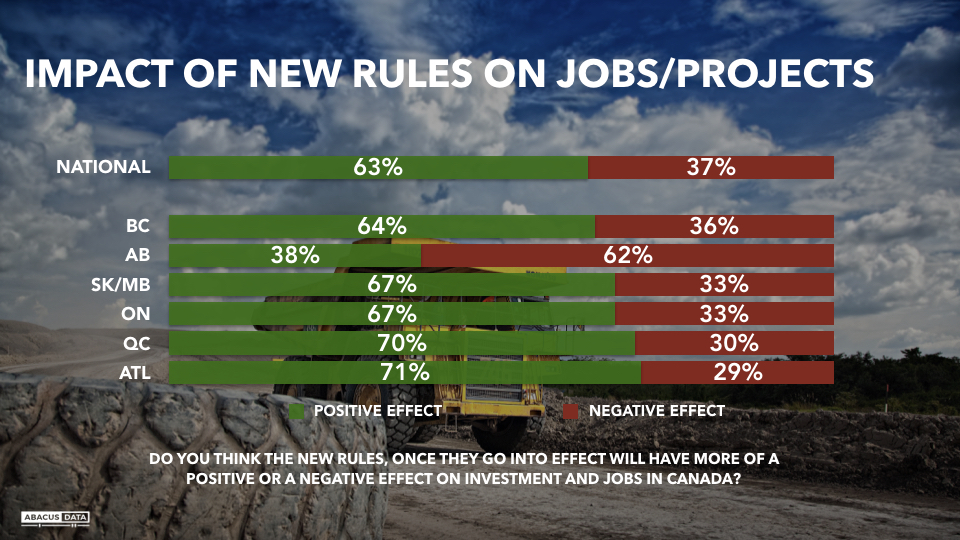

• 62% of those aware think that when C-69 becomes law, it will have a positive effect on investment and jobs in Canada. Albertans are 62% of the view that the impact will be negative, as are 56% of Conservative Party supporters.

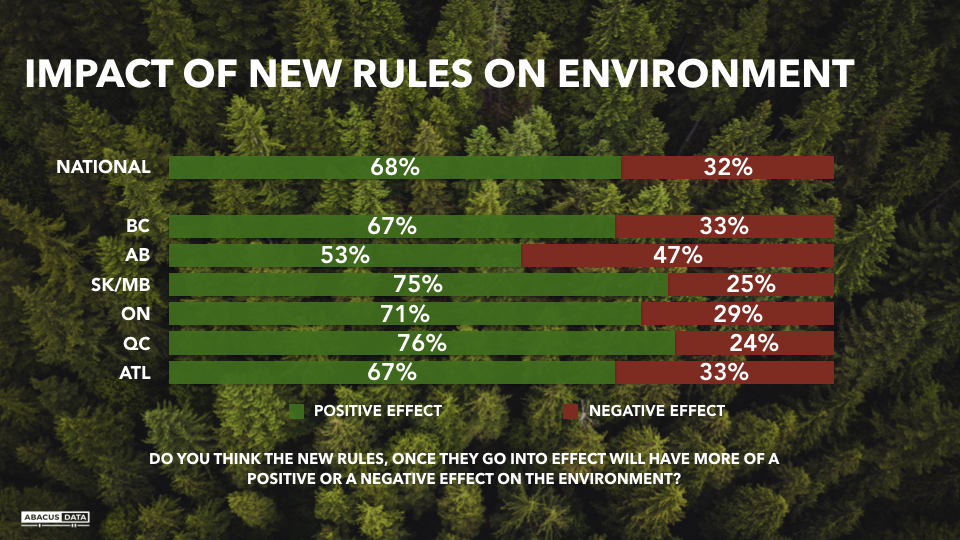

• 68% think C-69 will have a positive effect on the environment, including 53% of Albertans and 57% of CPC supporters.

UPSHOT

According to Bruce Anderson: “UCP Leader Jason Kenney has made opposition to Bill C-69 a major plank in his campaign to win the provincial election in Alberta and federal Conservatives have also been highly critical of the bill.

These findings are another reminder that what preoccupies partisans may or may not always attract a great deal of attention among the general public.

Opinions about the bill are clearly more negative among Albertans and Conservative Party supporters than among others, but the amount of polarization around regional and party lines is perhaps somewhat less than might have been expected given the tone and tenor of the debate.

The results suggest that many people have not developed the impression conveyed by the critics of Bill C-69 – that it is a project killer and will have a chilling effect on investment in the resources sectors.”

METHODOLOGY

Our survey was conducted online with 2,500 Canadians aged 18 and over from February 8 to 12, 2019. A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.0%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

ABOUT ABACUS DATA

We are the only research and strategy firm that helps organizations respond to the disruptive risks and opportunities in a world where demographics and technology are changing more quickly than ever.

We are an innovative, fast-growing public opinion and marketing research consultancy.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail and exceptional value.

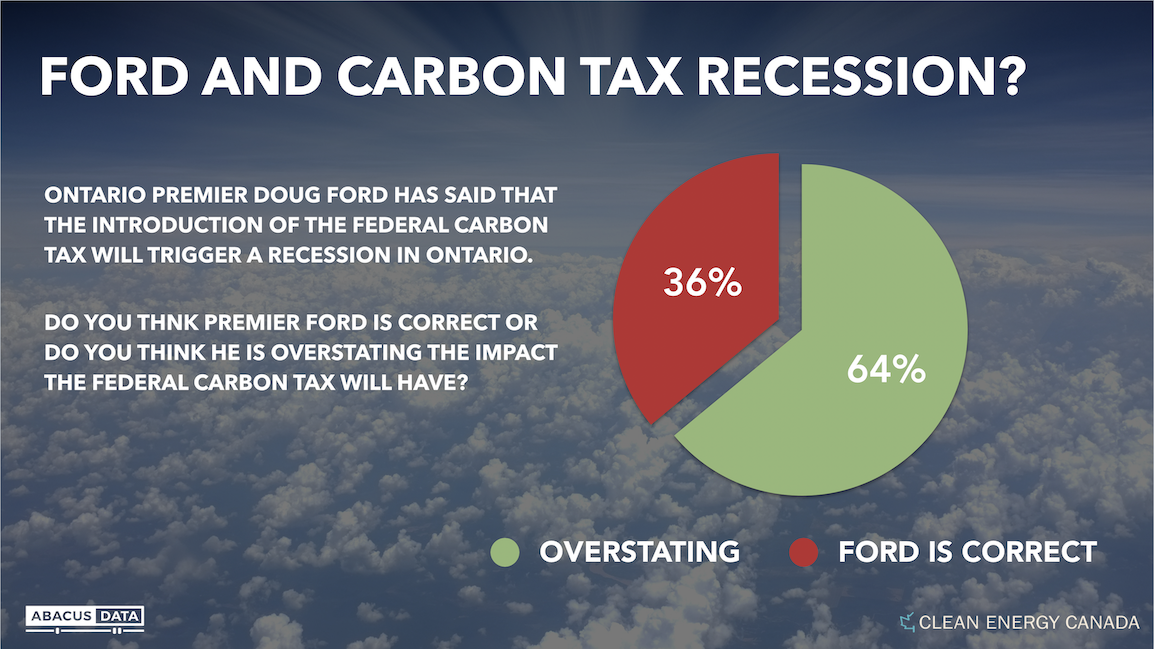

When Ontario Premier Doug Ford claimed the federal government’s carbon tax would cause a recession in Ontario, many economists disagreed. And it seems most regular people do as well.

According to the first in a series of Clean Energy Canada / Abacus Data nationwide polls:

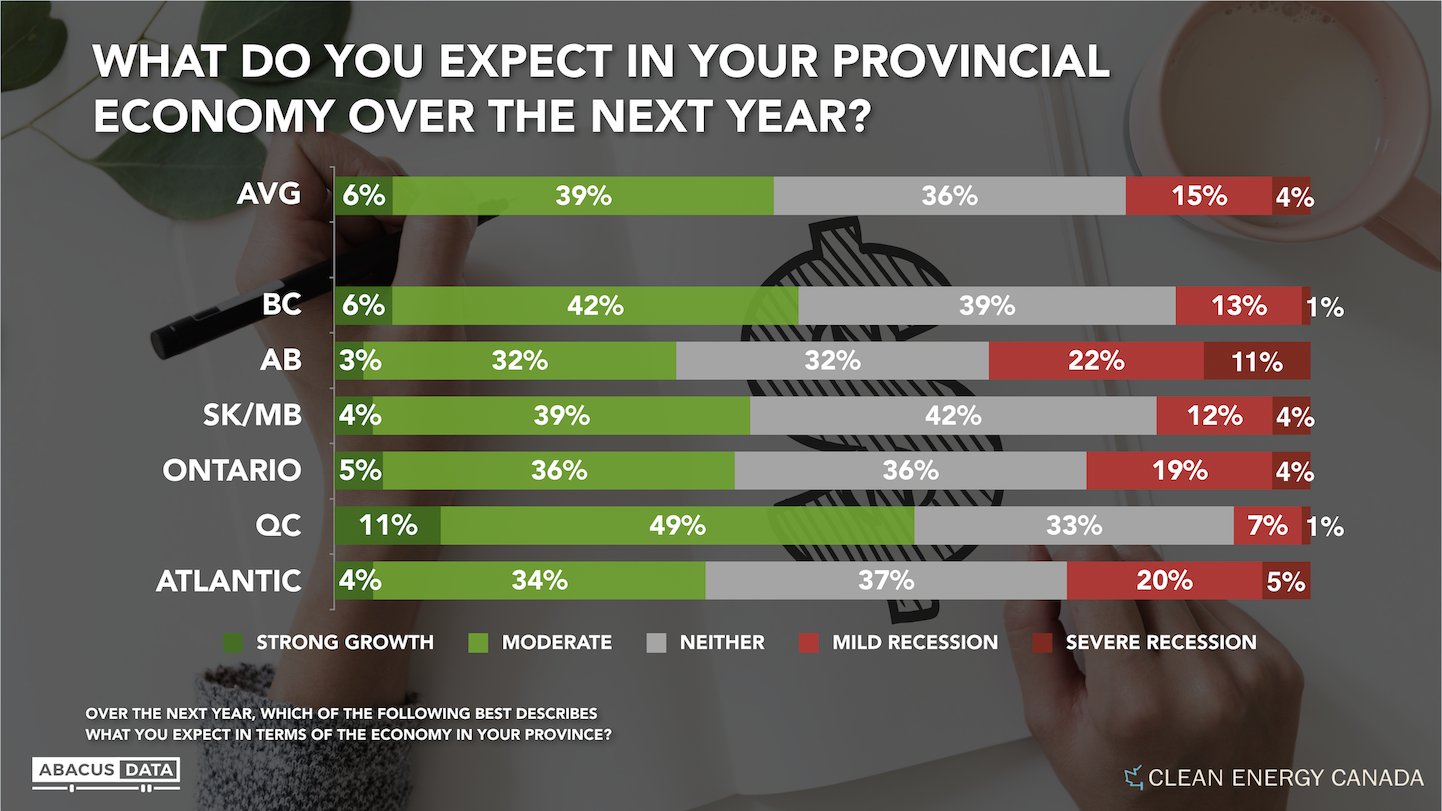

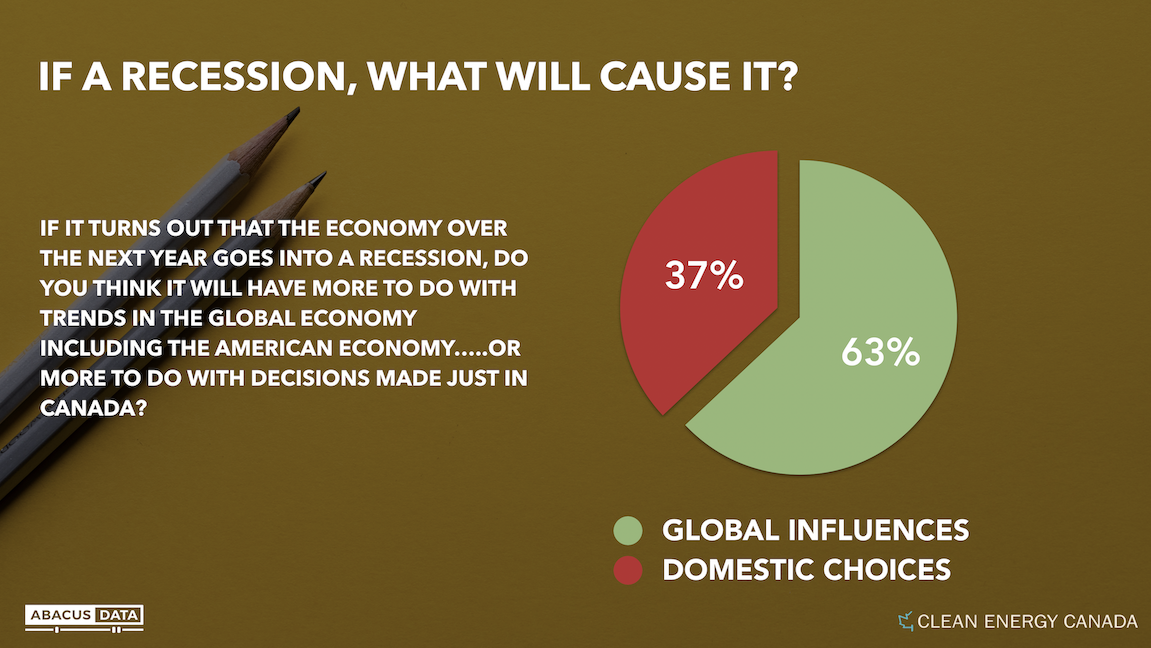

• Few Canadians (19%) expect a recession next year. If there were to be one, most (63%) say it would likely have more to do with global economic trends, than domestic policies.

• When told Premier Ford warned the federal carbon tax would cause a recession in Ontario, almost two out of three across the country (64%), and in Ontario (63%), disagreed, believing he was overstating the impact.

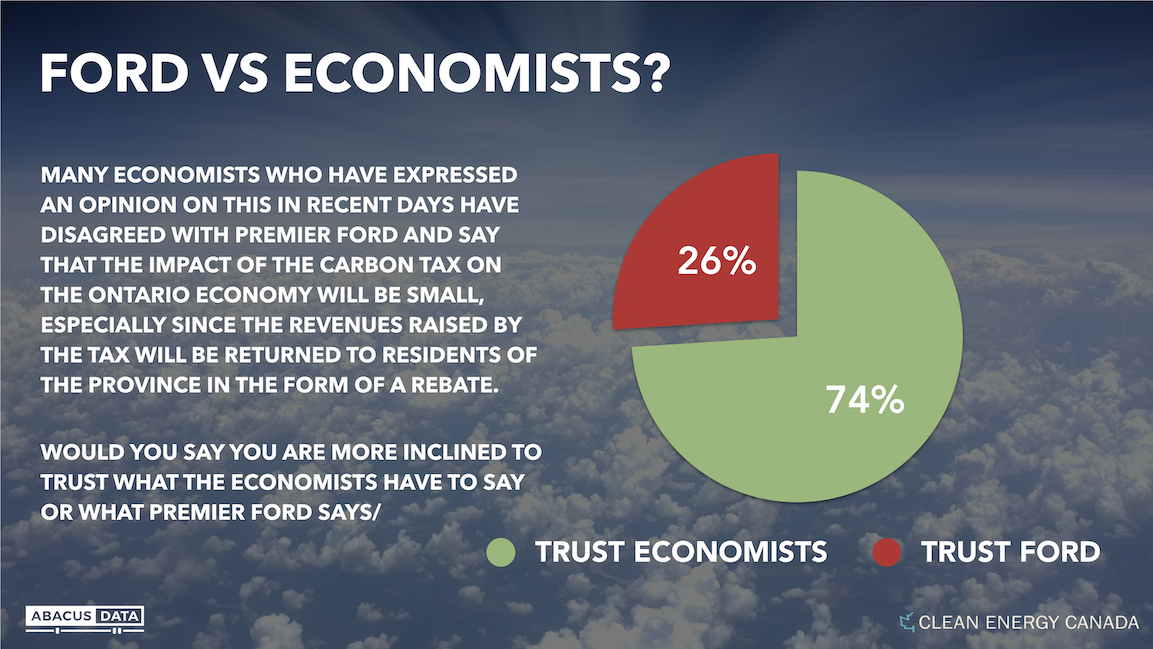

• When respondents were presented with a question which noted that many economists had offered a contrary view, namely that the impact of the tax would be too small to cause a recession, even more people (73% in Ontario, 74% across Canada) rejected Mr. Ford’s contention.

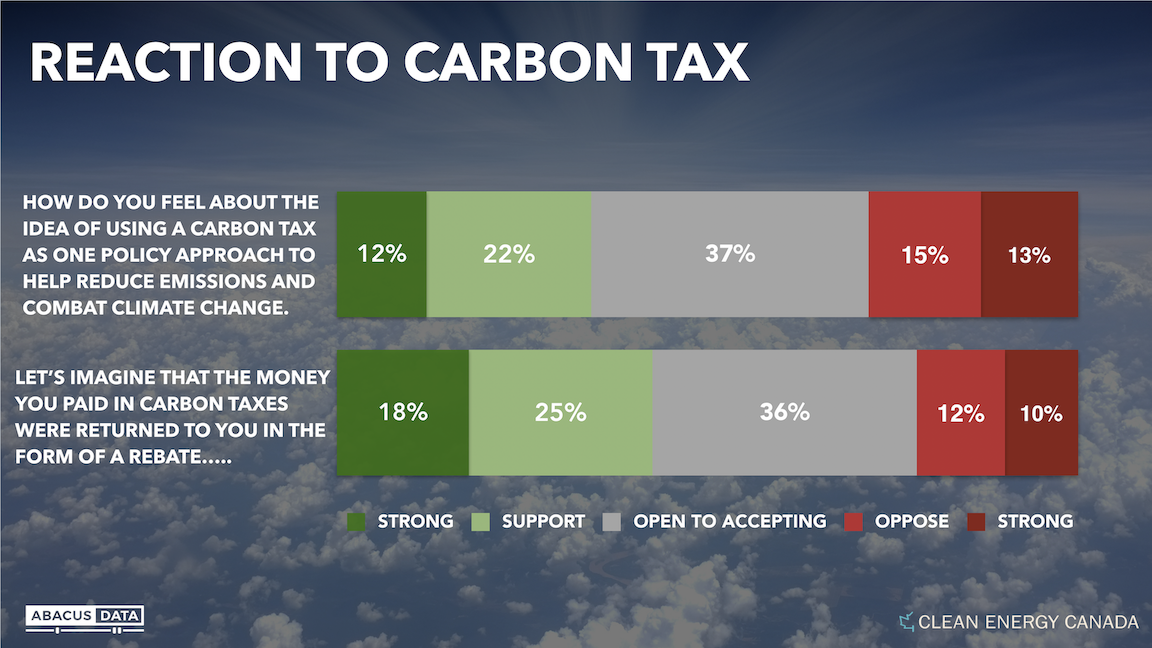

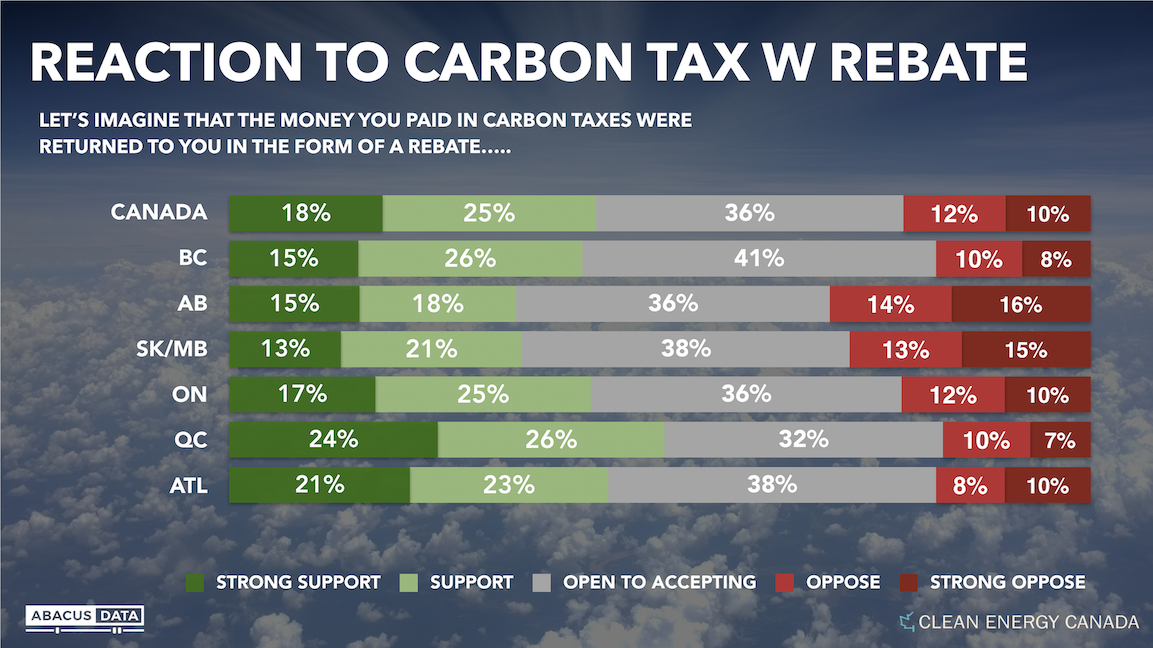

Canadians opinion about the federal carbon tax backstop reveals that 35% support the idea, 28% oppose it and 37% say they are open to considering it. When told of the idea that revenues would be rebated to affected households, support climbs by 9 points, and opposition declines by 6 points.

Opposition to the carbon tax is highest in Alberta, but even there only 41% are set against the idea, which drops to 30% when the rebate is introduced.

In Ontario, 34% support, 37% are open to, and 30% oppose the federal carbon tax. With the rebate, support jumps to 42%, and opposition drops to 22%.

QUOTES

“When it comes to climate policy—like climate science—we can choose who and what we listen to. On issues like pricing pollution where some political leaders are aiming to polarize Canadians, it’s critical that evidence and expertise trump political posturing and sound bites. These results suggest that most Canadians believe evidence and expertise are essential—not optional—for good policy.”

—Merran Smith, Executive Director, Clean Energy Canada

“Canadians don’t love new taxes but they are worried about climate change and want a rational discussion of what we can and should do about it. Time after time, people reject rhetoric which sounds far-fetched or over-reaching, which is how people reacted to Mr. Ford’s assertion. There are many chapters yet to be written in this highly charged debate, but this particular idea turned out badly for opponents of carbon pricing.”

—Bruce Anderson, Chairman, Abacus Data

METHODOLOGY

The survey was conducted online with 2,500 Canadians aged 18 and over from January 30 to February 5, 2019.

A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.0%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

At the start of 2019, we explored public attitudes toward liberalizing alcohol sales in Ontario. The provincial government expanded store hours in December and has started a consultation to look at other ways of changing the way alcohol is sold in the province. Note, this survey was not commissioned or paid for by an organization.

SUMMARY: Overall, we find broad support for liberalizing alcohol sales. Despite widespread satisfaction with the LCBO, most Ontarians support expanding grocery sales to include spirits, allowing convenience stores to sell wine and beer, and allowing private wine shops to open across the province.

THE CONTEXT

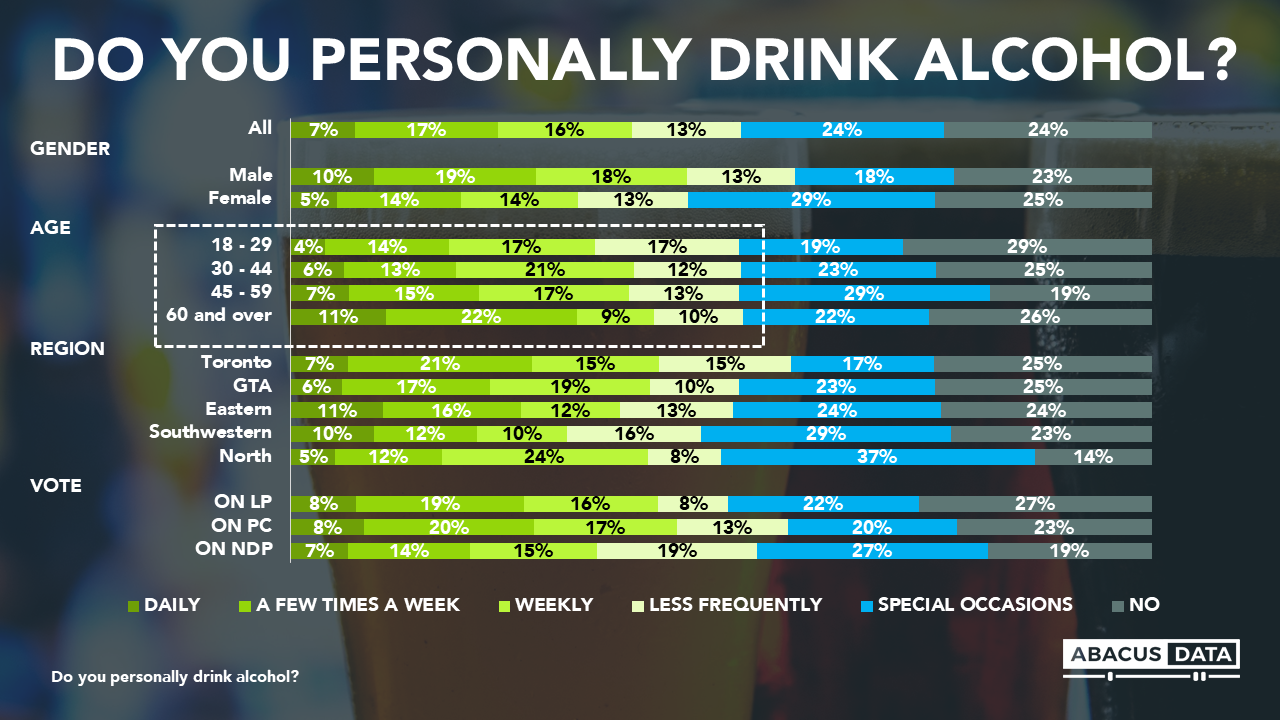

Four in ten Ontario adults drink alcohol at least once per week while 24% say they do not drink alcohol at all. Another 37% drink alcohol less than once a week. Men and older Ontarians are more likely to consume alcohol frequently. There is little variation across provincial party support. Consumption habits are highly correlated to support for liberalizing alcohol sales in Ontario.

Most Ontarians have shopped at the LCBO and a large portion has bought beer or wine from a grocery store. 40% shop at the LCBO regularly or occasionally while 1 in 5 Ontarians say they buy wine or beer at grocery stores regularly or occasionally.

In a very short period of time, many Ontarians have taken advantage of the wine and beer now available in many grocery stores across the province. Despite limited selection, there’s already wide take-up of the channel as a source for alcohol.

Ontarians are also generally satisfied with their experience at the LCBO. Satisfaction with the LCBO is particularly high with its selection, overall shopping experience, and the staff available to help customers. Most also say they are satisfied with the selection of new and interesting products and even the price.

Views about the experience buying wine and beer at grocery stores similar to that at the LCBO. Most Ontarians who have purchased those products at a grocery store report being generally satisfied with all aspects of the experience, although the intensity of satisfaction is more muted than with the LCBO suggesting there may be a desire from consumers for more choice and a better experience within grocery stores.

REACTION TO IDEAS TO LIBERALIZE ALCOHOL SALES IN ONTARIO

We wanted to gauge support or opposition to a number of ideas being floated around by the Ontario government and stakeholders to liberalize alcohol sales in the province. For all ideas, a majority of respondents either strongly support or support the idea demonstrating broad acceptance and support for liberalizing alcohol sales.

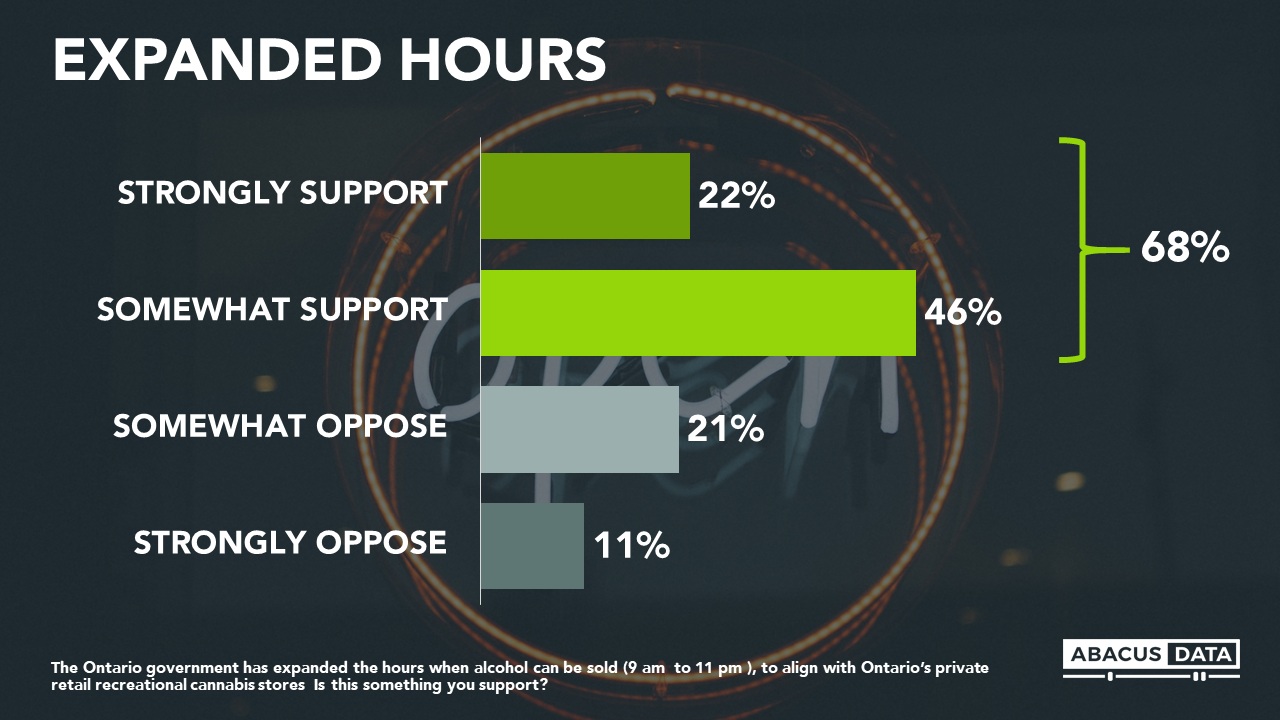

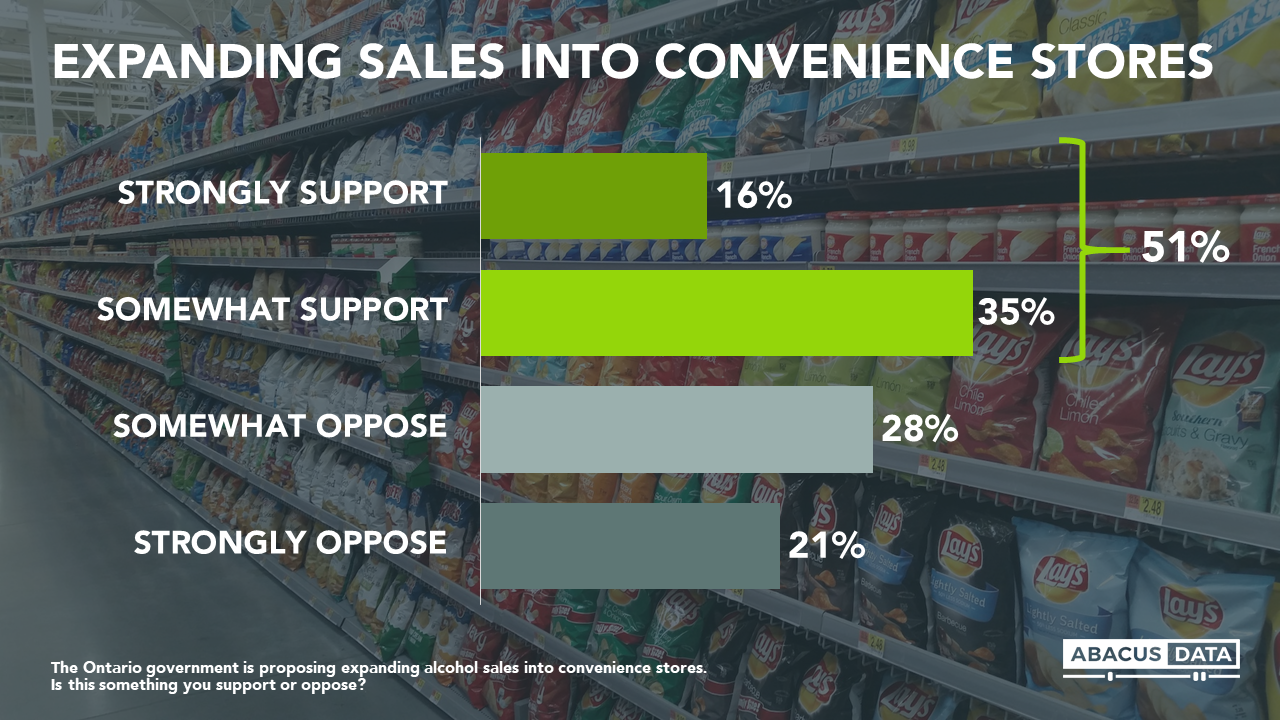

For example, two in three support the provincial government’s decision to extend the hours the LCBO and private alcohol retailers can sell alcohol in the province. There’s no political divide on this idea and finds support across age groups, regions of the province and among both men and women.

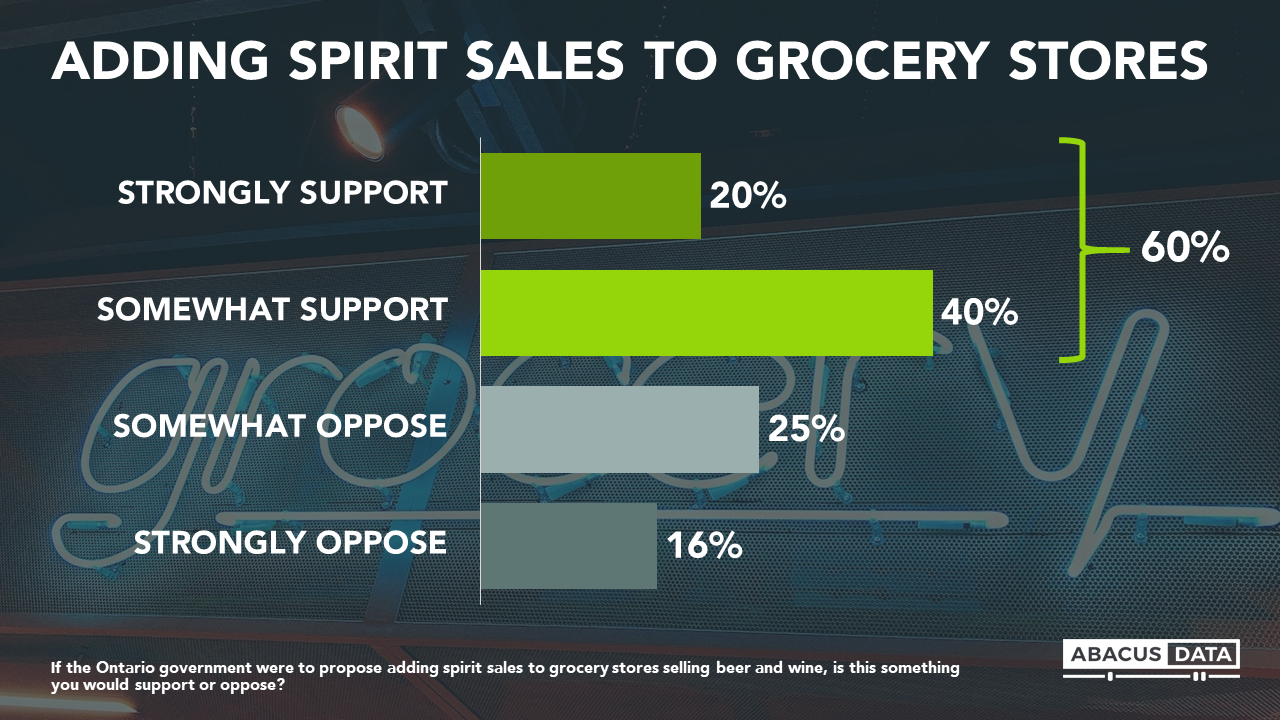

Six in ten Ontarians would support adding spirits onto grocery store shelves along with beer and wine with strong support four points higher than those who strongly oppose the idea. Support for allowing grocery retailers to add spirits to their shelves crosses all age groups (although younger Ontarians are more supportive) and party supporters.

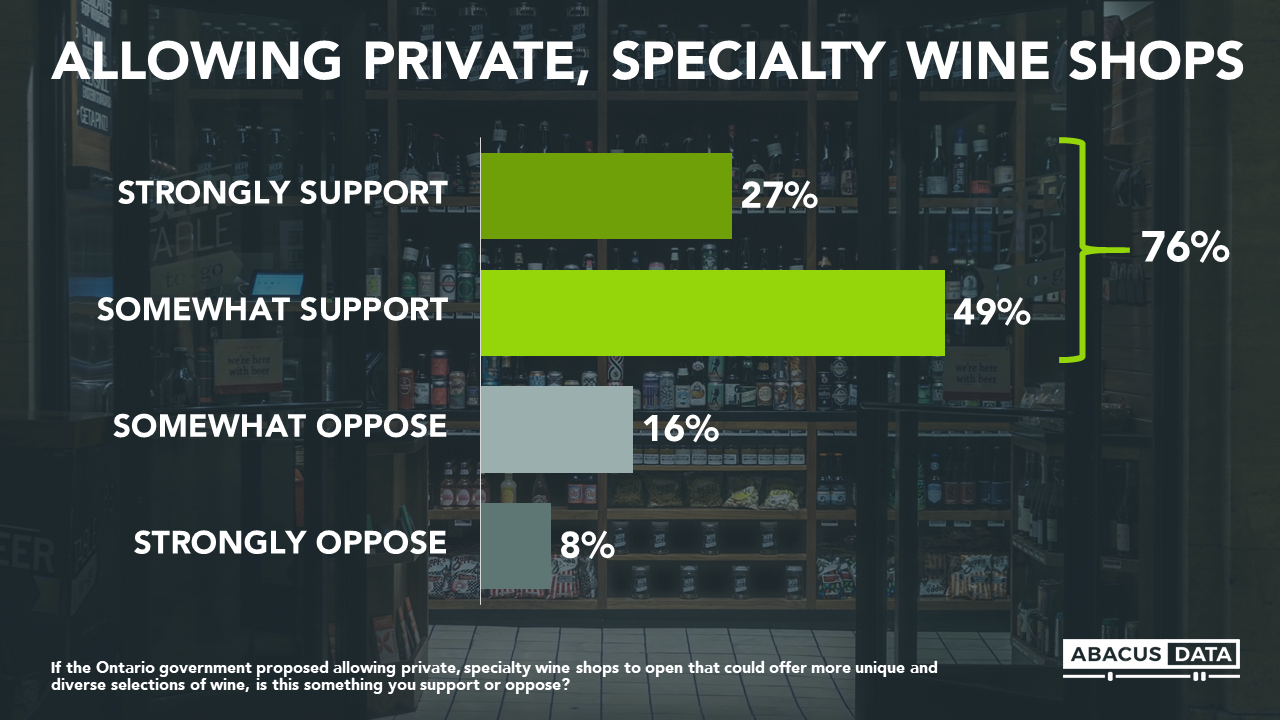

Most Ontarians would also support allowing private, specialty wine shops to open in Ontario. This idea found the broadest support with 3 in 4 supportive and only 8% strongly opposed.

Although more divisive, one in two Ontarians (51%) support expanding alcohol sales into convenience stores with support highest among Ontarians under 45, regular consumers of alcohol, and among PC and Liberal party voters.

UPSHOT

As the Ford government consults with stakeholders and the public on its plan for liberalizing alcohol sales in Ontario, our research finds broad support for many forms of liberalizing alcohol sales.

Expanded hours, expanded selection at grocery, extending beer and wine sales to convenience stores, and allowing specialty wine shops to open are supported by at least a majority of Ontarians, and in some cases, large majorities.

Younger Ontarians and men are particularly keen to see more liberalization but support is broad across all demographic, regional, and political groups.

It seems that this is a policy idea with legs as consumers seek more choice, customization, and competition in the province’s alcohol market.

For more information about this survey, please contact David Coletto at david@abacusdata.ca and follow him on Twitter @colettoD.

METHODOLOGY

Our survey was conducted online with 800 Ontarians aged 18 and over from January 11 to 14, 2019. A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 3.5%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Ontario’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

ABOUT ABACUS DATA

We are the only research and strategy firm that helps organizations respond to the disruptive risks and opportunities in a world where demographics and technology are changing more quickly than ever.

We are an innovative, fast-growing public opinion and marketing research consultancy.

We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail and exceptional value.

Find out more about how we can help your organization by downloading our corporate profile and service offering.

Will climate change and the environment be a ballot box question this year?

David Coletto joins the team at the Sixth Estate and a stellar line up of guests to discuss the issue.

Hosted by veteran journalist Catherine Clark, the show is broken down into three segments. In The Pulse, we ask opinions of expert guest pundits on pressing issues and interacts with the audience through polling technology to gain their reactions. Next in the The Policy segment, Catherine Clark invites newsmakers to the stage to talk about themed issues from their unique perspectives. In between interviews, Catherine asks the audience to submit questions electronically and vote up questions they want answered. After all guests have been interviewed, they remain on stage for the final segment called The People. Here Catherine engages the newsmakers in discussion by asking the most popular audience-generated questions.

Watch the full episode below and learn more about the show here.

The research cited below is sourced from an in-depth study of how consumers’ adoption of emerging technologies intersects with data privacy and public trust. If you would like to see more analysis from our work, please reach out to Executive Director ihor@abacusdata.ca for more information.

-Direct to consumer genetic testing driven by ancestry; health a tertiary consideration.

-Genetic genealogy industry grappling with trust deficit.

-Consumers more comfortable sharing genetic data than movement, financials, private messages.

Know thyself. Not just ancient Greek philosophy, but a marketing proposition genetic genealogy firms like 23andMe, AncestryDNA and MyHeritage are using to encourage consumers to try a new suite of at home testing services. In a departure from selling glossies to travel starved suburbanites, even National Geographic has gotten in on the action.

Having evolved in the last decade from the sole domain of labs & hospitals to an easy to use, saliva-based, direct-to-consumer offering, these genetic testing kits offer a seductive sell: a robust, scientific estimate of who you are, how you’re built, and where you’re from.

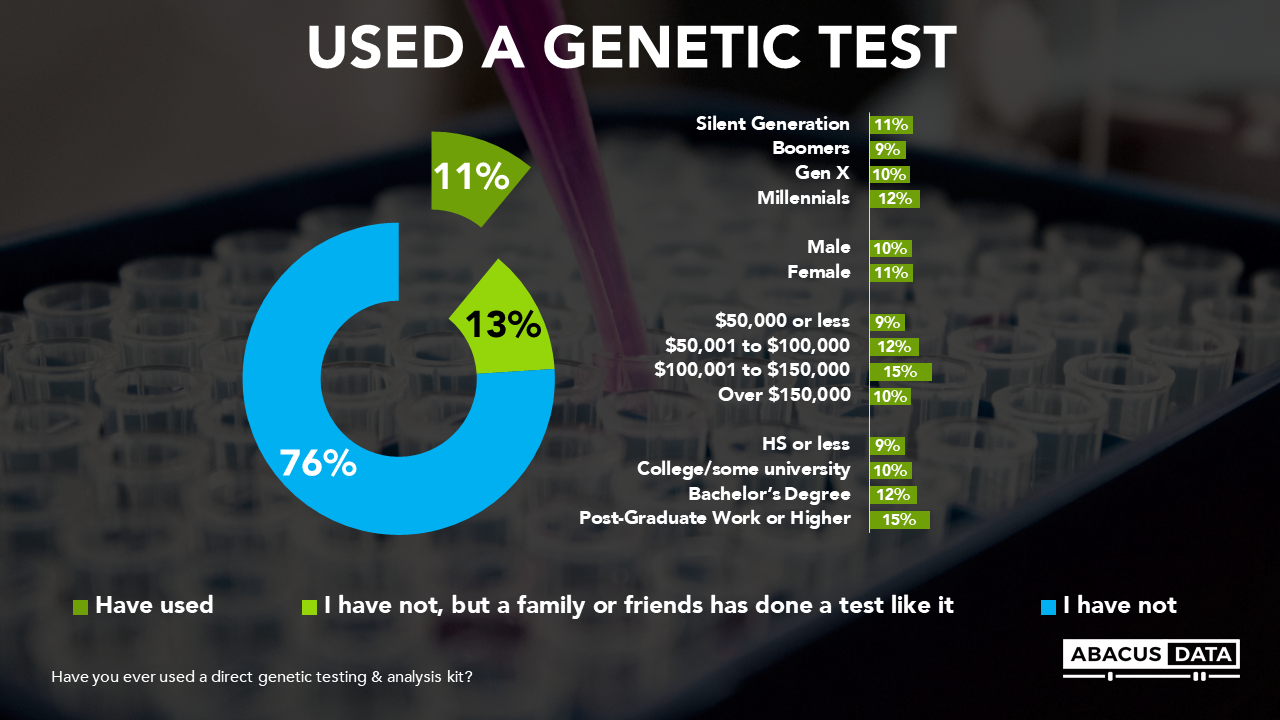

When we surveyed Canadians last summer (2018), about 11% of the adult population – (~3 million Canadians) – reported having used a direct genetic testing & analysis kits. Rich or poor, old or young, the technology has been used in equal measure by every group.

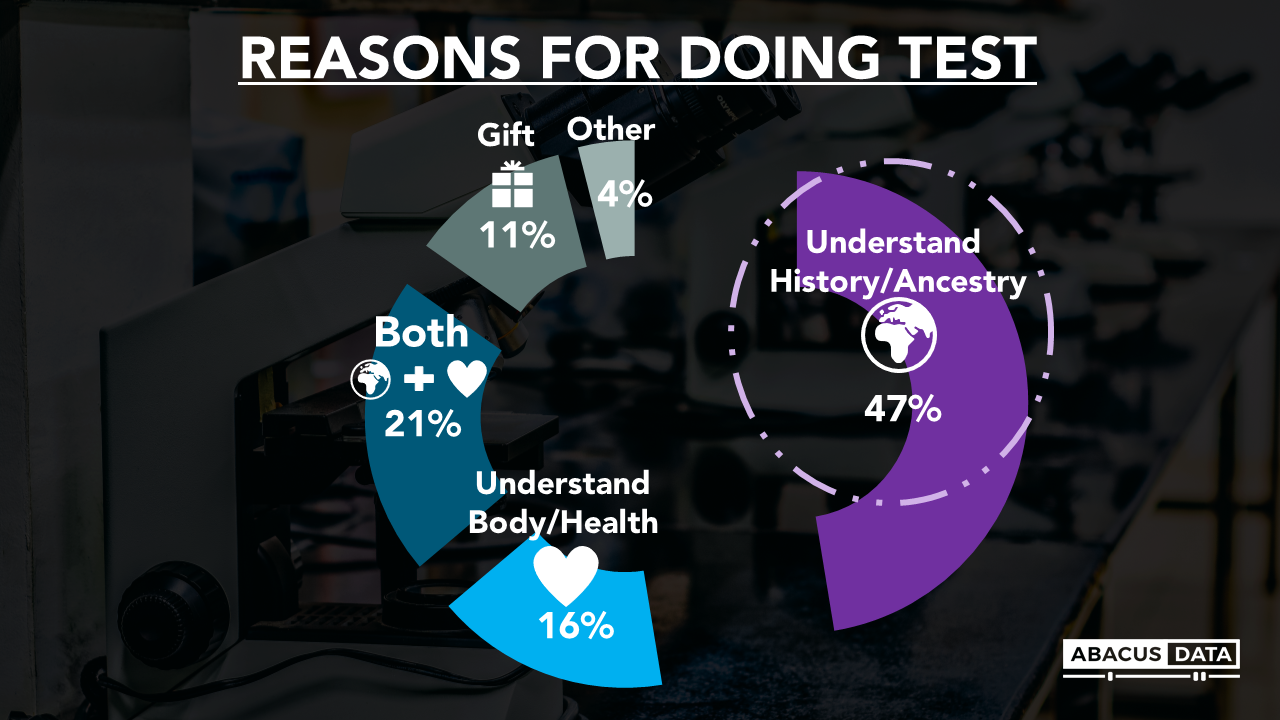

Though there are plenty of health applications, understanding history/ancestry is the big driver – the reason 7 of every 10 kit users ordered the test. Marketing at its core is an appeal to an individual’s identity. Have a product whose direct value proposition is telling you who you are and where you come from? Seems like an easy sell.

Yet in our age of data breaches and institutional trust deficits things are not so straightforward. Even if a life of crime or misattributed paternity surprises do not seem likely in your future, one could imagine why Canadians might be hesitant to trust companies with their data.

And so we surveyed those who have not taken the test to rate their feelings around the value proposition between several pairs of polarities, including whether in their view:

There is more benefit to the consumer vs. more benefit to the companies collecting the data.

The benefits outweigh the risks vs. risks outweigh benefits.

Information is being kept securely vs. information is insecure.

Information is used only for the benefit of consumer understanding vs. information is used in many other ways that benefit the company.

The prevailing sentiment is one where the fundamental trade off is seen as inherently tipped against the customer. More see risks than benefits, information is assumed to be unsecure. Crucially, consumers see far more upside for the companies on the receiving end of the data than they do for themselves. The balance of opinion swings the other way among test users, with many more believing that the technology benefits the consumer more than the company.

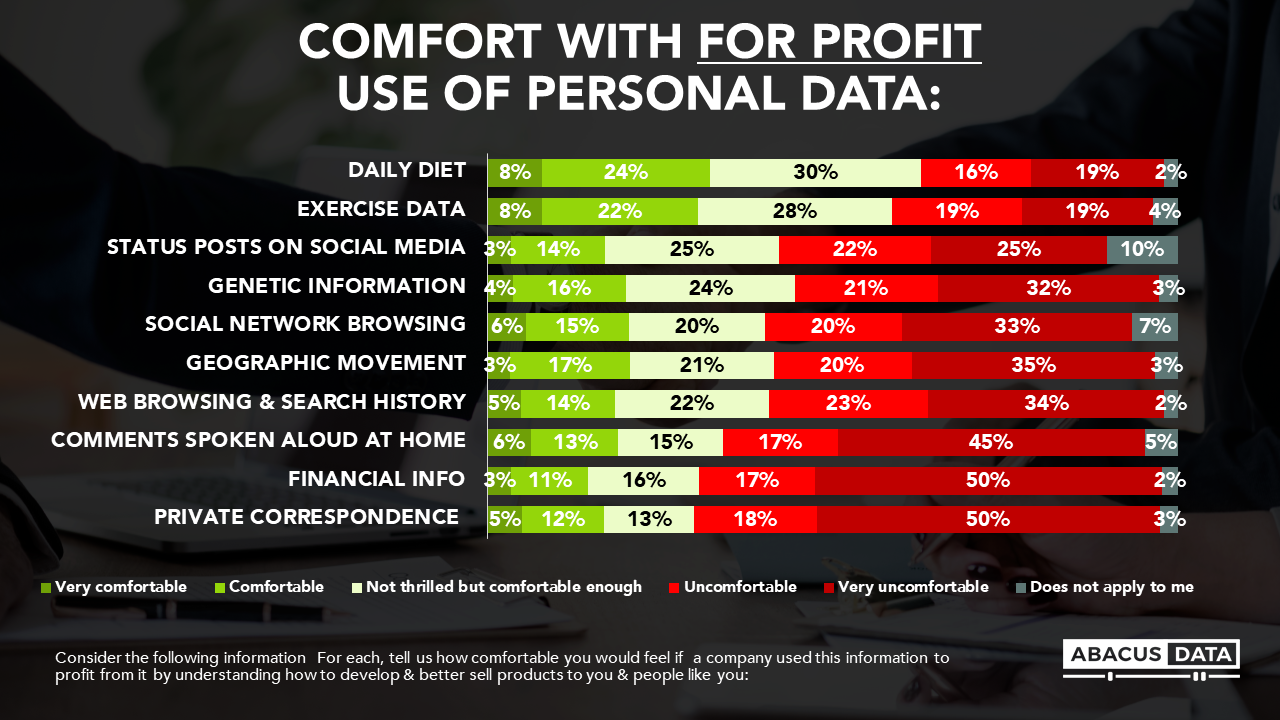

This attitude is not unique to genetic information. When we explored the relative comfort/discomfort Canadians felt with companies using various information sets for-profit, most were comfortable with the use of two health adjacent areas: daily diet and exercise data.

Genetic information is in a secondary tier of comfort along with social network activity – about half are opposed to corporate use of the information, while a little less than half are comfortable enough with it. It probably says something profound that financial information is considered far more sacrosanct in this context than your genetic code.

Despite these reservations, about 60% of the adult population in Canada were open to ordering a home kit genetic test. Most are in no hurry, and 18% would like to do one or are actively looking into it, leaving much room to grow for the sector.

This discussion exists in a specific cultural context – one where institutional trust is in decline, and data breaches raise public concern about the integrity of companies and the security of information. Public opinion is thermostatic and will shift depending on how much consumers perceive is being done on the part of regulators and industry to safeguard their data. If the scales are tipped towards an unregulated wild west, we will likely continue to see potential customers put up walls and assume the worst about industry’s intent. If industry can effectively demonstrate safety, responsibility and social benefit – with the “help” of regulators or without – expect these perceptions to decline.

Open up a business publication and you’ll often read something to the effect of “data is the new oil”. I find this a fantastic metaphor not due to the inherent validity of the claim, but because there is a parallel lesson in social license here. The resource industry (through much trial and more error) had the opportunity to learn many lessons over the decades on how central community buy in and public trust is to long term corporate health & profitability. For companies handling sensitive data, similar lessons exist, ones presently being learned by a certain social network. A proactive and consistent story of how these services could contribute to a social net benefit would go a long way in making Canadians more comfortable about the prospect of taking one of these tests.

Methodology

The survey was conducted online with 1,500 Canadian residents aged 18 and over from August 15th to 20th, 2018. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The Marketing Research and Intelligence Association policy limits statements about margins of sampling error for most online surveys. The margin of error for a comparable probability-based random sample of the same size is +/- 2.53%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

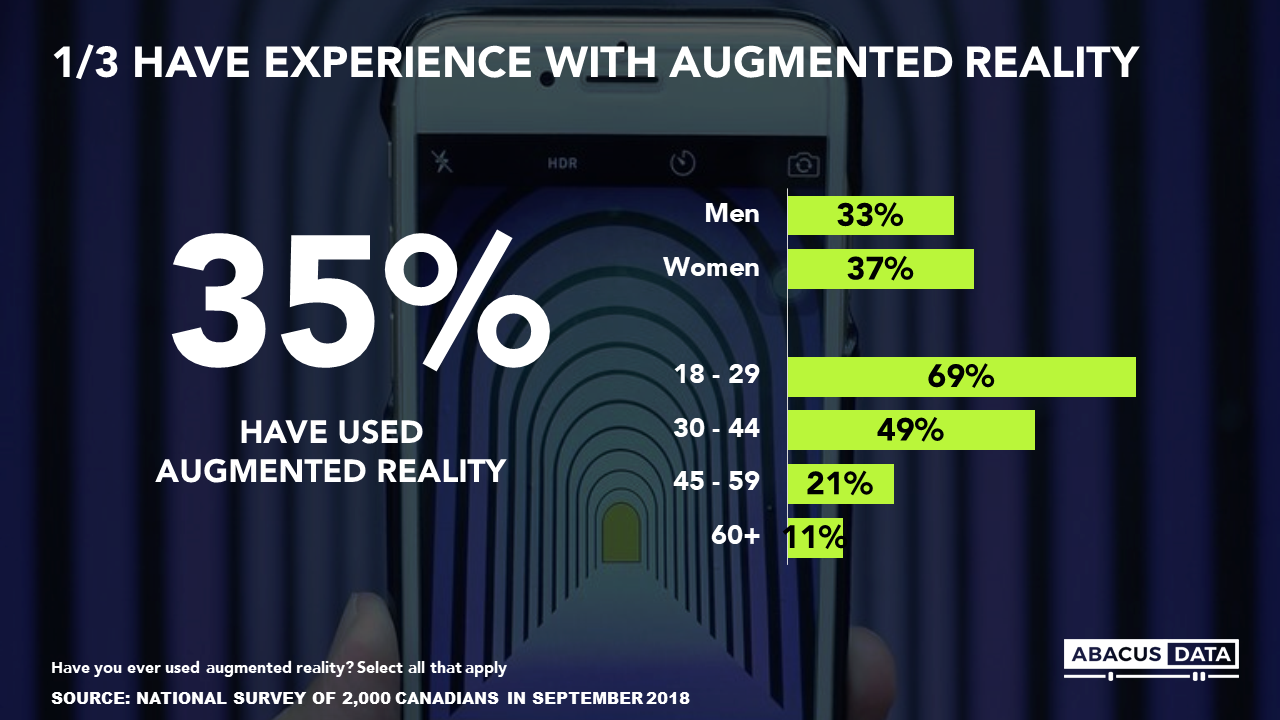

Over a third of Canadians have already used Augmented Reality (AR) and most are interested in seeing the technology in retail spaces.

Those under 45 are especially enticed by the idea of AR being integrated into their retail experience (75%).

Like many new technologies, AR use in retail will probably be driven by curiosity and novelty at first, but there is a signaling from consumers that AR could enhance the shopping experience.

Augmented Reality has the potential to be a one-two punch for retailers: First, by drawing consumers back into their physical stores through the novelty of AR, then enticing them to open their wallets through the enhanced user experience AR provides.

AR isn’t confined to retail disruption either. See the pdf at the bottom of this page for a short story-deck with some exciting stats and potential applications for different industries, including retail, museums and tourism, and entertainment facilities.

This article only scratches the surface of our study. For a comprehensive deck with an in-depth breakdown of all our findings please email Maciej Czop, Senior Research and Communications Consultant at Abacus Data.

The Evolution of Shopping

Remember, in the infancy of the World Wide Web, when only lunatics gave out their credit card numbers over the internet? These days, that fear is a vague memory and it’s fading quicker than shipping times for Prime Delivery.

Online retail has exploded in the past decade with the advent of trusted online payment systems, cheap or even free shipping, intuitive user interfaces, and a massive shift in consumer culture that makes it feel like we’ve been buying clearance-sale socks through our smartphones while lounging in bed since the dawn of the modern age.

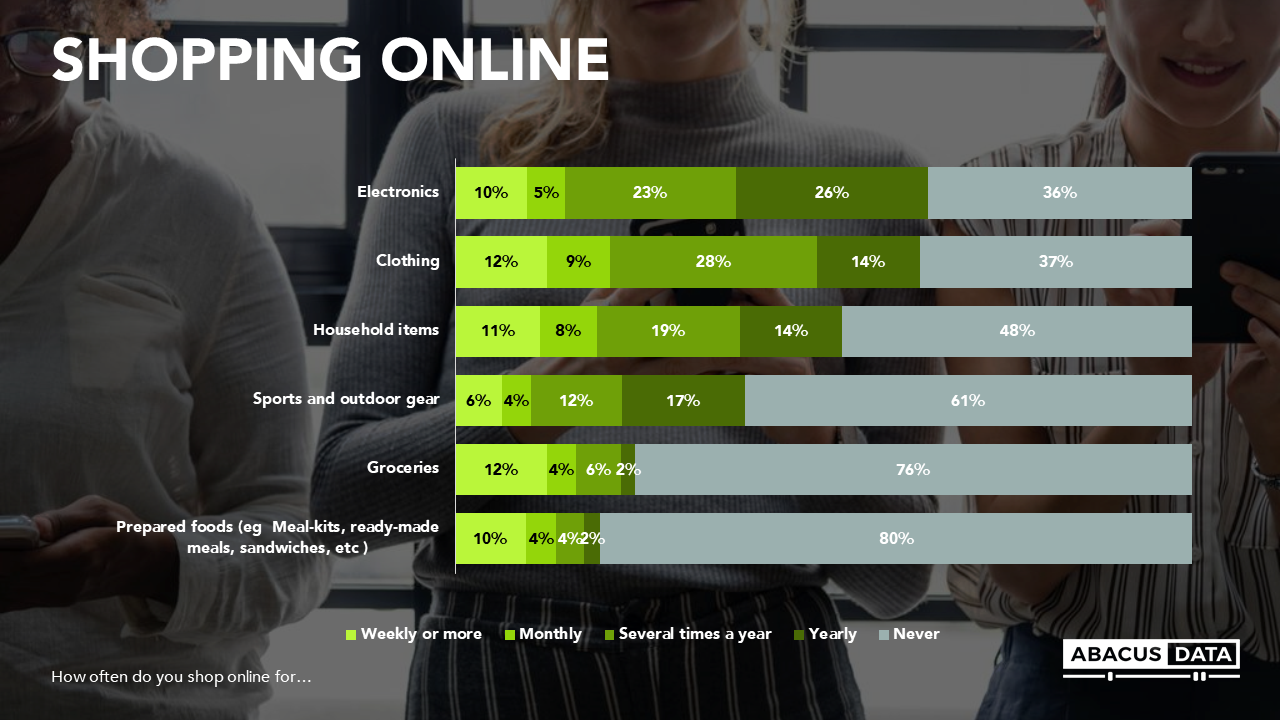

The obvious online purchases, like electronics and clothing, are leading this digital transition with almost 2/3’s of Canadians telling us that they shop for these online at least once a year. Traditionally less digital-friendly purchases are gaining traction as well. Just over half (52%) of Canadians bought household items like dish soap and laundry detergent online and about a quarter (24%) purchased groceries online in the past year.

With consumers moving significant portions of their spending online, and many retail trends pointing to strong and consistent growth in the digital space, where does this leave the brick-and-mortar shop? Some of the more intrepid and creative retailers are exploring how Augmented Reality (AR) could entice consumers back into their physical stores.

What is Augmented Reality (AR)?

Let’s start with the fundamentals. Augmented Reality is an enhanced environment as viewed through a screen or other display, produced by overlaying computer-generated images, sounds, etc. on the real-world. AR is half-way to virtual reality, but instead of a completely digital world, AR enhances the physical space around us. Think of the much-hyped Google glasses and you’ll get the idea, but AR can be as simple as interacting with a physical object/space through your smartphone, or a kiosk screen, or as complex as a Pokémon franchise revival.

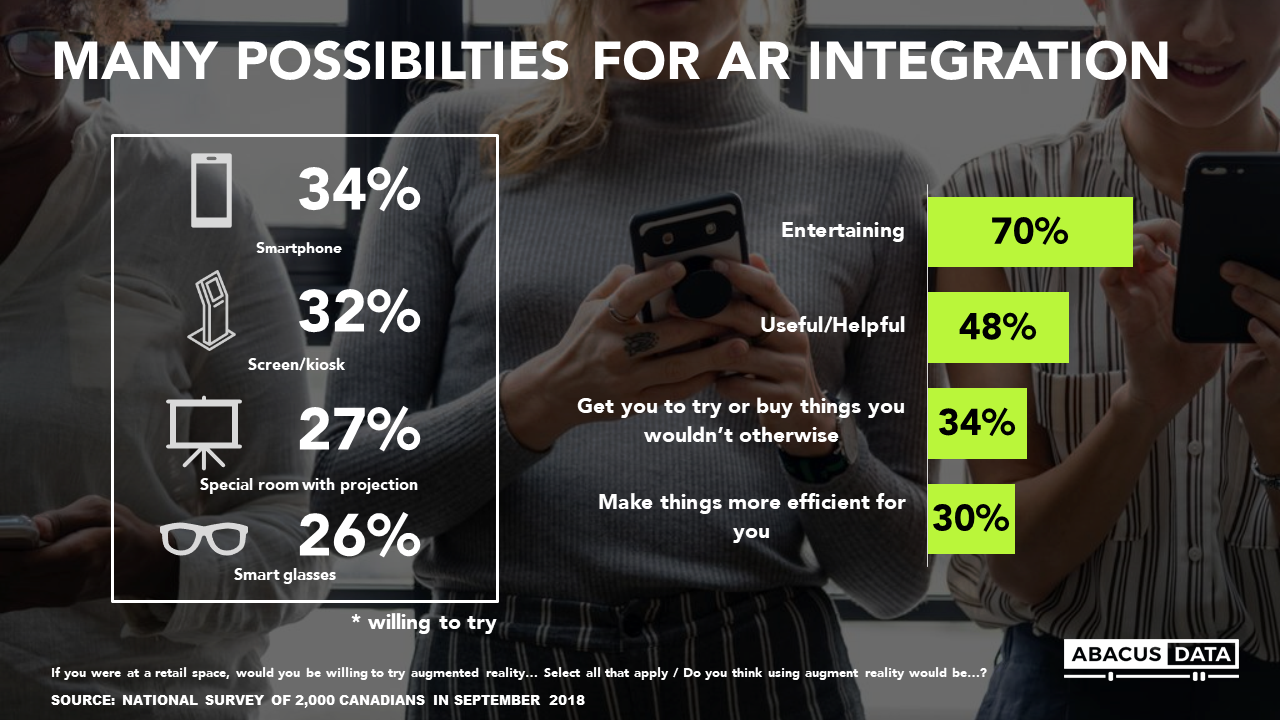

A surprising number of Canadians are already using AR. Just over a third (35%) of all Canadians have used augmented reality, and this number rockets to half (49%) of 30-44 year-olds and almost 7 in 10 (69%) 18-29 year-olds.

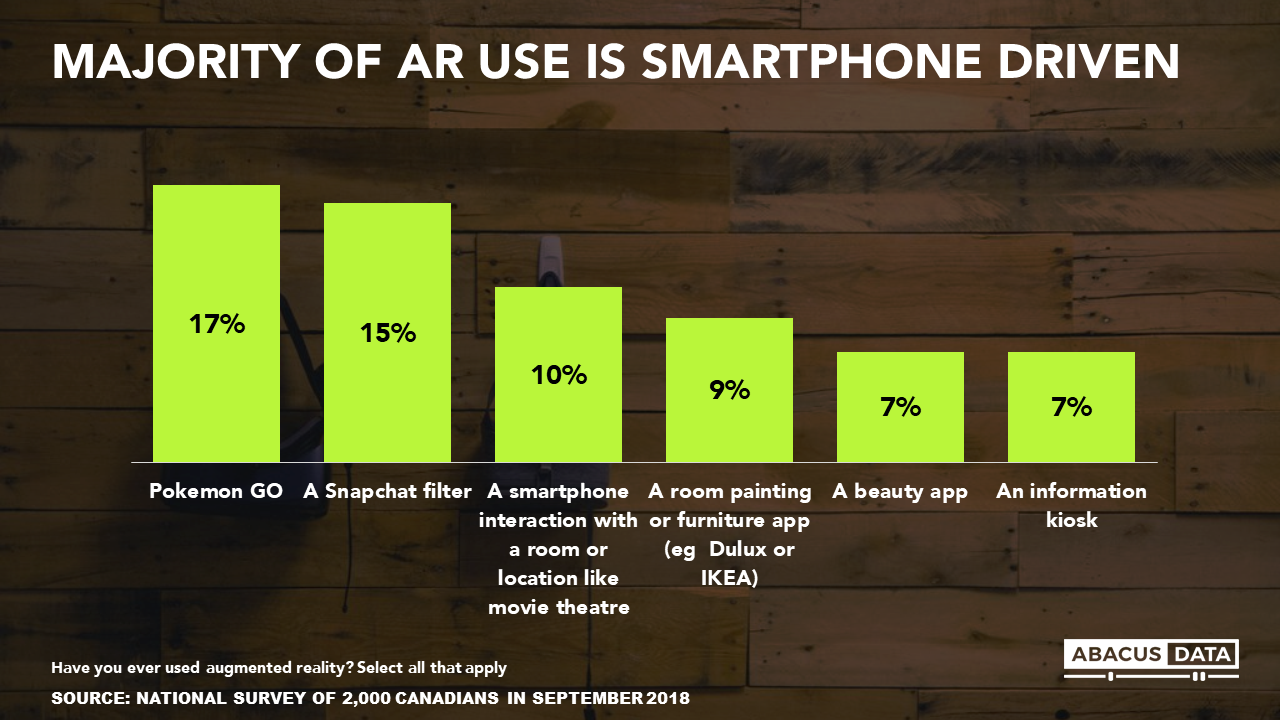

Smartphone games and social media apps are leading augmented reality use: 17% of Canadians have used AR through Pokémon GO and 15% through a Snapchat filter. But AR’s appeal doesn’t end with trivial distractions on phones, and this is where retailers’ ears will perk up: 1 in 10 Canadians have used a smartphone to interact with a room or used an AR app to try different paint colours or furniture arrangements, while 7% have used beauty apps to try make-up on a simulation of their face and the same number have used AR at information kiosks.

AR’s Potential in Retail

Looking beyond the way AR is currently being used, we also wanted to measure AR’s potential as it pertains to the retail space in Canada.

What we found was very promising for AR innovators and enthusiasts: Most Canadians (59%) are willing to try AR in a retail space and this climbs to a large majority of 18-29 year-olds (82%) with 30-44 year-olds not far behind (70%).

Canadians think clothing and entertainment are the most popular potential uses for retail AR. Those willing to try AR say they are most interested in trying-on clothing without having to use a change room (26%) and using it for fun at an arcade or theatre (25%).

However, consumers are also interested in how AR can help them make purchases, such as providing more information and demonstrations for electronics (18%), for beauty and cosmetics to see what you look like without physical application (10%), and grocery shopping to get more information about products such as nutrition and how foods fit into personal meal plans (8%).

The main driver of potential retail AR use seems to be the “novelty” factor: 7 in 10 said using AR would be entertaining. Retailers would be wise to make sure whatever implementation of AR they attempt is easy, intuitive and fun for consumers to use.

Many Canadians are anticipating more serious benefits from AR as well. Almost half (48%) said AR would be useful/helpful, over a third (34%) said it would get them to try or buy things they wouldn’t otherwise, while 3 in 10 believe it would make shopping more efficient.

No Perceptual Barriers to AR and lots of Consumer Interest

The big story is that many Canadians are interested in seeing AR in retail spaces, especially those under 45. Like many new technologies, AR use in retail will probably be driven by curiosity and novelty at first, but there is a signaling from consumers that AR could enhance the shopping experience. Augmented Reality has the potential to be a one-two punch for retailers: First, by drawing consumers back into their physical stores through the novelty of AR, then enticing them to open their wallets through the enhanced user experience AR provides.

Physical retail may never match the convenience of online shopping, but these new augmentation technologies can give consumers something experiential, useful and valuable that draws them back to brick and mortar stores. At the very least, Canadians don’t seem to be opposed to or disinterested in retail AR, but there is also evidence that a significant portion of Canadians explicitly desire it as part of their purchase decision making due to its perceived benefits.

Big Opportunities for Retailers who get AR “Right”

Perhaps the most interesting facet of AR is that Canadians already conveniently carry a powerful piece of AR tech around with them wherever they go: the smartphone. This is a major advantage in the consumer culture arms race and a significant opportunity. Now it’s up to attentive retailers to make retail AR easy and enticing, and give consumers a reason to take their phones out of their pockets.

In an age of big-budget, at-your-fingertips TV shows a la Netflix, Amazon prime, etc., expectations for great story telling and sumptuous aesthetics have never been higher – if you want consumer attention then the production value of AR better be of high quality and unique creativity or retailers risk leaving even the most interested users unimpressed. A neat example of a creative approach to AR is a recent trend seen on some wine labels to tell a story to potential customers.

Our research shows that shoppers expect to be entertained as well as informed, and a short AR interaction that tells a brand/product story can enhance what might otherwise be a mundane experience and keep customers coming back for more – IF the effort is thoughtful, fun, attractive and polished.

AR isn’t confined to retail disruption either. Here is a short story-deck with some exciting stats and potential applications for different industries, including retail, museums and tourism, and entertainment facilities.

This article only scratches the surface of our study. For a comprehensive deck with an in-depth breakdown of all our findings please email Maciej Czop, Senior Research and Communications Consultant at Abacus Data.

Methodology

The survey was conducted online with 2,000 Canadian residents aged 18 and over from September 15th to 20th, 2018. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The Marketing Research and Intelligence Association policy limits statements about margins of sampling error for most online surveys. The margin of error for a comparable probability-based random sample of the same size is +/- 2.19%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

As 2018 wraped up we asked Canadians to tell us how likely and how desirable a series of possible events would be in the coming year. Here’s what the results revealed:

HOPES FOR 2019

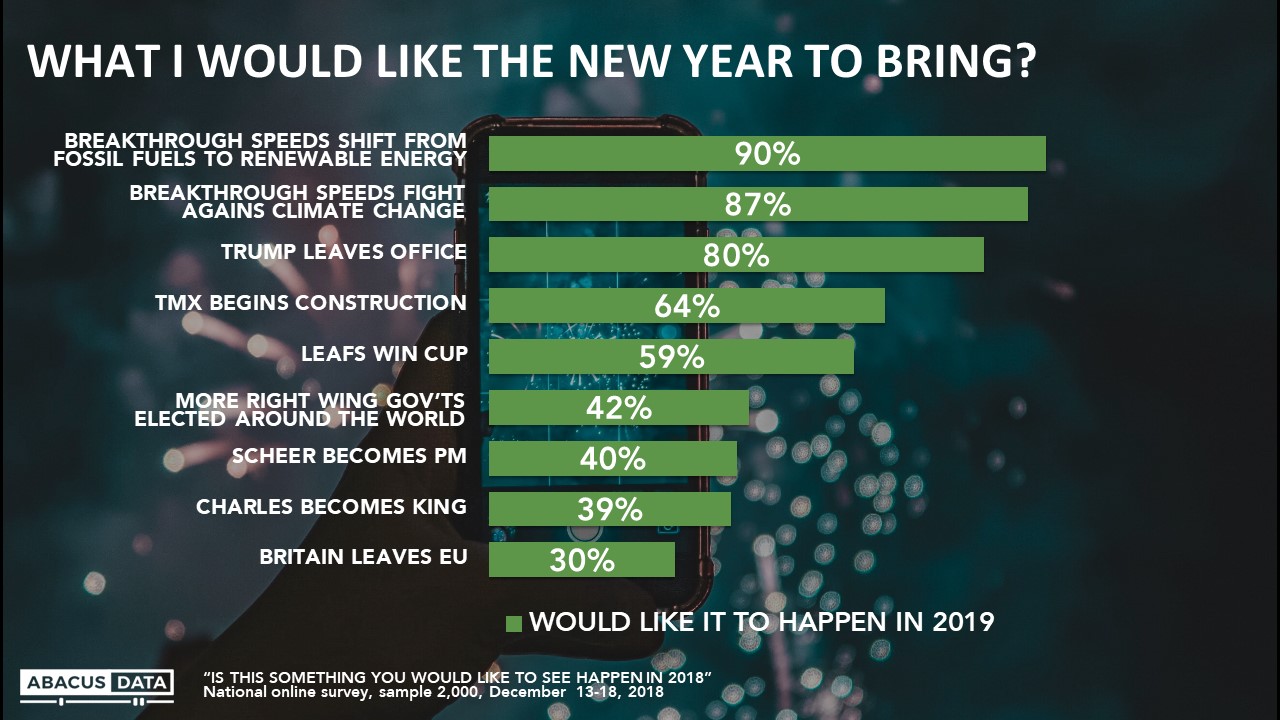

• Almost everyone hopes for a scientific or technological breakthrough that can accelerate progress in the fight against climate change (90%) and a shift from fossil fuels to renewable energy (87%). We asked the question both ways, to see if there would be a difference in response and found only a 3-point gap. In Alberta, 87% would like to see a breakthrough in the fight against climate change and 76% would like to see a breakthrough that accelerates a shift from fossil fuels to renewable forms of energy.

• 8 out of 10 Canadians hope 2019 sees Donald Trump leaving the office of President, including 70% in Alberta, and 67% of current CPC voters.

• Two out of three people hope that the year sees the renewal of construction on the TMX pipeline expansion. This includes 60% in BC, 87% in Alberta, 70% in Ontario, but just 41% in Quebec. 71% of Liberal voters and 49% of NDP voters would like to see construction on the pipeline this year.

• A majority, albeit a somewhat modest majority, would like to see the Toronto Maple Leafs win the Stanley Cup. In Ontario, 79% would like the Leafs to win, but neighboring Quebec finds only 41% share this hope.

• 42% would like to see more right-wing governments elected around the world, and 40% would like to see Andrew Scheer become Canada’s Prime Minister. In Alberta, 58% would like to see Mr. Scheer become PM.

• Only 39% would like to see 2019 be the year that Charles becomes King and only 3 in 10 would like to see Britain leave the EU. A majority (57%) of Conservatives would prefer not to see Brexit happen.

EXPECTATIONS FOR 2019

• A majority (56%) believe TMX construction will happen and that Britain will leave the EU (55%).

• While 80% would like Mr. Trump out of office, 41% think it will happen. One in two people thinks there will be more right-wing governments elected around the world.

• 4 in 10 expect to see a scientific or technological breakthrough that helps speed the fight against climate change and 35% expect to see the same thing in terms of a shift from fossil fuels to renewable energy.

• About one in three (35%) expect Mr. Scheer to become PM (76% of Conservative voters) and a similar number expect Charles to be crowned King.

• Only 28% expect the Leafs to break their 50-year drought this year. In Ontario, 65% do not believe this will happen.

UPSHOT

The results to these questions reinforce our findings throughout the last couple of years on energy and climate issues – people want progress in the fight against climate change and believe in the need for a shift to renewables – but they also want Canada to participate sensibly in the energy markets that exist today, including getting more Canadian oil to new customers.

The political rhetoric implies that large swaths of centrist, Liberal, BC or eastern voters are dug in against the TMX project but the reality in our polling tells a different story. A modest majority in Quebec are against the project, but everywhere else majorities support completing this pipeline. A majority of Liberal voters and half of NDP voters do as well.

For years we’ve also seen a belief that the biggest solutions to the climate and carbon challenges may be found in scientific and technological discoveries to come. This underpins support for policies that include pricing pollution but also incentivizing research into clean technologies.

The responses to the questions about Mr. Trump are remarkable – both in the unusual strength and consistency across partisan lines of antipathy to the US President and in the expectation among 4 in 10 that his Presidency will end sometime in the next 12 months.

Leaf fans may feel more supported by the hopes of other Canadians this year, but in any event, expectations appear to be modest. Hope may spring eternal, but Toronto fans aren’t getting ahead of themselves just yet.”

METHODOLOGY

Our survey was conducted online with 2,000 Canadians aged 18 and over from December 13 to 18, 2018. A random sample of panelists was invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 2.5%, 19 times out of 20. The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region. Totals may not add up to 100 due to rounding.

ABOUT ABACUS DATA

We are the only research and strategy firm that helps organizations respond to the disruptive risks and opportunities in a world where demographics and technology are changing more quickly than ever.

We are an innovative, fast-growing public opinion and marketing research consultancy. We use the latest technology, sound science, and deep experience to generate top-flight research-based advice to our clients. We offer global research capacity with a strong focus on customer service, attention to detail and exceptional value.

As we enter into a new year, we turn our gaze to the future of the millennial generation. January 1st doesn’t just mark the beginning of another year; it marks the first time that boomers will not hold the plurality of decision-making power in a Canadian election. With the average life expectancy of Canadians hovering around 80, this year marks the first wave of millennials entering their middle-aged lives (turning 39). Many millennials have purchased a home (47%) and another 20% are renting and living with their partner. 59% are married/in civil union or are living with their partner. More and more millennials seem to be morphing into the modern versions of their boomer parents.

However, there are still persistent differences between the generations which will play out in 2019. For instance, the average household size in 1980 was approximately 4 persons – 2 parents and 2 kids. Today the average Canadian household ranges closer to 2 person – 2 partners and no kids. Millennial households also earn 35% less on average compared to what their boomer parents were earning at the same time in their lives. Few millennials have been able to find affordable housing that they can independently afford, relying on parents or government assistance to purchase their first home. Fewer millennials own cars and are opting to use public transit, bikes, or rent a car when they need to get around. If this family planning trend continues, we could see a shift in house designs from the atomic family two-car garages and deep backyards to two-person dwellings or multigenerational family homes. Affordability will also be a key component of the millennial housing market. The homes of tomorrow will have to become more affordable, or new saving and mortgaging schemes will have to be developed, to initiate the next generation of homeowners.

Although millennials make less than boomers, they save more. 38% of millennials have no consumer or student debt. Nevertheless, for the other 62% of millennials debt still looms large and an economic downturn or interest rate rise could tip many into poverty. With no secure assets like a house or car available for liquidation if times get hard, millennials may find themselves in precarious financial straits.

On the investment front, millennials are going to continue to demand that their money be invested ethically and sustainably. Millennials have turned the niche multimillion-dollar ethical investment industry into one of the fastest growing and largest investment segments. Millennials are risk-averse and would rather make slow and steady gains in quality investments than short rapid growth with the potential for large losses. Millennials want financial stability and they are fine with government intervention to ensure it. A millennial-dominated financial market will most likely not be as high growth as the boomer-dominated one; markets could anticipate modest growth with investors seeking long-term returns.

Politically, there are also differences. Top issues for boomer include healthcare, the economy, and taxes. The top issues for millennials are housing affordability, job creation, and healthcare; they also place more importance on climate change action and affordable education. Millennials are looking for a parental government – a government that will take care of them if they get in trouble, and ensure the best outcome for everyone. From personal finances to policing, national defence, the environment, and social services, millennials want to feel that the government is a social justice advocate. Millennials do not respond well to negative campaigns but prefer positive visions of the future and communitarian messages that show how Canadians will collectively be better off. Half of all millennials think that life would be better off under a socialist system, political parties need to consider this when positioning themselves in the 2019 election.

Just as their parents did before them, millennials will change how we look at the world. They are well-educated, aspirational, and young. They put great emphasis on being good stewards of the environment and good friends to their fellow human, whether they be a world away or across the street. How will the new pilots of the world tackle the big problems is to be seen, but there is no doubt that whatever way they choose it will be the millennial way.

At Abacus we strive to understand the nuances of generational change and how it impacts you and your business. The Canadian Millennials Report is the largest syndicated study of millennials in Canada. We survey 2,000 millennials twice a year on a range of topics including politics, social values, and consumer trends. If you are interested in learning more about this generation, reach out to us and we would be happy to connect.