Canada’s Housing Crisis: A universally recognized challenge that Canadians believe requires government leadership

In the final segment of our four-part series investigating Canada’s housing crisis, conducted in collaboration with the Canadian Real Estate Association (CREA), we pivot our attention towards evaluating the Canadian public’s perceptions of government performance at all three levels.

These findings, sourced from a survey of 3,500 Canadian adults aged 18 and above, conducted between September 22 and 28, 2023, provide a comprehensive perspective on a crisis that necessitates the collective focus, collaboration, and innovative solutions of government bodies at every tier to ensure that all Canadians can exercise their fundamental right to a secure place they can call home.

Pervasive Housing Market Apprehensions

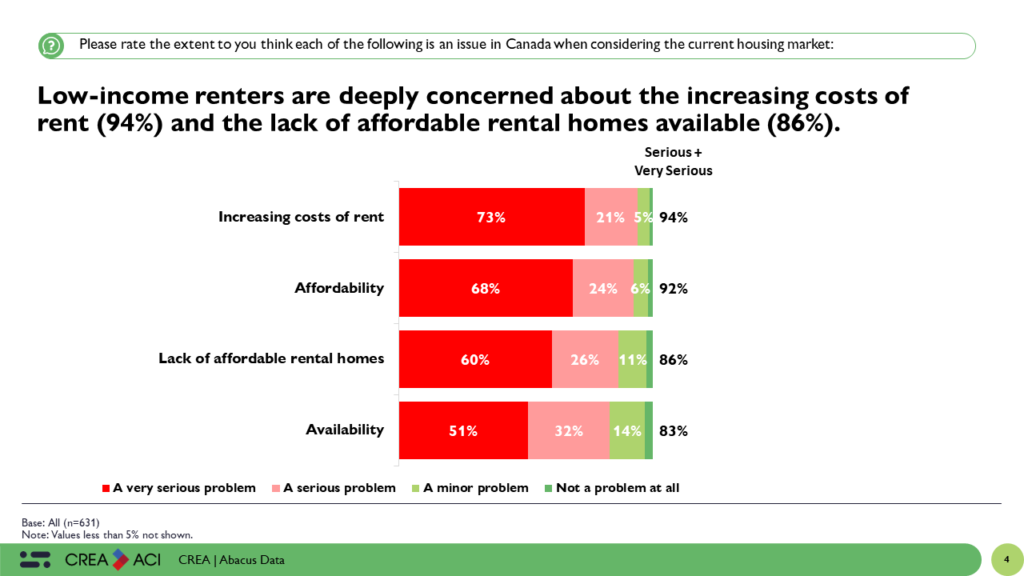

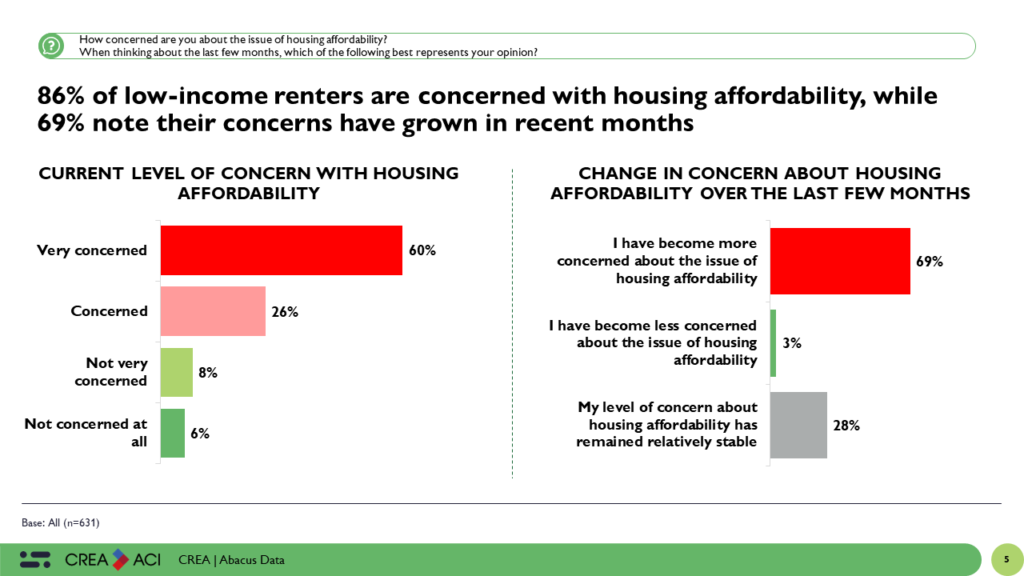

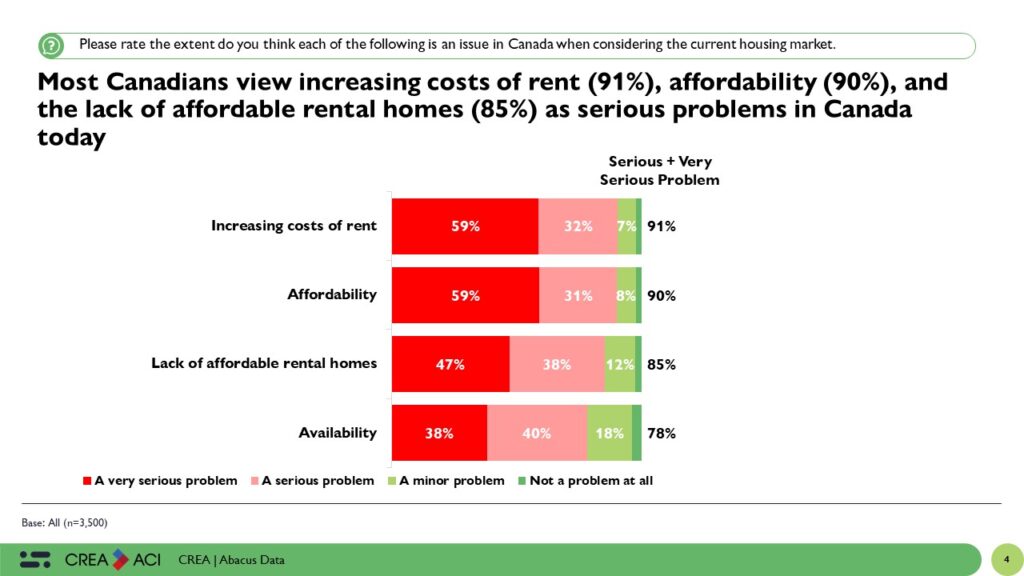

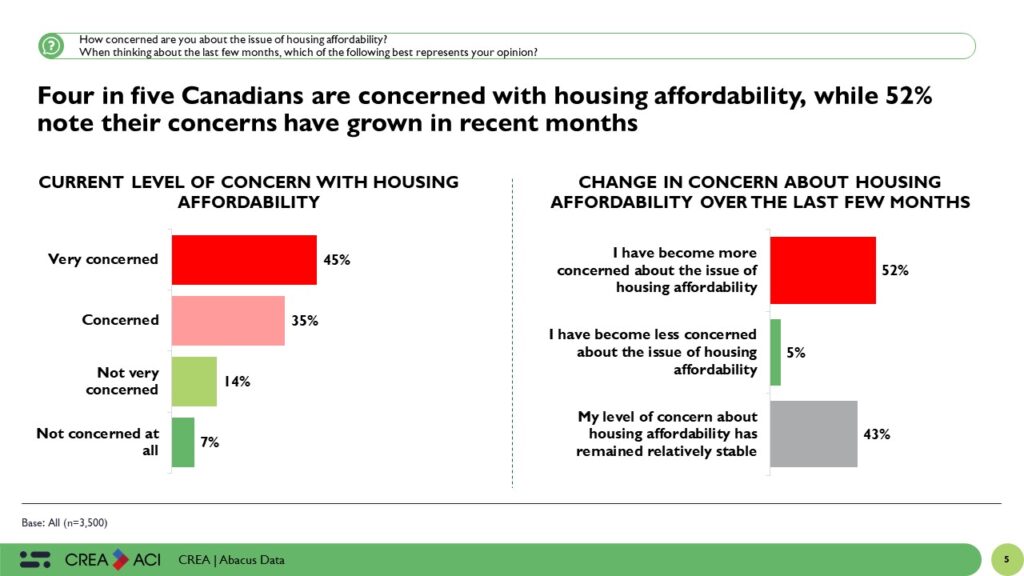

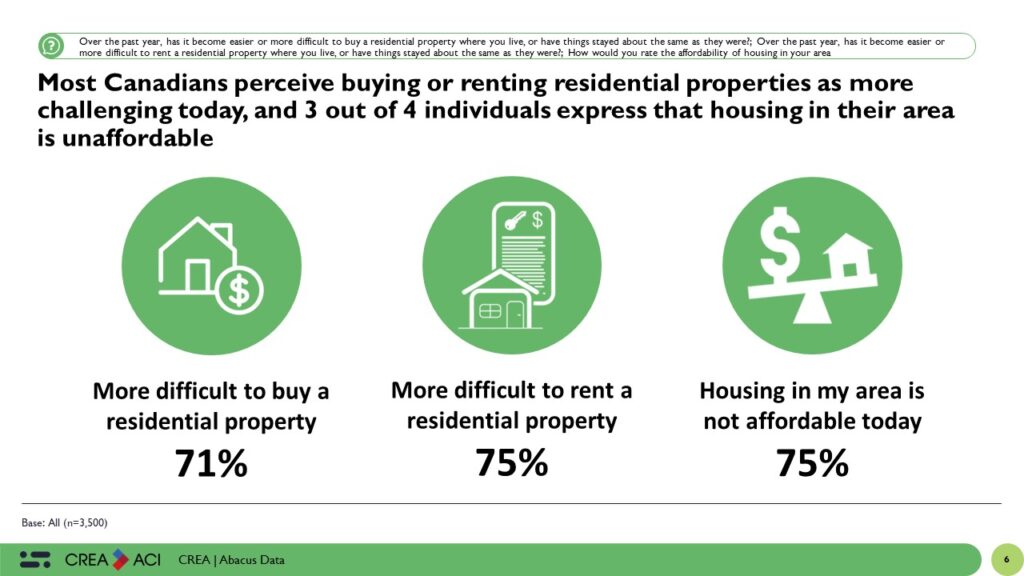

Housing market apprehensions permeate the Canadian landscape, with an overwhelming majority of citizens identifying escalating rent costs (91%), overall affordability challenges (90%), and the scarcity of affordable rental options (85%) as significant issues impacting Canadians today. Notably, 4 in 5 Canadians express overwhelming concerns regarding the affordability of housing in Canada. This collective unease is further underscored by the fact that half of the population has witnessed their concerns about housing affordability intensify in recent months (52%). These concerns are compounded by the prevailing perception that both buying (71%) and renting (75%) residential properties in Canada have become notably more difficult in recent months. Overall, results reveal that a striking 75% of Canadians firmly believe that housing, in its current state, is simply unaffordable.

Government Response and Public Perception: Bridging the Gap: Aligning Government Priorities with Public Expectations

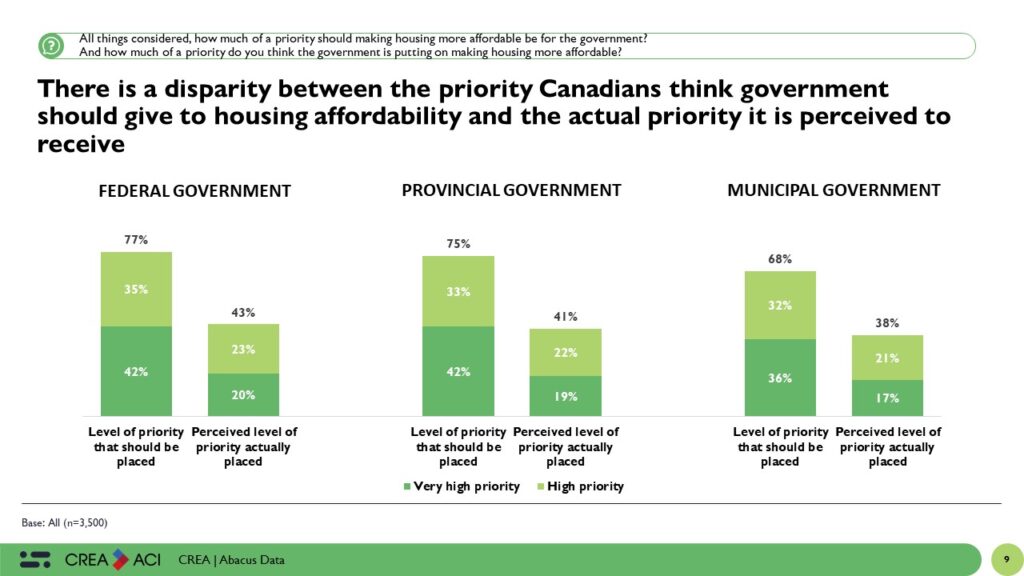

A stark divergence between the government’s perceived priorities and the expectations of Canadians has come to the forefront. The findings reveal that most Canadians believe that housing affordability should be a top priority for federal (77%), provincial (75%), and municipal (68%) governments, while fewer perceive these issues as current priorities (57% for federal, 59% for provincial, and 38% for municipal). This glaring disparity underscores the imperative for better synchronizing public expectations with government actions to effectively combat the housing crisis.

Scrutiny on Government Competence: A Three-Level Assessment

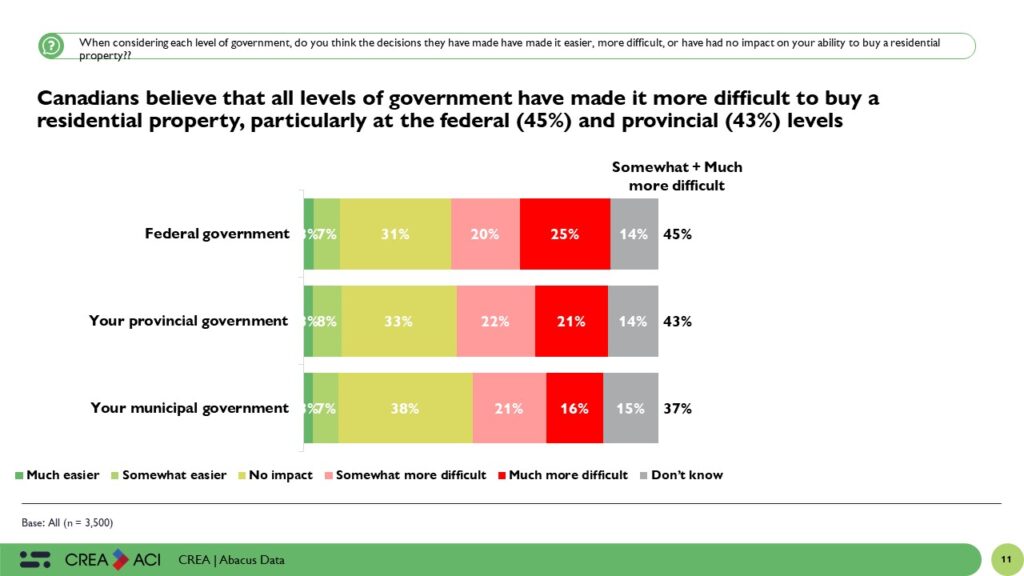

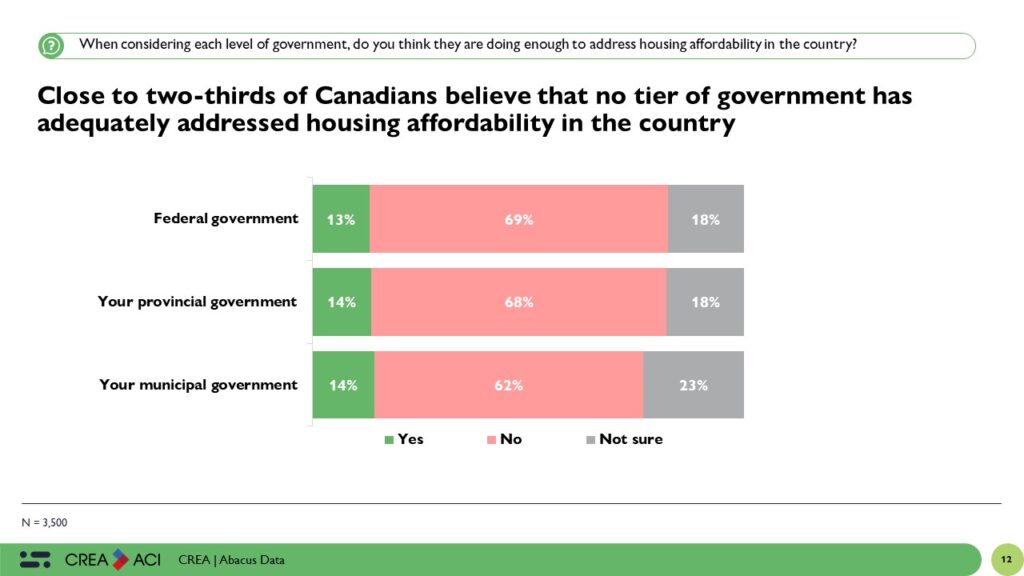

The competence and efficacy of government entities at all three levels in addressing housing concerns have now become a subject of intense scrutiny among the Canadian populace. A substantial 45% of Canadians assert that the federal government has actively contributed to the increased complexity of residential property acquisition, a sentiment mirrored by 43% regarding provincial governments. Even more astonishing, close to two-thirds of Canadians maintain the conviction that no tier of government – whether federal, provincial, or municipal – has exhibited adequate dedication to tackle the affordability crisis in the housing market.

Echoes of Dissatisfaction: Assigning Blame, Identifying Barriers, and the Cry for Effective Government Response

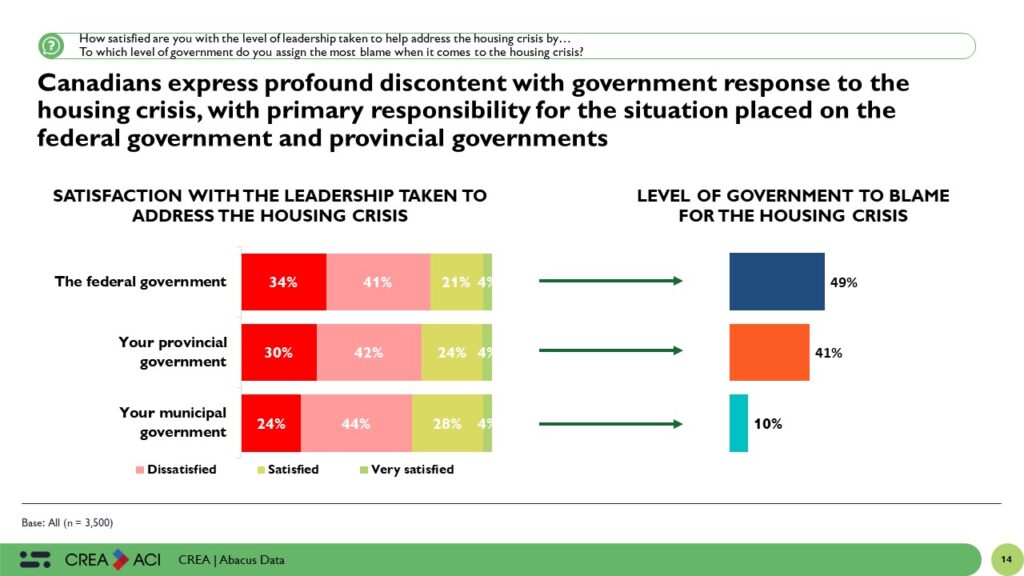

Canadians are highly dissatisfied with government responses to the housing crisis, with 75% expressing their discontent with the federal government, 72% with their provincial counterparts, and 68% with municipal authorities. These widespread discontented sentiments underscore the urgent demand for a more effective and coordinated approach from all levels of government. Additionally, when it comes to identifying responsibility for the ongoing housing crisis, 49% of Canadians attribute it to the federal government, closely followed by 41% placing blame on their provincial government. This prevailing perception highlights the need for improved collaboration between federal and provincial authorities, a sentiment held by two-thirds of the Canadian population (66%), to address the housing crisis effectively. This perception underscores the urgent need for enhanced cooperation and coordination between government tiers to address the housing crisis adequately.

Solutions and Opportunities for Change

The resounding call for immediate and resolute action resonates across the nation. Now, more than ever, Canadians anticipate government authorities at all levels to use to the occasion and assume a leadership role in addressing this urgent matter. As we conclude our four-part analysis of Canada’s housing crisis in partnership with the Canadian Real Estate Association, it is imperative to emphasize the need for a call to action. This call underscores the pivotal role government at all three levels must undertake to address this crisis effectively.

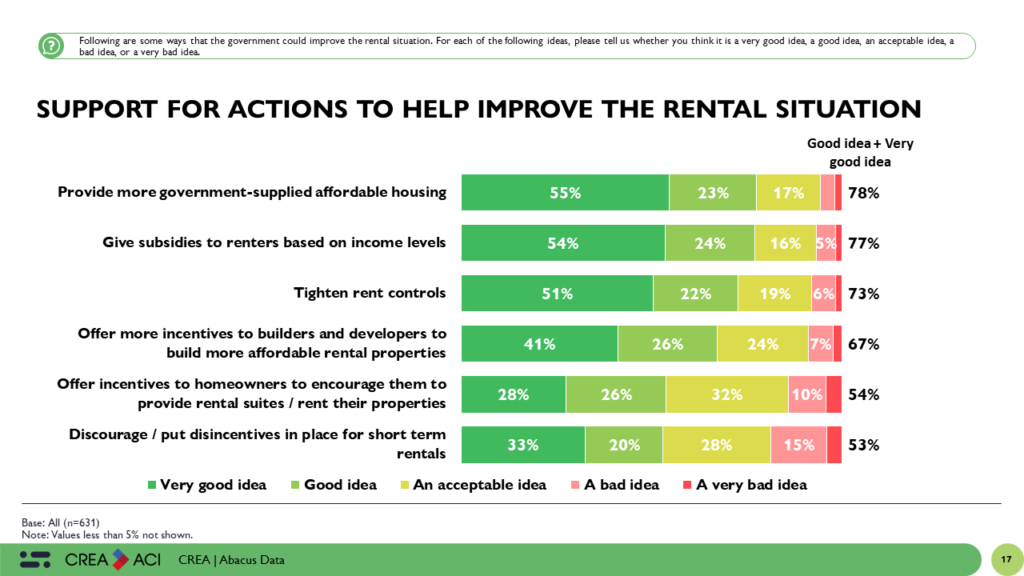

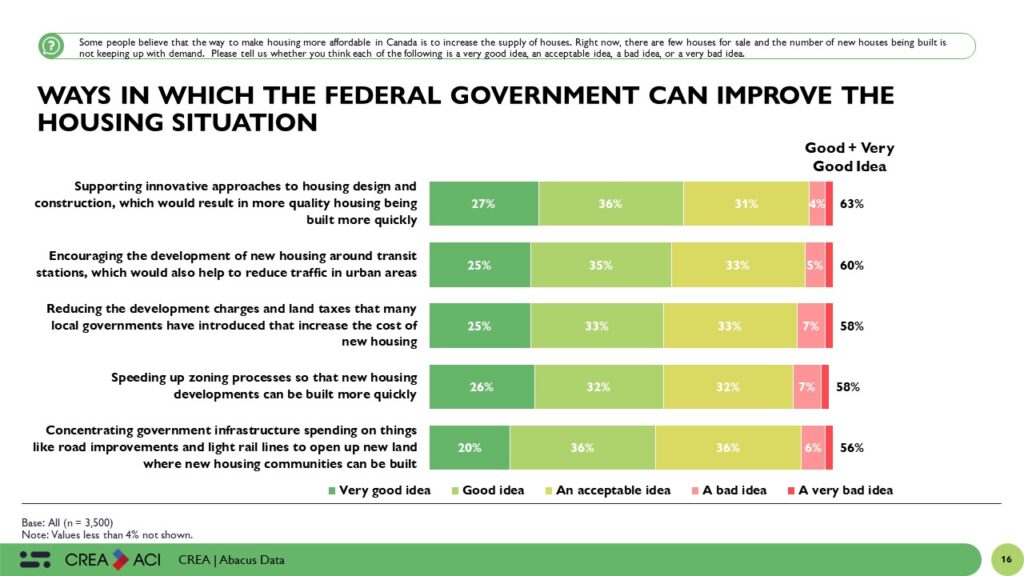

- Support for Innovative Housing Design: A significant majority of Canadians endorse innovative housing design and construction (64%). This involves adopting modern construction techniques and technology to expedite the creation of high-quality housing, addressing the growing demand for homes while enhancing housing quality.

- Reducing Development Charges and Land Taxes: A majority of Canadians, nearly 60%, back the idea of cutting local government development charges and land taxes. These charges often inflate the cost of new housing, limiting accessibility. Lowering these fees at the federal level can contribute to increased housing affordability.

- Accelerating Zoning: Speeding up zoning procedures is a vital aspect of tackling the housing crisis. With 58% support, it’s evident that a substantial number of Canadians view it as an effective approach. Faster zoning translates to quicker construction and more housing units, addressing the demand in high-pressure housing regions.

- Infrastructure Focus: Although not the most popular option, channeling federal infrastructure investments into road upgrades and light rail lines remains a viable approach with 56% support. This strategy seeks to create new housing development opportunities by enhancing transportation infrastructure. While it may take time to witness the full effects, these investments can have a lasting positive impact on housing availability.

Overall, the voices of Canadians underscore the urgency of addressing the housing crisis through a multifaceted approach. Innovative housing design, reductions in development charges and land taxes, expedited zoning procedures, and an emphasis on infrastructure investments reflect some of the initiatives that Canadians support. These findings illuminate the necessity of collaborations at all levels of government to implement solutions that resonate with the Canadian population, ultimately ensuring affordable and accessible housing for all.

The Upshot

The housing crisis in Canada has hit a critical juncture, characterized by significant challenges related to the affordability and availability of housing. The results underscore the widespread lack of confidence Canadians hold in all levels of government to effectively resolve the housing crisis. Dissatisfaction with current government actions, a perception that the issue isn’t receiving the priority it deserves, and the belief that insufficient measures have been taken to date are prevalent.

The resounding call for immediate and resolute action resonates across the nation. Now, more than ever, it falls upon the federal government to step into a leadership role and address this pressing issue. As we conclude our four-part analysis of Canada’s housing crisis in partnership with the Canadian Real Estate Association, it is imperative to emphasize the need for a call to action. This call underscores the pivotal role the federal government must undertake to address this crisis effectively.

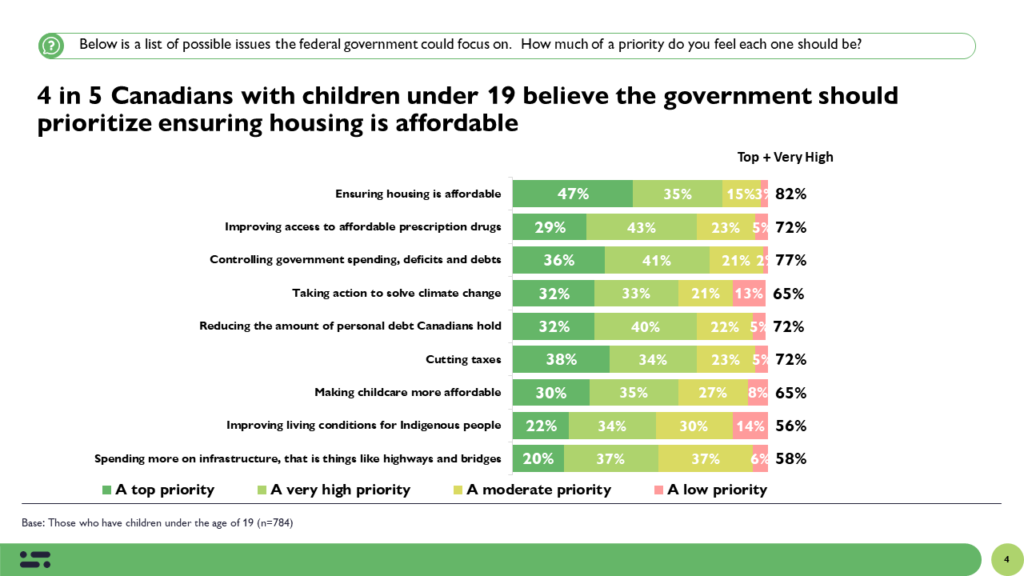

- Prioritize Housing Affordability: Recognize housing affordability as a top priority for the federal government. Listen to the voices of Canadians, where 82% have emphasized the paramount need for affordable housing. Align government priorities with the public’s expectations.

- Coordinate Government Efforts: Housing affordability is a multifaceted issue that spans federal, provincial, and municipal jurisdictions. Forge strong partnerships and collaborative efforts between all levels of government to create a unified approach to addressing the crisis. Housing knows no boundaries; neither should our solutions.

- Streamline Housing Policies: Develop comprehensive and streamlined housing policies that are responsive and effective. The current housing market apprehensions demand well-thought-out measures that ease financial burdens for both renters and homebuyers. This may involve tax incentives, subsidies, and strategic investments to make housing more affordable and accessible.

- Innovate and Expedite: Embrace innovative housing design, streamline zoning processes, and reduce development charges and land taxes. These solutions have garnered significant support from Canadians and can expedite the availability of affordable housing units.

- Crisis of Access and Affordability: It is important to remember that the housing crisis is not just about affordability but also about accessibility. Policies should address the needs of all Canadians, ensuring that everyone has a fair opportunity to access quality and affordable housing.

The time for action is now. The federal government has the opportunity to lead the way in ensuring that housing in Canada is accessible, affordable, and of high quality. By responding to the widespread concerns of Canadians and taking decisive steps, the government can make a lasting and positive impact on the housing landscape.

However, failure by the federal government to take a leadership role in addressing the housing crisis risks worsening an already dire situation with severe consequences. The crisis has caused widespread discontent among Canadians, and a lack of effective action could further erode public trust and confidence in the government. Failing to address the housing crisis prolongs suffering, tarnishes the government’s reputation, and may lead to political repercussions and public discontent. Inaction is not an option, as it jeopardizes the government’s standing in the eyes of the Canadian populace.

Methodology

The survey was conducted with 3,500 Canadian adults from September 22 to 28, 2023. A random sample of panelists were invited to complete the survey from a set of partner panels based on the Lucid exchange platform. These partners are typically double opt-in survey panels, blended to manage out potential skews in the data from a single source.

The margin of error for a comparable probability-based random sample of the same size is +/- 1.66%, 19 times out of 20.

The data were weighted according to census data to ensure that the sample matched Canada’s population according to age, gender, educational attainment, and region.

This survey was paid for by the Canadian Real Estate Association (CREA).

Abacus Data follows the CRIC Public Opinion Research Standards and Disclosure Requirements that can be found here: https://canadianresearchinsightscouncil.ca/standards/